CWS Market Review – August 10, 2018

“People calculate too much and think too little.” ― Charlie Munger

Earnings season has finally passed for us. It felt like the last few issues were just me reading off numbers to you: “So-and-so reported X cents, beat by Y and raised Z cents.” Despite all the math, earnings season is crucial for us, and it gives our strategy a moment to shine.

I’m happy to say that our Buy List has been doing very well lately. This week, we hit a new all-time high. We’re up 6.2% for the year, and we’ve already taken out our January peak, while the S&P 500 hasn’t quite done the same (though it’s getting very close). Going back to May 3, our Buy List is up 9.64% compared with 8.51% for the S&P 500.

Several of our stocks, like Ross Stores (ROST), Fiserv (FISV), Becton, Dickinson (BDX) and AFLAC (AFL), are at or near new 52-week highs. In this week’s issue, I want to change course and talk more about the economy and the general investing climate. The good news is that it looks very good for us. Let’s dig in and start with last week’s jobs report.

The Economy Is Good, Not Great

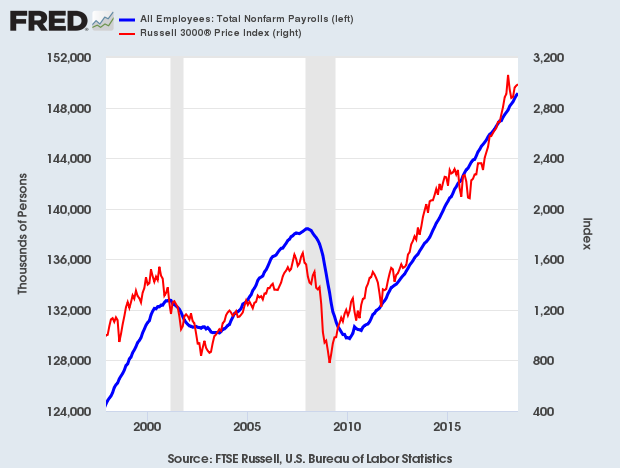

Last Friday, the government reported that the U.S. economy created 157,000 net new jobs for the month of June. That’s a decent figure, although it was below expectations. It means the jobs machine continues to plow on, past when many people thought it would peter out. The unemployment rate ticked down to 3.9%. The unemployment rate is lower now than it was for every single month from 1970 through 1999.

It’s true: the economy is doing well. Please understand that I mean that in a strict macroeconomic sense. Of course, lots of people are having a hard time. I don’t mean to imply that we’re on easy street. By a “strong economy,” I mean that in the aggregate, economic activity is expanding. I don’t have the final number on the Q2 earnings season, but the earnings beat rate was running over 80%, and the revenue beat rate was running at over 70%. That’s very good. Earnings were up over 20% compared with last year’s Q2.

We can see evidence in the government reports as well. The initial report on Q2 GDP showed an increase of 4.1%. That’s pretty good. Jobless claims continue to be near 50-year lows. The stock market is moving up, and the U.S. dollar is strong. What’s also interesting is that the breadth of the stock market is improving. It’s not just the FAANG stocks, but more and more smaller guys are joining the party.

It’s important that we keep an eye on interest rates. Last week, the Fed decided to leave rates alone. That was the right call, but they’ll almost certainly raise rates again in September. It won’t end there. The futures traders are betting that we’ll get another hike in December. Personally, I’m not so sure of that, but I’m open to being convinced. The recent remarks from Fed officials have stressed the need to move on rates before inflation starts to spark higher. The Fed always overshoots on rates. That’s not my opinion. It’s a well-established historical fact.

The Problem Is Wages

We should also remember that the Fed isn’t raising rates from normal to high. Instead, we’re going from very, very, very low to somewhat moderate. It’s just that we haven’t been in this range in a long time, so the change may feel larger than it is. Still, short-term interest rates are running below inflation. It’s been that way for 10 consecutive years.

The problem for the Fed is the troubling detail that appeared in last week’s jobs report, and that’s wages. Americans are seeing their pay growing, but after inflation, it hasn’t amounted to much. That’s frustrating to see. Of course, higher wages mean more shopping, and that means more profits. The improved earnings have actually lowered stock valuations over the last few months. (I wonder how many people realize that.)

This economy has been quite good for companies like Ross Stores (ROST) which focuses on bargain-sensitive consumers. The deep-discounter just made another 52-week high.

We’re also seeing renewed strength in some cyclical stocks. These are the sectors whose fortunes are mostly closely tied to the economic cycle: construction, railroads, steel, chemicals—stuff like that. On our Buy List, we’ve been getting big gains lately from our cyclicals. Later on, I’ll talk about the big rally in our wallboard company, Continental Building Products. Wabtec (WAB), our freight-services stock, is doing very well this year. Sherwin-Williams (SHW) started out poorly for us but has made an impressive turnaround.

