CWS Market Review – July 31, 2015

“Investment success does not require glamour stocks or bull markets.” – John Neff

Good news—the earnings recession may finally be over. Not all the numbers are in just yet, but Q2 earnings for the S&P 500 may have been slightly higher than they were one year ago. Earnings had declined for the previous two quarters, and this looked like it was going to be a third. In fact, as late as July 1, analysts had been expecting an earnings drop of 3%. But business hasn’t been suffering due to poor fundamentals. Rather, it’s been damage caused by the strong dollar that’s dinged earnings.

Fortunately, the stock market has mostly ignored the dollar’s impact, and stock prices haven’t declined. In fact, the incredible trading range of the last six months lives on. The S&P 500 closed Thursday at 2,108.63. Remarkably, that’s the eighth time since March that the index has closed with a 2,108 handle. Consider this stat: Since February 12, the S&P 500 has closed within 1% of today’s close 69% of the time. In other words, Wall Street has become a giant treadmill. Or rather, a giant $20 trillion treadmill that’s severely emotionally stunted.

This has been a very good earnings season for our Buy List. Through Thursday, 12 of the 14 Buy List earnings reports have exceeded expectations. This week, we had some solid reports. Ford Motor (F) beat consensus by 10 cents per share. Express Scripts (ESRX) beat earnings and raised its full-year guidance. (I love it when our stocks do that!)

In this week’s CWS Market Review, I’ll run down our latest earnings reports. We also had a Fed meeting this week. The central bank is strongly hinting that a rate hike is coming. I’ll have more on that in a bit. I also have several updates to our Buy Below prices. Plus, I’ll preview our final earnings report for this earnings season which comes out next week. But first, let’s look at the all-important one-word addition to this week’s Fed policy statement.

The Federal Reserve Adds One Word

Can one word move the market? The answer is, apparently, yes. This week, the Federal Reserve released its latest policy statement, and it contained a small but important change.

In the previous statement, the Fed said that it wanted to see “further improvement” in the jobs market before raising interest rates. This week, the Fed said it wants to see “some further improvement” in the labor market before raising rates.

In other words, the Fed sees a rate increase coming sooner than expected. Trust me: That “some” is some big deal. If you’ve read Fed transcripts as much as I have (don’t ask), you’ll know that they take every word seriously. The Fed members debate the precise meaning of every sentence, word and paragraph. You can tell the economists put a lot effort into this. That’s why they’re written so poorly.

The futures market now thinks there’s a 63% chance the Fed could raise rates at its December meeting. There’s even been talk of a rate increase coming as early as September. That’s probably a long shot, but it’s certainly being considered.

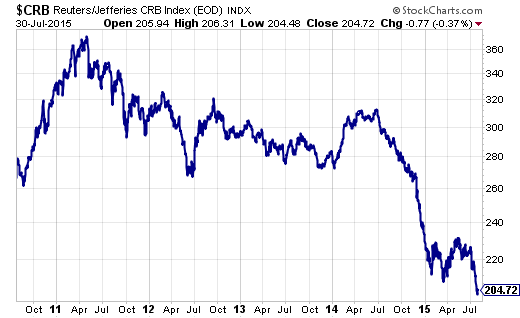

Investors need to understand that there are some understandable reactions to a higher-rate environment. For example, July is shaping up to be one of the worst months ever for commodities. The CRB Index is plunging (see above). Gold is near a five-year low. Copper is at a six-year low, and oil is down about 20% in the last month. Companies are feeling the squeeze. Chevron (CVX) and Royal Dutch Shell (RDS) just announced big job cuts. Linn Energy (LINN) just ditched its dividend. Commodity-dependent markets like Brazil (EWZ) have sold off sharply.

The beneficiaries of lower commodity prices will be retail and consumer-oriented sectors as less money goes toward filling up at the pump. Tech stocks should also do well. On our Buy List, stocks such as Ross Stores (ROST) and PayPal (PYPL) will continue to prosper off lower commodities. Now let’s look at some of last week’s earnings reports.

Ford Motor Beats by 10 Cents per Share

Investors were clearly nervous about Ford Motor (F) going into this earnings season. On Monday, the stock got as low as $14.23 per share, which is very inexpensive.

I’m happy to say that the doubters were wrong. Ford had very good results for Q2. The automaker earned 47 cents per share which topped estimates by 10 cents per share. The shares rallied above $15 for the first time in a month. Thanks to the revamped F-150, Ford posted record profits for North America. Their operating margin came in at a healthy 11.1%. The F-150s are selling for an average price of $44,100.

I was particularly glad to see Ford reiterate its full-year operating profit range of $8.5 billion to $9.5 billion. I can’t exactly translate that into a post-tax EPS figures, but it’s probably somewhere between $1.40 and $1.60. In other words, Ford is still going for less than 10 times earnings.

Shares of Ford rallied more than 4.5% on Tuesday and Wednesday. It’s about time. This is why we’ve stuck with this frustrating stock. This was a very good quarter for Ford. Ford Motor remains a good buy up to $17 per share.

Higher Guidance from AFLAC and Express Scripts

Also on Tuesday, AFLAC (AFL) reported Q2 operating earnings of $1.50 per share. That was two cents below expectations. That broke our unbeaten streak this earnings cycle (Ball Corp would also miss).

Despite the earnings miss, the details for AFLAC were pretty good. The weak yen knocked off 14 cents per share. AFLAC actually raised its full-year guidance. Previously, it had projected full-year currency-neutral profits to rise between 2% and 7%. The new range is 4% to 7%. That’s small, but I’ll take it.

