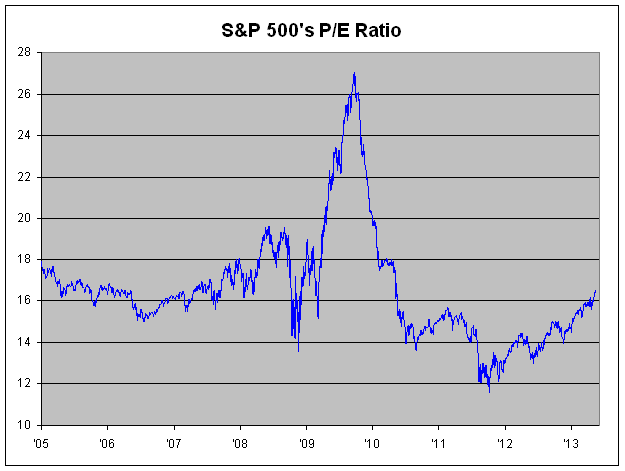

Three-Year High for the S&P 500’s P/E Ratio

On Friday, the Price/Earnings Ratio for the S&P 500 closed at a three-year high. By historical comparisons, the P/E Ratio still ain’t that high. It’s currently at 16.49. The ratio has been quite low for the last few years. At its low point in October 2011, the S&P 500’s P/E Ratio touched a 22-year low. All told, the market’s P/E Ratio was expanded by more than 40% which adds a nice breeze to any market rally.

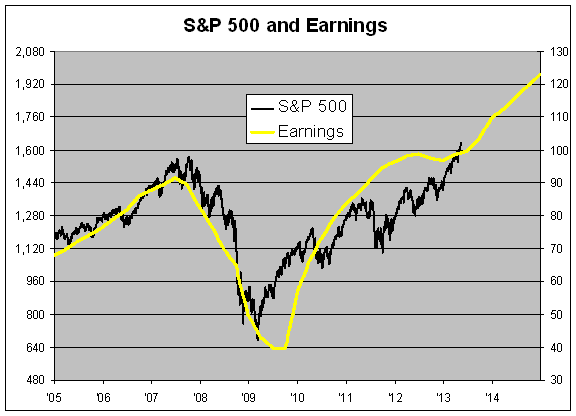

Here’s a look at the S&P 500 (black line, left scale) along with its earnings (yellow line, right scale). I scaled the two lines at a ratio of 16-to-1 so whenever the lines cross, the P/E Ratio is exactly 16. As you can see, we just dipped our heads above the line. For technical note, I’m using the operating earnings as provided by S&P.

Let me point out a few deficiencies of the P/E Ratio. (By the way, just because there are some problems with a metric doesn’t make it useless. You simply need to be aware of its limitations.) The P/E Ratio is made up of two numbers, the price and the earnings. Price is a fixed-point number. You know exactly what it is at any point in time. Earnings, however, are a ratio. It’s the amount of money earnings between two points. The P/E Ratio mixes these two numbers. That usually isn’t an issue, but sometimes it can be.

The biggest problem is that stock prices look ahead while earnings tell you what just happened. Notice how in 2009 the stock market, the black line correctly anticipated the upturn in earnings, the yellow line. Because of the mismatch, the P/E Ratio soared. I remember this caused a lot of consternation among market bears. The P/E Ratio was telling us the market was expensive when it was really its cheapest.

Here’s a look at the market’s P/E Ratio. It’s the exact same graph as above except it’s the black line divided by the yellow line.

But we can also see something interesting about the market crackup in 2007 and 2008. What makes that period noteworthy is that it was largely unexpected as the stock prices quickly reacted to crumbling earnings. On the other hand, you can see how market downdrafts in 2011 and 2012 were incorrect expectations of trouble ahead. Perhaps the market was so burnt in 2008 that it’s become overly cautious today.

The issue for us right now is the stalling out of earnings growth over the last few quarters. The future part of the yellow line is Wall Street’s forecast. If analysts are correct that this is just a small notch in an upward earnings trend, the market is probably underpriced. At ratio of 16 and expected earnings of $123.13, it could be at 1,970 by the end of next year. That’s a 20.6% gain in about 20 months.

Of course, that involves a lot of assumptions that are probably too thin to rely on. Last year, I recall Barry Ritholtz pointing out a chart showing the success rate of analysts’ forecasts. It’s not an enviable record. To oversimplify things, corporate earnings tend to go in two modes — slow, steady rises or sharp dropoffs. Analysts try to split the difference by almost always predicting modest increases. As a result, they’re usually slightly too pessimistic or wildly overly optimistic. The hard part is catching the economy’s turning points. Once you’ve mastered that (LOLz), everything else is easy.

Posted by Eddy Elfenbein on May 13th, 2013 at 10:00 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His