CWS Market Review – March 6, 2020

“The stock market is going to fluctuate. Sometimes it will fluc down; other times it will fluc up.” – Louis Rukeyser

In last week’s issue, I wrote, “I think there’s a good chance the Fed will cut rates before the next meeting.”

Sure enough, that’s exactly what happened. On Tuesday, the Federal Reserve cut interest rates by 0.5% two weeks before its scheduled meeting. And the market responded…by falling flat on its face. The S&P 500 fell by 2.8%, which came after one of the market’s best days in decades.

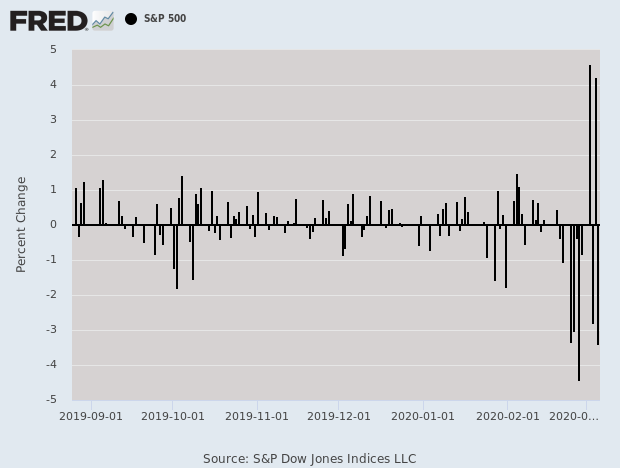

So how come a rate cut didn’t work? Well, as much as we hope, low rates won’t cure any virus. Simply put, the market is on edge right now. It’s hard to state just how volatile the market has become. It hasn’t been like this in years. Check out the daily changes for the S&P 500.

Consider some stats. The S&P 500 has now closed up or down by more than 2.5% for four straight days. It hasn’t done that in more than eight years. At one point, the S&P 500 closed up or down by more than 4% three times in five days. In the eight years prior to that, it happened just twice. (For that last stat, Brian Sullivan gave me a shout-out on CNBC.).

Trading Nation and @EddyElfenbein got a shout-out from @SullyCNBC on tonight's @CNBCFastMoney. Aw, shucks. pic.twitter.com/QWEW9fDxdX

— Trading Nation (@TradingNation) March 4, 2020

In this week’s issue, I’ll break down what’s happening, and more importantly, I’ll tell you how to position yourself. But I’ll warn you, it’s very likely we’re not done just yet. I’ll also update you on this week’s earnings report from Ross Stores. The deep-discounter beat earnings and hiked its dividend, but guidance wasn’t so hot. I’ll have more on that in a bit. But first, let’s look at the Fed’s surprise rate cut.

The Fed Cuts Rates and the Market Drops

I’d like to credit my Fed prediction to my wisdom and sagacity. In reality, I simply saw that the Fed had few other choices. They had to cut, and cut fast. The stock market was plunging, bonds were soaring and commodity prices were in free fall.

I like to follow the “break evens.” That’s basically the market’s estimate for what inflation will be. The 10-year break-even had dropped sharply in just a few days. That was a clear sign from the market that a rate cut was needed. The entire TIPS (Treasury Inflation Protected Securities) yield curve is negative. I wasn’t surprised to see that the Fed’s vote this week was unanimous.

In its statement, the Fed said, “The fundamentals of the U.S. economy remain strong. However, the coronavirus poses evolving risks to economic activity.” We may see negative rates soon.

Of course, lower rates won’t do much to stop the spread of coronavirus, but they may help soften the economic dislocations caused by the virus. Cruise stocks, for example, have been creamed. Many airline stocks are near multi-year lows. Natural gas is at a four-year low.

I think it’s likely that economic growth will take a hit this year, but it’s too early to say how long and by how much. But the slide in the yield of long-term bonds suggests that Wall Street isn’t expecting much in terms of growth this year. At a first guess, I’d say we can expect a flat economy with 0% growth. Look at how steeply the 10-year yield fell.

The fallout from the world of the coronavirus isn’t always so obvious. For example, shares of Clorox (CLX) have done well. Makes sense once you think about it. Campbell Soup (CBP) is also up. (People staying at home?)

Quick quiz: Guess what country’s stock market just hit a fresh two-year high?

Give up? The answer may surprise you. It’s China. “The blue-chip CSI 300 Index jumped 2.2% on the day to 4,206.72, its highest point since February 2018.” In China, seven of 31 provincial-level governments have pledged to spend $505 billion on infrastructure projects. That’s a staggering number and it will get even bigger as other cities join in. I’m curious to see if the U.S. will do something similar.

I also want to point out that our Buy List continues to do well in a relative sense. Outperforming in a down market is a key aspect of long-term success. I don’t yet have Friday’s final numbers, but it looks like our Buy List is set to outperform the S&P 500 for the fifth week in a row. Since our portfolio is focused on high-quality stocks, it tends to fare better in downdrafts. We also beat the market last year in a strong up year. Since February 20, the S&P 500 has shed 10.52%, but our Buy List is down by 8.97%.

What to Do Now

There are three things to do now.