As long as consumer spending and the housing market remain healthy, the economy will continue to chug along. A lot of people have asked me if the growing trade war will sink the economy. My answer is that it’s bad for the economy but probably not severe enough to trip things up. Among major economies, the U.S. is one of the least trade-intensive.

I would caution investors against being too heavily weighted towards technology stocks. We have some good ones on our Buy List. Check Point Software (CHKP), for example, has done well for us. It’s OK to have some tech stocks, but I don’t like the prices I’m seeing out there. Be careful not to be over-exposed.

I’d also urge investors not to forget dividends. We have lots of solid dividend-payers on our Buy List. Smucker (SJM), for example, now yields over 3%. Last month, the jelly folks raised their dividend by 9%. It was their 17th annual increase in a row.

AFLAC (AFL) has increased its dividend for 35 years in a row. Look for #36 in October. Going by Thursday’s close, the duck stock yields 2.22%. That’s equivalent to 567 points on the Dow, and you basically get that for just showing up.

It’s important not to chase stocks. Wait for good stocks to come to you. Make sure you’re well diversified, and pay attention to our Buy Below prices. Now here are some updates on our Buy List stocks.

Buy List Updates

In last week’s issue, I mentioned the excellent earnings reports from Continental Building Products (CBPX). However, the stock reported after the close on Thursday, and I wasn’t sure how the market would respond.

Well, now we know. The stock soared. CBPX gained more than 8% on Friday and then another 4.5% on Monday. It gained ground on Tuesday, Wednesday and Thursday as well. In the last week, the CBPX is up 18%. It’s now our second-biggest winner on the year (+32.5%), trailing only Wabtec (+36.9%). This week, I’m lifting my Buy Below on Continental Building Products to $40 per share.

In our last issue, I also discussed the good earnings report and higher guidance from Becton, Dickinson (BDX). The stock, however, dipped down 4% on the morning of the earnings report. I decided it was best to keep our Buy Below at $250 per share. That seemed like a nice, round number.

Well, the market kept to its trend. Not only did Becton make up the 4% loss, but it continued to rally past $250 and hit a new high. This is a really good company, and I don’t want investors to be left behind. That’s why this week, I’m bumping up our Buy Below to $260 per share.

While the big wave of earnings reports has passed us, we have three Buy List stocks with quarters that ended in July. They will be reporting earnings soon. JM Smucker (SJM) will report earnings on Tuesday, August 21. Ross Stores (ROST) and Hormel Foods (HRL) will report on Thursday, August 23. I should add that Ross has been acting very well lately. It’s up almost 15% this year. After those reports, we enter the quiet period for earnings reports. For nearly two months, only FactSet (FDS) and RPM International (RPM) will report. After that, the third-quarter earnings season will get underway in mid-October.

One other note on FactSet. Merrill Lynch said this week that it’s ditching Thomson Reuters as its primary data source and will now be using FactSet. That’s very good news. Merrill has 15,000 advisers. FDS jumped nearly 5% on Monday. I’m lifting our Buy Below on FactSet to $219 per share.

We also had good news from Fiserv (FISV). The board has authorized the company to buy back 30 million shares of stock. That’s about 7.5% of their outstanding shares. The stock broke out to another new high, and it’s a 20% winner for us this year.

That’s all for now. No Buy List earnings reports next week, but there are some key events to look out for. On Wednesday, we’ll get reports on retail sales and industrial production. The IP numbers have been looking better lately. On Thursday, we’ll get reports on housing starts and jobless claims. The jobless-claims numbers are still very close to the best figures since the 1960s. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Syndication Partners

I’ve teamed up with Investors Alley to feature some of their content. I think they have really good stuff. Check it out!

Buy These 3 REITs Thanks to the U.S. Supreme Court’s Internet Tax Ruling

In June, the U.S. Supreme Court reversed earlier tax rules to allow states to collect sales from online vendors who do not have a physical presence in a state. Before the ruling, a lot of Internet sales did not include the collection of sales taxes, giving online vendors a price advantage over local brick-and-mortar retailers. With the ruling, that advantage has been eliminated. The retail apocalypse has been postponed and now is a good time to pick up shares of high quality retail focused REITs.

The result of the fake “retail apocalypse” and the recent U.S. Supreme Court ruling is that now is a great time to pick up shares of mall and shopping center focused REITs. Here are three to consider.

This 8.5% High-Yield Stock Could See Its Share Price Jump 50%

In the IPO world, new biotech or consumer tech stocks get all the attention. The financial news keeps close track of how much a new tech IPO climbs the first few days after a public market launch. This makes great news bites, but it is hard for individual investors to participate. IPOs in the high-yield stock world get little or no attention. I make a point of finding and tracking new dividend stocks, and then recommending them to my subscribers when my analysis confirms attractive total return potential.

One such stock has returned 50% since I made the first recommendation last fall. The 2018 second-quarter earnings show that the positive run still has plenty of room to grow.

Posted by Eddy Elfenbein on August 10th, 2018 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His