CWS Market Review – July 1, 2016

The market is fond of making mountains out of molehills and exaggerating

ordinary vicissitudes into major setbacks.” – Benjamin Graham

As I wrote last week’s CWS Market Review, I was keeping a close eye on the Brexit referendum results from our cousins across the pond. Going into Election Day, the Remain camp appeared to have a slight lead. Once the polls closed, the media reported that it was too close to call, and that’s what I assumed as I wrote last week’s newsletter.

However, as soon as I instructed my valet to press “send” and email the newsletter to you, things started to change—and they changed dramatically. The Leave side gained momentum. Soon it became apparent that a majority of British voters wanted out of the European Union. Wow!

The Brits Vote to Leave the EU

This was a shock to the global political establishment—and to global financial markets. Last Friday, European markets plunged. The British pound dropped from $1.50 to a three-decade low of $1.32 (see below). All hell broke loose in England’s green and pleasant land. David Cameron said he’ll resign as Prime Minister. The Labour Party faces an internal revolt as well.

I started off last week’s issue talking about how calm things had become (ha!) and about how the S&P 500 hadn’t had a 1% drop in 54 days. Clearly, I jinxed it. On Friday, the S&P 500 lost 3.17%. That was its biggest drop in nearly a year.

All across the world, investors dumped stocks and ran to the safety of conservative assets. The U.S. dollar soared. So did the Japanese yen. The yield on the 10-year Treasury approached its lows from four years ago, which were the lowest yields since 1790!

Oh, and the idea of a Fed hike? As my New York friends like to say, “fuggedaboutit!” The Fed’s not going to do anything anytime soon. I don’t think we’ll see a rate increase this year. There’s even talk that the Fed’s next move would be a rate cut (which I strongly doubt).

The selling continued into Monday, and soon we heard dire predictions of what lay ahead. Britain was headed towards recession! Other countries were going to abandon Europe! Trade protectionism would sweep the developed world! The S&P 500 lost another 1.81% on Monday and closed a fraction above 2,000.

Then what happened? Everything reversed itself. The U.S. stock market rallied strongly on Tuesday, Wednesday and Thursday. The index gained more than 1% for three days in a row. A number of our Buy List stocks like AFLAC, CR Bard, Fiserv and Stryker broke out to new highs. By the closing bell on Thursday, the S&P 500 gained back 88% of what it lost.

In fact, if you had completely ignored the market from last Thursday’s close to yesterday’s close, you probably would have assumed not much happened. The index lost a scant 0.68% over that time. For a one-week period, that’s no biggie. Sure, a lot happened during that time, but you get my point.

I often tell investors that investing is unlike any other activity. Imagine if you went to a tennis instructor for tennis lessons and the instructor told you that the best way for you could improve your game would be to immediately stop playing tennis, put your racket in storage and don’t even think about tennis. You might think the instructor had lost his marbles. Yet, as odd as it sounds, that advice is quite sound for investing. The less you try, the better you’ll do. Not panicking last week was a wise move, yet it’s simply too hard for so many.

Markets are instruments that process information. That means they tend towards short periods of freaking out and long periods of not doing much. Last Friday and Monday were freak outs. The world assumed the British would vote to stay in the EU, and the world was wrong. That happens. The selling was exaggerated because the areas seen to benefit from a Remain victory had been rallying.

I can’t claim any foresight. I thought the Remain side would pull it out as well. The difference is that our strategy of focusing on high-quality stocks isn’t dependent on a particular election outcome. We’re prepared for whatever comes our way. Actually, some of the immediate effects, like a stronger yen, will help our portfolio. AFLAC (AFL) closed out Thursday at a new all-time high.

What’s the Impact of Brexit?

So what does all this mean for our portfolio? That’s a difficult question to answer, but I think the long-term effect will be minor. Remember that we’re hearing people who didn’t see this vote coming now confidently predicting what it all means.

Most importantly, this is almost purely a financial matter. Let me explain. There are really two economies. There’s the “production economy,” which consists of people going out and building things or providing services for people. That’s the real economy. Then there’s the make-believe economy, also known as the financial economy, which consists of people in expensive suits who trade pieces of paper.

The two economies are related to each other, but sometimes that relationship can appear to be rather distant. The stock for any particularly company can move sporadically, even though the company’s operations are as stable as ever.

In the case of Brexit, we’re talking about an event firmly based in the world of the financial economy. Many European banks dropped sharply on hearing the news, and many American banks did poorly as well, including our own Wells Fargo (WFC) and Signature Bank (SBNY). That’s probably due to the belief that interest rates are going to stay low. Long-term bond yields have been closely correlated with the relative strength of financial stocks, meaning bonds and banks are moving in opposite directions.

