CWS Market Review – July 5, 2019

“The laws of probability, so true in general, so fallacious in particular.”

– Edward Gibbon

The trading week was shortened by the July 4th holiday. As a result, there wasn’t much news. Sensing this, many Wall Street big shots took off for the Hamptons, causing the usual financial frenzy to be cut short.

I want to take advantage of this lull in market news to summarize our Buy List at the midpoint of the year. I’m happy to report that our Buy List is doing quite well this year.

We also had a somewhat poor ISM report on Monday. This could be further evidence that the Fed will cut rates at its meeting later this month. I’ll review the latest numbers. But first, let’s look at how well our Buy List is doing in 2019.

Our Buy List Is Up 23.21% This Year

I’ll be honest: at the start of the year, I would not have guessed that stocks would do so well in 2019. Fortunately, we always stay in the market and so don’t miss out on any unexpected surges.

The stock market closed early on Wednesday and was closed all day on Thursday. At the closing bell on Wednesday, the S&P 500 reached 2,995.82. That’s another all-time high.

For some context, the index first broke 300 in 1987. The old version of the index broke 30 in 1929. We may break 3,000 any day.

Now let’s look at some numbers. Through Wednesday, our Buy List is up 22.48% on the year compared with 19.51% for the S&P 500. Including dividends (and I always include dividends in our final calculation), we’re up 23.21% while the S&P 500 is up 20.75%.

Our “beta” is running at 0.800 which is bit low compared with previous years (in reality, I don’t pay much attention to it). There’s been a 90.1% correlation between the daily changes of our Buy List and those of the S&P 500.

Our Buy List generally yields about 1%, which is about half the yield of the S&P 500. I don’t plan it this way, but that’s usually how it works out. We’re running a little higher this year.

Twenty of our 25 stocks are up this year. The biggest winner by price percentage is FactSet (FDS). FDS is currently up 47.93% for us this year. Moody’s (MCO) isn’t far behind at 44.68%.

We have four positions up more than 40%, and seven are up more than 30%. Fourteen of our stocks are up, beating the market this year. Sherwin-Williams (SHW) is just a tiny bit behind. Our worst stock this year is Hormel Foods (HRL). The Spam stock is down just over 2%. On Thursday, eight of our Buy List stocks touched new 52-week highs.

Our sells from last year aren’t doing that well. Alliance Data Systems is down 2% this year. Ingredion is off by 8%. Snap-on is up 12%. Wabtec is up by 5%. Carriage Services is the big winner with a 22% gain.

Our most dramatic stock this year has been Cognizant Technology (CTSH) which dropped 18% over the course of two trading sessions. It’s still up a bit for us this year. Due to broad diversification, the drop didn’t shake our portfolio much.

I nearly forgot the most important part—we didn’t make a single trade all year. Yet we still beat the market, and we did it with lower volatility.

Here’s a look at how each stock has done, along with its dividend-adjusted gain.

| Symbol | 31-Dec | 3-Jul | Gain | Adj Gain |

| AFL | $45.56 | $56.85 | 24.78% | 26.11% |

| BDX | $225.32 | $255.24 | 13.28% | 14.00% |

| BR | $96.25 | $131.85 | 36.99% | 38.14% |

| CPBX | $25.45 | $26.08 | 2.48% | 2.48% |

| CERN | $52.44 | $74.53 | 42.12% | 42.48% |

| CHD | $65.76 | $75.04 | 14.11% | 14.86% |

| CHKP | $102.65 | $119.47 | 16.39% | 16.39% |

| CTSH | $63.48 | $64.18 | 1.10% | 1.71% |

| DHR | $103.12 | $145.31 | 40.91% | 41.27% |

| DIS | $109.65 | $142.98 | 30.40% | 30.40% |

| EGBN | $48.71 | $54.23 | 11.33% | 11.77% |

| FDS | $200.13 | $296.06 | 47.93% | 48.73% |

| FISV | $73.49 | $94.23 | 28.22% | 28.22% |

| HRL | $42.68 | $41.77 | -2.13% | -1.16% |

| HSY | $107.18 | $138.00 | 28.76% | 30.31% |

| ICE | $75.33 | $88.59 | 17.60% | 18.42% |

| MCO | $140.04 | $202.61 | 44.68% | 45.49% |

| ROST | $83.20 | $100.00 | 20.19% | 20.85% |

| RPM | $58.78 | $62.30 | 5.99% | 7.30% |

| RTN | $153.35 | $173.45 | 13.11% | 13.70% |

| SBNY | $102.81 | $123.97 | 20.58% | 21.62% |

| SHW | $393.46 | $470.16 | 19.49% | 20.12% |

| SJM | $93.49 | $119.73 | 28.07% | 29.99% |

| SYK | $156.75 | $208.15 | 32.79% | 33.49% |

| TMK | $74.53 | $91.63 | 22.94% | 23.69% |

| Buy List | 22.48% | 23.21% | ||

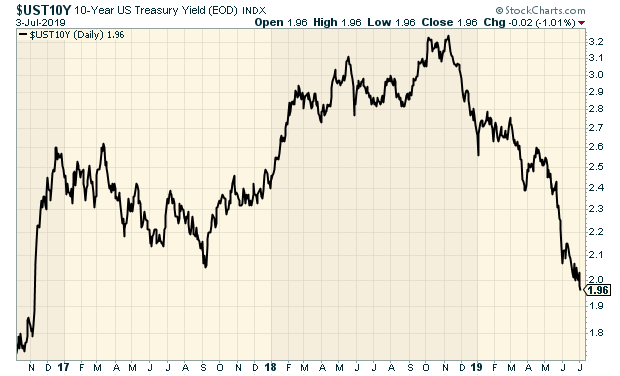

The 10-Year Yield Drops Below 2%

On Monday, the ISM report for June came in at 51.7. That’s the lowest since October 2016. Then on Wednesday, the ADP payroll report came in light. That helped send the 10-year Treasury down to 1.96%. That’s the lowest yield since late 2016.

We’ll learn more about the state of the economy in the jobs report, which is coming out later today. Wall Street seems convinced that the Fed will cut rates at the end of this month. I can’t say I share their certitude.

I need to make a correction to last week’s issue. Danaher (DHR) shareholders will not get shares of Envista, the dental spinoff. Instead, it will IPO and Danaher will retain a position. In effect, we’ll still own it, but only via DHR.

That’s all for now. The June jobs report is due out later today. Next Tuesday, Jerome Powell will be speaking at a Fed conference on stress testing. We might get clues as to what the Fed is thinking on the economy. Folks pay careful attention to every remark he makes. Then on Thursday, the CPI report for June is released. We’ll also get an update on the budget for this year. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on July 5th, 2019 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His