CWS Market Review – December 11, 2015

“Other guys read Playboy. I read annual reports.” – Warren Buffett

Get ready! Next week is a big week for us and for Wall Street. On Tuesday and Wednesday, the Federal Reserve meets in Washington and will very likely raise interest rates for the first time in nine and a half years.

The day that some thought would never come is finally at hand. No more QE. No more Operation Twist, and no more ZIRP (Zero Interest Rate Policy). A lot has changed since June 2006. Believe it or not, Apple was around $8 per share. Companies like Facebook and Twitter had just been started, and Uber was still a few years away.

But our Buy List was already around. Which reminds me: the other big news coming next week will be the 2016 Buy List. I’ll unveil the new list in next week’s issue. As a reminder, I’ll be adding five new stocks and deleting six of our current stocks. The extra one is the due to the PayPal spinoff. The new Buy List will go into effect at the start of trading on January 4. That will be the first day of trading for the New Year.

In this week’s CWS Market Review, I want to take a closer look at the dramatic decline in the price of oil. OPEC has effectively surrendered, and the price of crude is at its lowest point in seven years. I’ll also preview next week’s earnings report from Oracle (ORCL). Plus, we got a nice 10% dividend increase from Stryker (SYK). Since 1991, the orthopedic stock has raised its payout by 243-fold! But first, I want to take a closer look at the stock market which has been a bit more complicated than the indexes suggest.

The Stock Market Isn’t One Giant Stock

On the surface, this has been a flattish year for stocks, but if we peer just below the surface we can glimpse a much more complicated environment. The fact is, this has been a very unbalanced market. The gap between the biggest winners and everybody else hasn’t been this wide in 16 years.

The last time we saw a spread like this was during the Tech Bubble in 1999. If you take away a small number of very big winners, this has been a pretty blah year for the overall market. Here’s a jaw-dropping stat: According to Goldman Sachs, 20% of the margin growth for the entire stock market during this bull market has come from one stock—Apple.

Even recently, the market’s stats tell a complex story. For example, the S&P 500 has rallied nine times in the last 10 weeks. I would never have guessed that to be the case. (This current week will probably be a downer, but I’m writing this on Friday morning.) Yet on Wednesday, the S&P 500 touched its lowest close in nearly a month.

The index hasn’t been able to get much traction lately. We haven’t had back-to-back up days since November 2-3. That’s one of the longest such streaks in decades. The last nine up days for the market have all been followed by down days. There’s just no follow-through. Puts against losses in the S&P 500 are now worth twice the calls for similar gains.

Ryan Detrick (a must-follow on Twitter) notes that the S&P 500 touched 2,100 an amazing 55 times this year. That’s 23% of the trading days. Twice this year, the Dow has had 100-point moves for seven consecutive days. It very nearly happened a third time this week. Compare that to last year when it didn’t happen once.

Through Thursday, the S&P 500 is down a scant 0.32% on the year. No big deal, right? Yet 151 stocks are up more than 10% on the year, while another 174 are down more than 10%. The middle has been hollowed out. Only about one third of the index even comes close to reflecting what “the market” is doing—and I’m using a very broad definition for that term.

In fact, we can see this effect on our Buy List. While we’re up more than 47% in Hormel Foods (HRL), together with a 31% winner in Fiserv (FISV) and three more +20% winners, we’ve been hurt by big losses in Bed Bath & Beyond (BBBY) at-29% and Qualcomm (QCOM) at-34%. In markets like this, you feel the key isn’t picking big winners but staying away from big losers.

One of the candid market stats comes from Morgan Housel, who writes, “According to JP Morgan, 40% of stocks have suffered ‘catastrophic losses’ since 1980, meaning they fell at least 70% and never recovered.” This is a good reminder that investors ought to use some caution whenever they talk about “the market” as if it’s one giant stock.

Don’t Let the Fed Scare You

I’ll warn you now. The financial world will come to a halt on Wednesday afternoon, waiting to hear what the Fed has to say. The futures market now thinks there’s an 83% chance that rates will go up next week. Personally, I think that’s about 16.99% too low.

In the October 30 issue of CWS Market Review, I said that if the next two jobs reports average 180,000 net new jobs, the Fed will go ahead and raise rates in December. Since then, the two jobs reports were +298,000 for October and +211,000 for November. That averages to +254,500.

Ultimately, a rate increase is a positive sign in that it reflects that our economy has finally gotten back to normal after a long and painful recession. Of course, we’re not fully recovered yet, but we should note the progress that’s been made. I’m still troubled by the low workforce-participation rate, although some demographic factors are at play. I’d also like to see a greater increase in average hourly earnings.

Following the meeting, Fed Chairwoman Janet Yellen will face the media in a press conference. The members of the FOMC will also update their economic projections (these are the “blue dots,” so named for the Fed’s scatterplot graphs). In my opinion, the Fed’s outlook has been far too hawkish, meaning they see rates going up too far too fast.

Jon Hilsenrath, the WSJ reporter most widely assumed to be the conduit for the Fed, recently noted that the Fed doesn’t want to be locked in a predetermined path. The central bank wants to maintain its flexibility in determining the right path for interest rates.

Here’s the interesting part: what comes after next week? The futures market thinks the Fed will probably raise rates again at its April 2016 meeting. Sounds reasonable. After that, they’re almost evenly split on the chances for a third hike at the September 2016 meeting. What this means is that the market is not expecting an aggressive round of rate hikes. In fact, the Fed funds rate will most likely continue to be well below inflation for all of 2016. That’s good for stocks.

