CWS Market Review – June 7, 2019

“Go for a business that any idiot can run—because sooner or later,

any idiot probably is going to run it.” – Peter Lynch

My friend and blogger extraordinaire Josh Brown has a clever way of describing the relationship between the economy and the stock market. He says to think of a woman walking a dog through a park. The woman is walking in a clear path, while the dog lurches all around.

The woman is like the economy. She’s following a steady path. Meanwhile, the dog is like the stock market. It’s erratic and jumping back and forth, but ultimately, the dog arrives at the same destination as the woman.

That metaphor has come to mind lately as we’ve experienced a temper tantrum in the financial markets, while the actual economy remains quite stable. The bond market is soaring, and the stock market is dropping. In this week’s CWS Market Review, I’ll explain what it means for us and our investments.

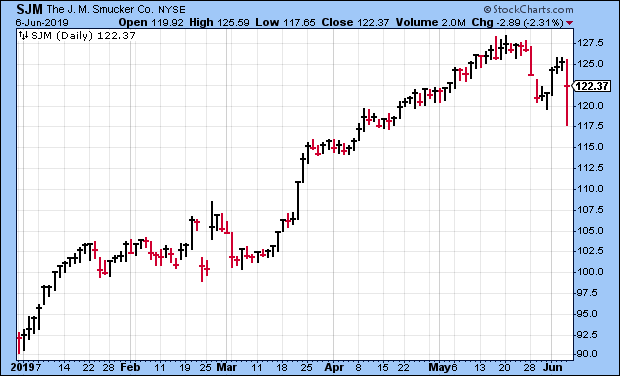

Speaking of which, we just had a very good earnings report from JM Smucker. The jam folks topped Wall Street’s estimates by 13 cents per share. Smucker also had good guidance for the coming year. SJM is now a 30.9% winner for us this year. Before we get to that, let’s take a look at the financial market’s latest freak out.

Will the Fed Come to Wall Street’s Rescue?

Late last year, the stock market threw a hissy fit when the Federal Reserve stuck by its plans to raise interest rates. The central bank was planning to raise rates three times in 2019. Traders didn’t like that at all. Between September and December, the stock market tanked.

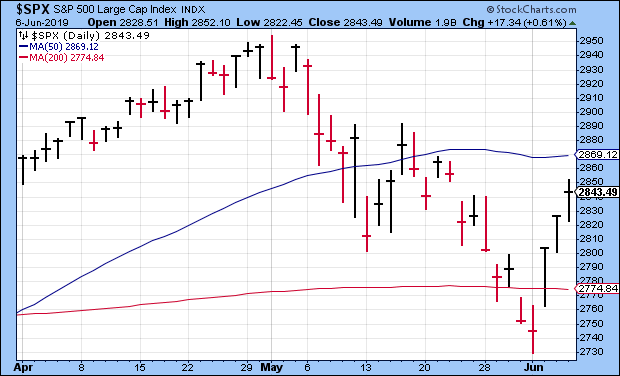

The Fed eventually got the message and backed off. The stock market snapped back quickly. It rallied much faster than I had expected. Now we’re in the spring, and the stock market is unhappy again. The major indexes took a bath during May. The selling really got going after a pair of tweets from President Trump escalated the Trade War with China.

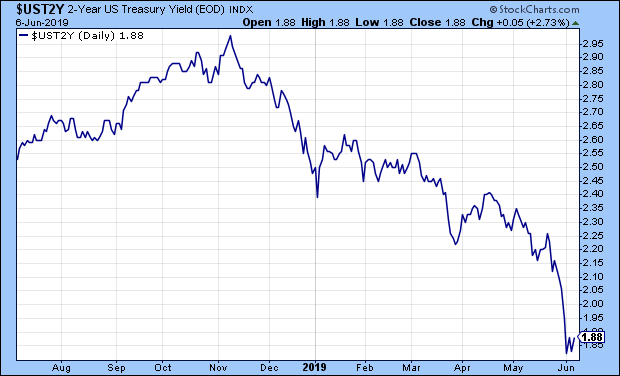

Will the Fed come to the rescue again? That’s what the bond market thinks. In anticipation of rate cuts, the yield on the two-year Treasury has fallen off a cliff. The two-year is often a decent proxy for Fed policy. It fell from 2.26% on March 21 to 1.82% this past Monday. That’s a big move for such a short amount of time.

The futures market agrees. The Fed funds futures now thinks the Fed will cut rates at its July meeting, and again at its September meeting. This is a huge about-face from a few months ago. In fact, the futures are split on the odds of a third rate cut in December. This has led to the yield curve becoming partially inverted. Of course, with rates already so low, the Fed doesn’t have much room to cut rates.

Will the Fed take the bait? I’m a skeptic. Central bankers don’t like big dramatic moves, and Chairman Jay Powell is a cautious guy. Without much data indicating that a rate cut is needed, I don’t see the Fed making a move. Just because the market is getting the shakes doesn’t mean the Fed’s going to change course. In the Fed’s mind, they already placated Wall Street by calling off the rate hikes. But now Wall Street wants rate cuts? I doubt it.

I’m in the minority here, but Wall Street is getting way ahead of itself. I’ll give you an example. Recently, Chairman Powell made some perfectly anodyne remarks about the Fed being ready to “act as appropriate to sustain the expansion.” Big deal. All Fed officials say stuff like that. But Wall Street completely overreacted and interpreted the remark as meaning the Fed is ready to pivot. That was enough to spark a relief rally this week.