1. Do not panic and sell.

2. Expect more volatility. We’ll probably retest the low.

3. Pick up bargains with any free cash.

I’ll restate the Peter Lynch quote from last week: “The real key to making money in stocks is not to get scared out of them.”

I can’t predict that we’ve already seen the low. Going by historical patterns, we probably haven’t. The market likes to test and retest prior low points. Last Friday, the S&P 500 got down to 2,855.84. I think we’ll test that soon. If it breaks, then the bears will be back. On Thursday, the S&P 500 closed below its 200-day moving average, which is not an encouraging sign.

Now to point #3. What bargains? Thanks to the downturn, some of our Buy List stocks look pretty good. Here are three:

Shares of AFLAC (AFL) are quite attractive here. The stock has gotten seriously beaten. Remember that most of their business comes from Japan. In fact, the company had a coronavirus case in one of its call centers. The shares are now down more than 25% from their 52-week high.

Don’t forget how well run this company is. Going by yesterday’s close, AFL currently yields 2.7%. That’s a solid dividend, too. Last month, AFLAC raised its dividend for the 37th year in a row. For 2020, the duck stock expects earnings of $4.32 to $4.52 per share. I think there’s a chance that AFL many lower guidance at some point.

I’m dropping my Buy Below down to $46 per share, but if you can pick up AFL below $42, then you’ve made a good deal.

Globe Life (GL) also looks very good in this range. For 2020, Globe life expects earnings of $7.03 to $7.23 per share. That gives the stock a P/E Ratio of less than 13. I’m lowering my Buy Below to $100 per share, but if you can get GL below $90, that’s a very good entry price.

I also like Check Point Software (CHKP). The stock recently hit a 52-week low. The last earnings report was pretty good. I’m dropping my Buy Below price on Check Point to $110 per share.

The selloff has thrown several of our Buy Below prices off. I don’t think it’s worthwhile to do a mass adjustment in one issue, but I’ll gradually readjust several Buy Belows over the next few weeks.

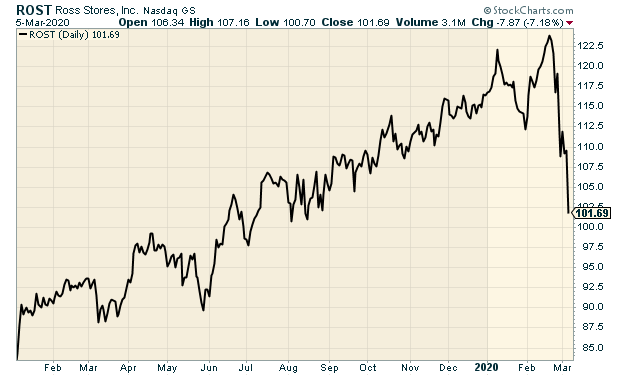

Ross Stores Beats Earnings and Raises Dividend

On Tuesday, Ross Stores (ROST) reported fiscal Q4 earnings of $1.28 per share. This was for the months of November, December and January. That’s the key holiday-shopping season for Ross. Previously, Ross had given us a range of $1.20 to $1.25 per share.

They key stat to watch for any retailer is same-store sales. For Ross, that rose by 4% last quarter. Ross has been expecting same-store sales growth of 1% to 2%. For the year, Ross made $4.60 per share. That’s up from $4.26 in 2018. Annual sales rose 7% to $16.0 billion.

Barbara Rentler, Chief Executive Officer, commented, “We delivered strong sales and earnings growth for both the fourth quarter and fiscal year. Our ongoing ability to offer compelling bargains to our customers enabled us to achieve these results despite our own challenging multi-year comparisons and a fiercely competitive holiday season.”

Ms. Rentler continued, “Fourth quarter operating margin of 13.3% was slightly better than expected, driven by higher merchandise margin.”

During Q4, Ross bought back 2.7 million shares for $309 million. For the year, they bought back 12.3 million shares for $1.275 billion. There’s still $1.275 billion left in the current authorization.

Ross also raised its quarterly dividend by 12%. The quarterly payout will rise from 25.5 cents to 28.5 cents per share. The new dividend is payable on March 31 to stockholders of record as of March 17. Ross has raised its dividend every year since 1994.

Now for guidance:

For the 52 weeks ending January 30, 2021, the Company is planning same-store sales to grow 1% to 2% and earnings per share of $4.67 to $4.88. We also plan to open about 100 stores this year, consisting of approximately 75 Ross Dress for Less and 25 dd’s DISCOUNTS locations.

For the first quarter ending May 2, 2020, comparable-store sales are forecast to be up 1% to 2% with earnings per share projected to be $1.16 to $1.21 versus $1.15 for the first quarter ended May 4, 2019.

That’s not so hot, but I think Ross is playing it safe. Wall Street had been expecting $1.25 per share for Q1 and $5.01 per share for the year. The stock just fell to a six-month low. I still like Ross, but I’m lowering my Buy Below price to $110 per share.

That’s all for now. The jobs report is due out later today. Next week, there’s not much in the way of economic reports. The CPI comes out on Wednesday. I expect it will show more low inflation. Also on Wednesday, we’ll get an update on the Federal budget. The deficit is looking quite large this year. Then on Thursday, we’ll get the weekly jobless-claims report. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on March 6th, 2020 at 7:06 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His