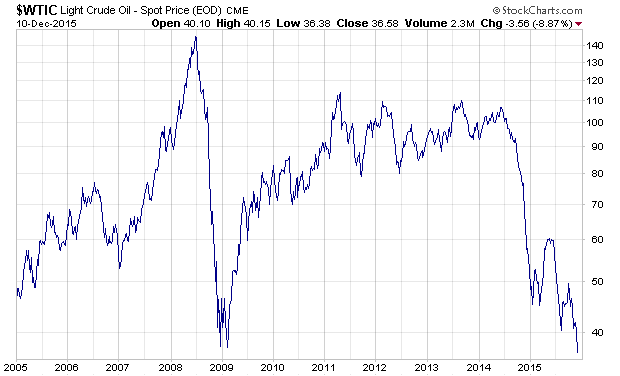

The Decline and Fall of OPEC

Last Friday, OPEC held a meeting in Vienna, and it may go down in history. At the meeting, the cartel essentially decided to abandon any production quotas. If a cartel can’t or won’t prop up prices, then it’s really not much of a cartel.

Going into the meeting, we knew that OPEC members were cheating anyway. The meeting just made de facto de jure ‘cause de oil is gonna be pumped no matter what.

But I wouldn’t be so quick to declare OPEC dead. It’s still big and very influential. There’s also the issue of Iranian oil coming back on line at some point. The giant, as always, is Saudi Arabia, and if they wanted to, they could unleash a massive supply of oil onto the world. We’re seeing a rift grow between the core members of OPEC and the more marginal players (like Ecuador or Venezuela, which I always forget are in OPEC.) The marginal players are losing—and badly. Last weekend, voters in Venezuela gave the socialist government there a crushing defeat.

In the U.S., the junk-bond market is closely tied to oil production. As oil has fallen, junk-bond spreads have increased. There could be a lot of defaults coming soon. Speaking of the junk bond market, Jeffrey Gundlach recently said, “I don’t like things when they go down every single day.” It’s as if it’s 2008 all over again, but just in the energy patch.

Lately, however, there are signs that the weakness in junk bonds isn’t solely about oil, and it may be spreading to other areas. Some bears are latching onto this as an omen of bad times, and they think higher rates from the Fed will make things even worse. One junk bond fund just blocked investor withdrawals. I’m concerned about a breakdown in the high-yield sector, but I’m not alarmed just yet.

Oracle’s Earnings Preview

Oracle (ORCL) is due to report its fiscal Q2 earnings after the market closes on Wednesday, December 16. Wall Street currently expects earnings of 60 cents per share which is down from 69 cents for the same quarter last year.

The strong dollar has clobbered Oracle’s earnings recently. I expect to see more of the same for Q2. Oracle was late to the game in the cloud business, but they’ve been trying to close the gap.

Oracle has been going through a tough transition period. We’ve probably just passed the low point (Q4 was a total disaster). Bookings have been strong for Oracle, and I think we’ll see much better results from them in the future.

The company said it sees Q2 earnings ranging between 63 and 66 cents per share and revenue (in constant currency) coming in between -1% and +2%. But they project cloud growth of 50%. I recently listed Oracle as one of the stocks I’m considering dropping next year. I hope to see strong signs of improvement here.

Stryker Raises Dividend by 10%

On Thursday, Stryker (SYK) announced that it’s bumping up its dividend by 10%. I love it when good companies reward their investors. SYK’s quarterly dividend will rise from 34.5 cents to 38 cents per share.

From the press release:

“As part of our capital-allocation strategy, we are committed to consistent growth in our dividend, which is reflected in the announced 10% increase for 2016,” said Kevin. A. Lobo, Chairman and Chief Executive Officer. “We will continue to utilize our balance sheet for acquisitions that support our growth goals, dividends and share repurchases to help drive shareholder value.”

The annual dividend adds up to $1.52 per share. Based on Thursday’s close, that works out to a yield of 1.64%. Since 1991, Stryker has increased its dividend by 243-fold. Stryker remains a buy up to $101 per share.

Buy List Updates

As we head toward the close of 2016, I want to make a few adjustments to our Buy Below prices. This week, I’m raising the Buy Below on Ross Stores (ROST) to $56 per share. By the way, I think Ross will have little trouble beating its guidance for Q4.

I’m also raising my Buy Below on Microsoft (MSFT) to $58 per share. The stock made its all-time high in the closing days of the last millennium. I think there’s a good chance MSFT will make a new all-time high very soon.

Ball (BLL) has been on a roll (sorry). The company looks like it will win approval from the EU for the Rexam deal. Since September 29, shares of BLL are up nearly 20%. Interestingly, Ball is floating euro-denominated bonds to finance the deal. For now, I’m keeping my Buy Below on Ball at $70 per share.

I also want to lower my Buy Below on Cognizant Technology Solutions (CTSH). Don’t worry. I don’t think any less of CTSH. I just want to align the Buy Below better with the current price. The company has been doing very well lately. You may want to check out this recent Bloomberg article on Cognizant’s efforts to go after IBM in consulting. I rate Cognizant a buy up to $65 per share.

That’s all for now. Next week will be all about the Federal Reserve. The Fed meets on December 15-16. The policy statement will be released at 2 p.m. ET on Wednesday. Yellen’s presser will follow. On Tuesday, the government will release the CPI report for November. There’s a good chance that trailing core inflation hit 2%. That hasn’t happened in a while. Oracle will report its earnings after the market closes on Wednesday, December 16. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on December 11th, 2015 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His