If I ran a London-based investment bank that many clients used as an entryway to the European economy, then I suppose I’d be very concerned about the future implied by Britain’s not being in the EU. Since I don’t, and since our Buy List doesn’t reflect anything like this, I can’t say I’m terribly worried about Brexit. I would be more concerned by a larger wave of voters protesting free trade, but that doesn’t appear to be a major concern. In fact, many in the Leave camp stressed that they’re not opposed to trade or immigration. Rather, the issue for them is their own parliament, not Brussels, deciding such matters.

I think it’s interesting that the major British stock index, the FTSE 100, is actually higher than where it was before the vote. Some of that, of course, is due to the weakening of the British pound. Even on Friday, shares of Hormel Foods (HRL) closed higher. HRL rallied on Monday as well. We are truly playthings for the market gods.

The Buy List at the Halfway Mark

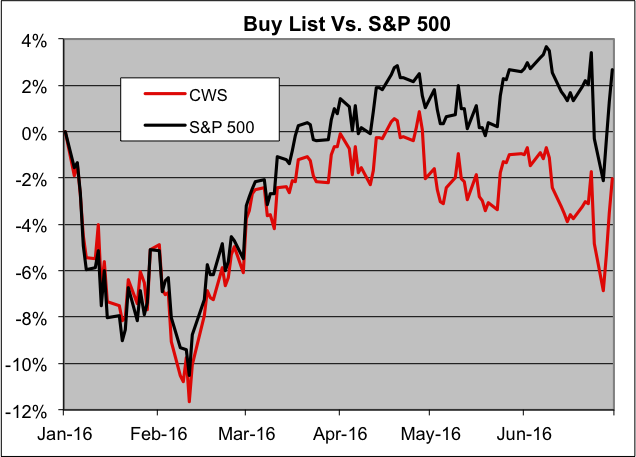

The first half of 2016 is now over. I’m afraid to say that our Buy List has lagged the S&P 500 during the first half of this year; however, it’s not doing that poorly.

For the first six months of 2016, our Buy List is down 2.04%, while the S&P 500 has gained 2.69% (see below). Once we include dividends, our Buy List is down 1.45%, while the S&P 500 is up 3.84%.

What did we do wrong? Nothing really. The issue is that the stock market reversed course in early February. That rally has been led by many cyclical stocks and “high-beta” stocks, which are underweighted on our Buy List. For example, the Energy Sector ETF (XLE) is up more than 30% from its February low. Our Buy List doesn’t have any energy stocks, so we haven’t enjoyed a bounce like that. On the other hand, we never suffered a 50% crash as the XLE did in the 20 months prior to that.

Underweighting those sectors wasn’t a strategic decision. I just didn’t see that many bargains there. I’m still optimistic for our Buy List for the remainder of this year. The only stock that I’m leaning toward regretting is Bed Bath & Beyond (BBBY). But even that one is so cheap, we might as well stick with it.

Stryker (SYK) is our #1 winner so far this year, with a YTD gain of 28.93%. In the cellar is Alliance Data Systems (ADS), with a loss of 29.16%. Earlier this year, ADS dropped 19% in one day.

I always try to be up front about our track record. While the first half has been disappointing, I’m looking forward to better second half of 2016.

Buy List Updates

Despite the market’s drama of the past week, there hasn’t been much news impacting our stocks. One big story is that Wells Fargo (WFC) passed the Fed’s latest stress test. The bank is pretty solid, and it’s never had much trouble passing muster with the Fed.

Now that Wells’s capital plan has gotten its gold star from the Fed, the bank is free to raise its dividend. Wells has been, by far, the most generous of the major banks. Last year, WFC paid out 75% of its net income as dividend or share buybacks.

In April, the bank raised its quarterly dividend by half a cent, from 37.5 to 38 cents per share, but that was under last year’s capital plan. The board said it’s going to meet to decide what to do with the dividend. Wells Fargo is due to report Q2 earnings on July 15, two weeks from today.

In last week’s issue, I mentioned how the rising yen is good news for AFLAC (AFL). I wrote, “there’s talk of it soon breaking 100.” By soon, I apparently meant a few hours. Thanks to this week’s chaos, investors rushed to buy safe-haven assets like the yen. At one point, the yen got to 99 to the dollar. It’s since settled back at 103. That’s an impressive rally. Late last year, the yen had been going for 123 to the dollar. AFL closed Thursday at $72.16, which is a new all-time high. The company will report earnings again on July 28.

That’s all for now. The stock market will be closed on Monday in honor of July 4. Next week, the Fed will release the minutes of its last meeting. I suspect that much of that discussion is already out of date, but it will be interesting to hear what the central bank said. On Thursday, we’ll get the latest initial-claims report, plus the ADP payroll report. That leads us up to the big June jobs report on Friday. The last jobs report was a major disappointment. I’ll be curious to see if some of those numbers will be revised. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on July 1st, 2016 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His