AFLAC sees Q3 earnings ranging between $1.40 and $1.53 per share. That’s within Wall Street’s view of $1.48 per share. For the whole year, AFLAC now sees earnings coming in between $5.88 and $6.17 per share. Wall Street had been at $5.97 per share. These ranges assume the yen averages 120 to 125 per dollar.

I was also pleased to hear CEO Dan Amos effectively rule out any big acquisitions for AFLAC. To be specific, he said, “The prices of insurance companies are through the roof.” He’s a top-notch CEO. Wall Street liked AFLAC’s higher guidance. Shares of AFL rose 1.3% on Tuesday and another 3.5% on Wednesday. For now, I’m going to keep my Buy Below for AFLAC at $65 per share. This is a good company.

Express Scripts (ESRX) reported Q2 earnings of $1.44 per share. That beat estimates by four cents per share.

For Q3, Express sees earnings ranging between $1.41 and $1.45 per share. Wall Street had been expecting $1.43 per share. The pharmacy-benefits manager also raised its full-year guidance. The new range is $5.46 to $5.54 per share which represents growth of 12% to 14%. The previous guidance was $5.37 to $5.47 per share. Three months ago, they narrowed their guidance by two cents per share at both ends. Last year, the company made $4.88 per share.

The stock initially gapped up after the earnings report, but later it slid back. It’s nothing to worry about. As with AFLAC, I’m keeping a fairly tight Buy Below on this one. Express Scripts is a solid buy up to $92 per share.

Fiserv on Track for 30 Straight Double-Digit Years

On Wednesday, Fiserv (FISV) posted Q2 earnings of 95 cents per share. That was one penny better than expectations. It was also 17% above last year’s Q2.

I like this stock a lot. They’re pretty quiet. Fiserv simply delivers stellar earnings report after stellar earnings report. The company reiterated its full-year range of $3.73 to $3.83 per share. That’s an increase of 11% to 14% over last year’s profit of $3.37 per share. Their six-month profit is up to $1.83 from $1.63 per share last year. Fiserv is on track to grow earnings by double digits for the 30th year in a row.

I’ll warn you that Fiserv isn’t a value stock, but I think its growth and reliability deserve an extra multiple. This week, I’m raising my Buy Below on Fiserv by $11 to $93 per share.

Ball Corp. Is a Buy up to $75 per Share

Ball Corp. (BLL) became our second company to miss earnings this earnings season. For Q2, the can maker earned 89 cents per share which was five cents below expectations. Ball is a well-run outfit, but frankly, this has been a tough environment for them.

CEO John A. Hayes said, “As we have been discussing throughout this year, headwinds related to foreign-currency translation, higher metal premiums in Europe, deferred compensation costs associated with director retirements and project start-up costs related to growth capital investments persisted and totaled 23 cents and 39 cents, respectively, in the second quarter and first half of 2015. Numerous capital projects are underway in North America, Europe and Southeast Asia and will fully ramp up in late 2015 and the first half of 2016.”

Ball hasn’t changed their full-year outlook. They still expect free cash flow of $600 million (roughly $4.35 per share). In Europe, the company is getting some regulatory pushback with its Rexam deal. To be fair, a Ball-Rexam combo would be a powerhouse in the can biz. But I can’t say I would be heartbroken if the deal falls through. These big mergers are hard to pull off. The most likely outcome is that they’ll have to sell off some assets. Don’t let the earnings miss fool you: Ball is doing just fine. I’m keeping my Buy Below for Ball Corp. at $75 per share.

I’m writing this to you early on Friday. Moog’s (MOG-A) earnings report comes out later today. I’ll recap the report in next week’s CWS Market Review. But I don’t like to sugarcoat my mistakes. Moog has struggled this year. Wall Street expects earnings of 94 cents per share.

Upcoming Earnings from Cognizant Technology Solutions

Cognizant Technology Solutions (CTSH) is one of our top-performing stocks this year, but most of CTSH’s surge came at the beginning of the year. It hasn’t done much since.

Three months ago, Cognizant rallied after a very good earnings report. The shares, however, soon gave back those gains. For Q2, the IT outsourcer expects earnings of at least 72 cents per share on revenue of at least $3.01 billion. For the whole year, they see earnings of at least $2.92 per share on revenue of at least $12.24 billion. I’ve looked at the numbers and they should easily beat 72 cents per share.

Other Buy List Updates

Our Buy List has been doing quite well lately. Through Thursday, we’re up 6.68% on the year (not including dividends). Our lead against the S&P 500 has stretched to 4.24%.

In last week’s CWS Market Review, I told you about the strong earnings report from CR Bard (BCR). The company beat estimates by nine cents per share. Later, on the conference call, Bard raised its earnings guidance. The company expects Q3 to range between $2.21 and $2.25 per share. Ball raised full-year guidance by five cents at both ends. The new range is $9.00 to $9.05 per share. This week, I’m raising my Buy Below on CR Bard by $20 to $204 per share. I think that’s a CWS record.

I also want to cut back my Buy Belows on two of our stocks. This week, I’m lowering my Buy Below on Oracle (ORCL) to $42 per share, and on Bed Bath & Beyond (BBBY) to $70 per share. Both stocks have pulled back recently, and I wanted our Buy Belows to reflect that.

That’s all for now. Next week is the last big week for earnings this season. We’ll also get the important turn-of-the-month econ reports. Personal income, auto sales and ISM are on Monday. Friday is the big July jobs report. The unemployment rate is currently at a seven-year low. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on July 31st, 2015 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His