That leads me back to our original metaphor. The financial markets (the dog on the leash) are frightened that we’re headed to recession meaning that the actual economy (the lady walking the dog) has shown very few signs of trouble.

Sure, this week’s ISM Manufacturing report came in a little light, but it wasn’t that bad. Some other data have been soft, but consumer confidence remains high. The jobless claims reports have been pretty good. Also, mortgage rates are down, so that will help the housing sector. But listening to the financial markets, you’d think the economy is plunging into the abyss.

Not only that, but it’s the kinds of stocks that have taken a beating that’s interesting. The pain has mostly been felt among more aggressive, cyclical stocks. For example, tech stocks have been down. Also, energy stocks are lagging badly. The small-cap Russell 2000 has fallen way behind.

This rotation has been great news for our Buy List stocks. On Thursday, our Buy List closed at a high for this year. This is especially impressive since the S&P 500 is still 3.5% below its high from a few weeks ago. We’re now up 18.4% so far in 2019. That’s 5% better than the S&P 500 (not including dividends).

On Thursday, seven of our stocks hit new 52-week highs: AFLAC (AFL), Cerner (CERN), Church & Dwight (CHD), Danaher (DHR), FactSet (FDS), Hershey (HSY) and Intercontinental Exchange (ICE).

The past few weeks have been excellent for our investing style. The reason is that Wall Street has gotten nervous that a trade war will sink the economy. For the most part, that doesn’t impact our stocks that much. Over the last five weeks, the high-volatility sector has been toast, and we’ve been fine. Apple and Facebook are both down more than 20%, and Google is down 19%. Now let’s look at a surprising winner for us this year.

Smucker Is a Buy up to $130 per Share

On Thursday, JM Smucker (SJM) reported fiscal Q4 earnings of $2.08 per share. Smucker ends its fiscal year on April 30. That’s why we get the earnings report at an odd time.

Overall, this was a solid quarter for SJM. First, some math. Previously, Smucker had given us full-year guidance of $8.00 to $8.20 per share. For the first nine months of the fiscal year, the company had made $6.20 per share. That implies an estimate for Q4 of $1.80 to $2.00 per share. Wall Street had been expecting $1.95 per share.

Whichever number you take, Smucker did much better than estimates. The company also provided guidance for the current fiscal year which is fiscal 2020. Smucker expects sales growth of 1% to 2%. The company expects earnings to range between $8.45 and $8.65 per share. That’s a bold forecast. Wall Street had been expecting $8.33 per share.

Sales growth was a bit weaker than expected. For the quarter, net sales rose 6.8% to $1.90 billion. Wall Street had been expecting $1.93 billion. Like other consumer companies, Smucker has been cutting prices. For the quarter, gross margins fell 2.4% to 36.4%. On the plus side, the pet-food business is doing well. (Yes, Smucker is a lot more than jelly.)

CEO Mark Smucker said:

“We are pleased with the progress that we made during the year towards executing against our strategic plan, which supported fourth-quarter adjusted-earnings growth of 8 percent and full-year adjusted-earnings growth of 4 percent. We successfully integrated Ainsworth, extending our leadership in pet foods, while our key growth brands delivered double-digit sales growth, demonstrating the power of our brands when supported by ongoing product innovation, including 1850® coffee and Jif Power Ups®. We continued to focus on productivity, allowing us to deliver on our cost reduction targets for the year, providing fuel for investment in future growth.”

“As we transition to fiscal year 2020, our organization is committed to delivering on its growth imperatives to lead in the best categories, build brands consumers love, and be everywhere our consumers want us to be. Disciplined investment in our brands across pet food, coffee, and snacking leaves us well-positioned to drive sustainable financial growth and enhance shareholder value for the long term.”

The stock initially dropped 6.1% after the earnings report, but it eventually closed down 2.3%. We have little reason to complain. SJM has been a big winner for us this year. This week, I’m lifting my Buy Below on Smucker to $130 per share.

Buy List Updates

Cerner (CERN) said it’s paying a dividend of 18 cents per share. This is important because it will be Cerner’s first-ever dividend. Impressively, the dividend is 20% higher than the estimate Cerner gave in February.

The new dividend is being paid after Cerner reached a deal with Starboard Value, an activist investor. The dividend will be paid on July 26 to shareholders of record of June 18. It’s not a lot, but it’s good to see. I’m raising my Buy Below on Cerner to $76 per share.

Last month, Church & Dwight (CHD) released a pretty good earnings report. The consumer-products company beat estimates by four cents per share. I was pleased to see gross margins increase by 20 basis points to 45.1%. Operating margins rose 120 basis points to 23.1%.

The company reiterated its full-year EPS guidance of $2.43 to $2.47. That’s an increase of 7% to 9% over last year. For Q2, CHD expects earnings of 52 cents per share, which matches the Street. After the earnings report, I thought of raising my Buy Below price, but I decided against doing so. The shares have performed well recently and touched a new 52-week high on Thursday. I’m raising my Buy Below on Church & Dwight to $82 per share.

That’s all for now. The May jobs report will be out later this morning. Next week, we’ll be getting some important economic reports. On Monday, we’ll get the job-openings report (JOLTS). The CPI report comes out on Wednesday. I’ll be curious to see if there are any price pressures building in the U.S. economy. Then on Friday, we’ll get the retail-sales report and the report on industrial production. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on June 7th, 2019 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His