The Long View for Stocks

Ibbotson Associates is known for their collection of long-term financial returns data. Their latest yearbook isn’t out yet, but I was able to bring the data up to date by using numbers from Standard and Poor’s.

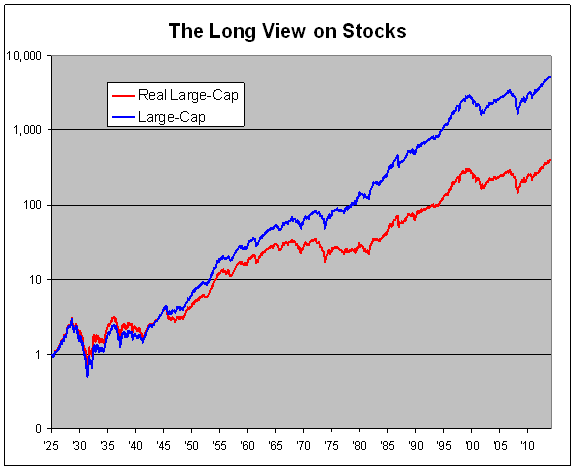

Here’s what the chart looks like of long-term stock returns from December 31, 1925 to December 31, 2014.

The blue line is stocks and dividends but is not adjusted for inflation. Starting with $1, it turns into $5,300 by the end of 2014. That’s an annualized total return of 10.12%.

The red line is the blue line adjusted for inflation. Stocks have averaged a total real return of 6.98% annualized over the last 89 years. That’s roughly stocks doubling in real value every decade.

Of course, there’s a lot of variation in that. Over the last 15 years, real stock returns have averaged less than 2% per year.

Jeremy Siegel often talks about how stocks have returned 7% in real terms over the long haul. I’ve even heard this referred to as the Siegel Constant.

Personally, I don’t think investors should expect 7% real returns going forward. The problem with this past data is that it’s based on the American Century. I’m still a long-term bull but we can’t replicate the success of 20th Century America.

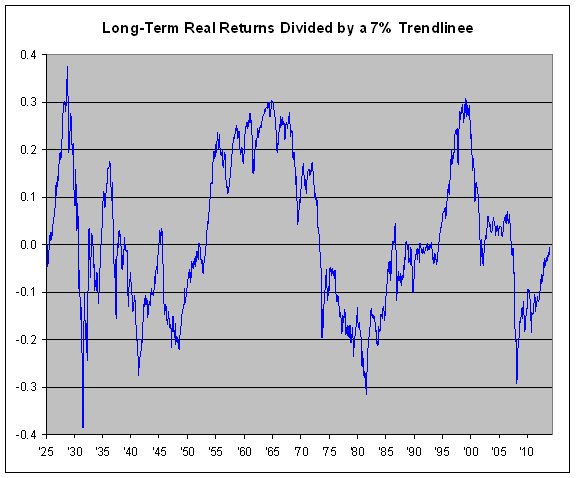

Now let’s have more fun with the data. I took the red line and divided it by a 7% trend line, meaning a line that just rises by 7% per year, every year. So when we divide the two, it means that whenever the line is rising, stocks are outperforming their long-term average. When it’s falling, they’re trailing it. (Even a mildly declining line is still making money for you.) I then made it a logarithm chart so it would be easier to read. Here’s what I got:

A few thoughts: First, notice how cyclical the chart is. Stocks don’t return 7% per year consistently. Rather there are long periods of outperformance followed by long stretches of underperformance.

Second, the 1949 to 1956 bull market was one of the greatest in history. No one talks about that one. I think it’s because it never crashed.

Third, the 1929, mid-1960s and 2000 peaks are all roughly similar. The mid-1960s peak was a rolling one. Things didn’t really fall apart until the 1973-74 crash.

Similarly, the 1932, 1982 and 2009 troughs aren’t too far apart.

Fourth, 1929 to 1932 sucked. Seriously.

Fifth, as strong as the last six years have been for stocks, we’re merely back to our long-term average. Actually, we’re still a bit short of it. Stocks would have to gain about 20% in 2015 for us to be back at the mid-point.

Finally, if you use a little imagination, this chart somewhat resembles the long-term chart of P/E Ratios. This makes sense since earnings have tended to increase at a fairly steady pace over the long haul. Not quite like a 7% trend line, but not too far off, either.

Posted by Eddy Elfenbein on January 22nd, 2015 at 1:21 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His {kind=link}