CWS Market Review – June 12, 2020

”We’re not even thinking about thinking about raising rates.” – Fed Chairman Jerome Powell

Last week’s issue of CWS Market Review was unusually prophetic. I said there’s a good chance that our Buy List would soon be positive for the year. Indeed, that happened two days later.

In that issue, I also said that the National Bureau for Economic Research might confirm the start of the recession before the end of the year. They did it on Monday. The expansion lasted 128 months.

I also noted that the Nasdaq Composite had just made a new all-time high. This week, the index went on to break 10,000 for the first time ever. The index started life in 1971 at 100. It took nearly 50 years to become a 100-bagger.

I also discussed the recent surge in cyclical stocks and wondered if the cycle had finally turned. On Thursday, however, cyclical stocks were severely punished as the market suffered its worst day in nearly three months. The S&P 500 plunged by 5.89% to close just above 3,000.

What caused the selling? We can point our fingers at the Federal Reserve, which met this week. Chairman Jerome Powell’s pessimistic outlook threw cold water on the market’s recent rally. There are also concerns that the long-feared “second wave” is starting to form.

On Thursday, the S&P 500 fell for the third day in a row. A three-day losing streak isn’t that big a deal, but we haven’t had one in 94 calendar days. That’s an usually long stretch. I guess we were due for one, and it came hard. In this week’s issue, I want to take a closer look at what’s been happening to the market and what we can expect going forward.

Cyclicals Get Crushed

One of the keys to understanding the stock market and investing is that the market tends to move in broad cycles. This happens as the market gets attached to a thesis. Let’s say the market convinces itself that the economy is gradually improving.

With that, we’ll see a fairly standard playbook. A rising market. Leadership from industrials and cyclicals. Lower bond prices. Higher yields and higher commodity prices. Greater pressure on the Fed to raise rates.

That’s the standard. Of course, each cycle will have its own peculiarities. Since March 23, the strong rally has been based on the idea of a diminishing threat from the coronavirus. Of course, that thesis isn’t completely unexpected since the rally is largely reversing the bear market which the coronavirus first caused. X is followed by negative X.

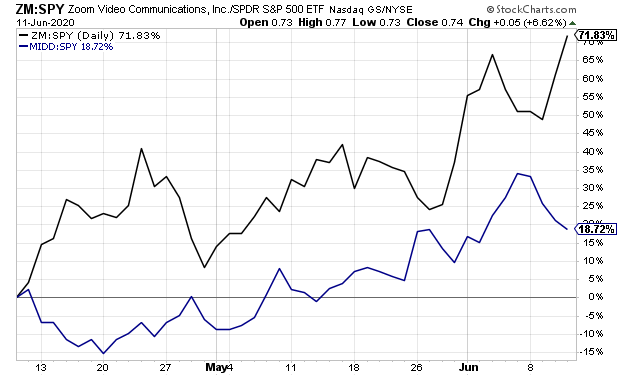

Here’s a good example of what I mean. This is a chart of the Zoom Video Communications (ZM) divided by the S&P 500 ETF, along with Middleby (MIDD) divided by the S&P 500 ETF.

When the lines are rising that means those stocks are beating the market. Conversely, when they’re falling, they’re lagging the market. If you examine the charts, you’ll notice that they tend to move in opposite directions. That’s the key point I want to get across.

In the age of the coronavirus, these two stocks are nearly polar opposites. I chose Zoom because it’s profited greatly from the lockdown, whereas Middleby has suffered. What’s been good news for one has been bad news for the other. (Zoom, truthfully, probably isn’t the best example for this exercise because the bullish trend has been so powerful, but even so, the cycle is still visible.)

Once these cycles get established, there will be strong contra-trend days. That’s a fancy word to say that everything that had been doing well gets crushed one day. At the same time, all the laggards suddenly find themselves in the spotlight. Or to quote more authoritatively, “So the last shall be first, and the first last.” As the thesis of the rally is debated on Wall Street, we’ll constantly see a tug-of-war between trend and contra-trend.

That’s exactly what we got on Thursday. It was a classic contra-trend rally. I’ll give you an example. If we look at High Beta stocks, these are stocks that tend to move around the most, and they got crushed. The S&P 500 High Beta Index lost more than 10% on Thursday. The High Beta sector is close to being an all-purpose anti-Covid sector. Whenever news breaks that the virus is fading, you can be sure High Beta will shine.

Within the stock sectors, the biggest loser was energy stocks. The S&P 500 energy sector lost over 9% on Thursday. In fact, the four worst-performing sectors on Thursday were (in order) Energy, Financials, Materials and Industrials. If you recall, these are the exact four that I told you last week comprise the cyclicals universe.

It’s these cyclical stocks that had performed so well that got their heads chopped off on Thursday. The price action on Thursday wasn’t a minor pushback, either. The bears gave these stocks a super-atomic wedgie. Callie Cox noted that on the NYSE, decliners led advancers by 1,800. That’s the most in nearly five years. In other words, the bears were going after everyone.

Last week, I asked if the cycle has finally turned. This week told us, “maybe not.” I wish I could be more emphatic in my predictions, but the facts won’t allow for it. Until we know more, we should maintain a conservative approach to our investments. Three of our stocks that look particularly good right now are Stepan (SCL), Middleby (MIDD) and Stryker (SYK).

Mr. Powell Spooks the Market

As I mentioned earlier, the Federal Reserve got together this week. On Wednesday, the Fed released its policy statement. As expected, there wasn’t any change to its policy. Rates are already rock bottom, and I doubt they’ll soon go negative.

What caught Wall Street’s attention were comments made by the Fed Chairman in his post-meeting press conference. Jerome Powell was unusually blunt. He said the Fed isn’t “even thinking about raising interest rates.” The Fed probably sees rates staying near 0% through this year, next year and the year after that. On top of that, the Fed will most likely continue to buy up bonds at a frenetic pace. Central bankers rarely speak so forthrightly.

This is somewhat ironic in that Mr. Powell was often harshly criticized by President Trump (who appointed him) for not lowering rates. There’s another story going on. A lot of the Fed’s job involves signaling. Right now, the Fed wants to make it clear to Wall Street that it will not stand in the way of any nascent recovery. Wall Street took the message to mean that the economy is more precarious than the bulls believe. Then on Thursday, it was as if three months of frustration from the bears came out all at once.

One big change between now and the market in March is that daily volatility has dropped significantly. The Fed also released its economic projections for the next few years. The central bank forecasts a very robust recovery. Of course, that’s coming off a very steep low.

The economic news is still quite scary. The latest jobless-claims report came in at 1.542 million. That’s the tenth weekly decline in a row. There was good news in last Friday’s jobs report. It showed an increase of 2.5 million jobs, although the Bureau of Labor Statistics conceded there were some errors in this report. We’ll have more details next month. (It’s not some conspiracy. It’s just hard to get the right data during extreme events.)

On Wednesday, we learned that consumer prices fell again last month. That’s the third monthly decline in a row. The good news is that we’re not too far from the normal range. My fear was that we could be near a deflation spiral where lower prices begat even lower prices. Things are getting back to normal, but it will take time.

That’s all for now. On Tuesday, we’ll get the retail-sales report for May. The previous report was terrible. Hopefully, that was the nadir. We’ll also get the latest report on industrial production. Then on Wednesday, we’ll have the latest report on new-home sales. Thursday, of course, will be another report on jobless claims. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on June 12th, 2020 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His