CWS Market Review – June 26, 2020

“That sounds about right.” – Me in last week’s issue, missing wildly on FactSet’s earnings

Boy, did I get that one wrong! In last week’s issue, I told you that Wall Street’s consensus on FactSet’s earnings of $2.43 per share “sounds about right.” Wrong!

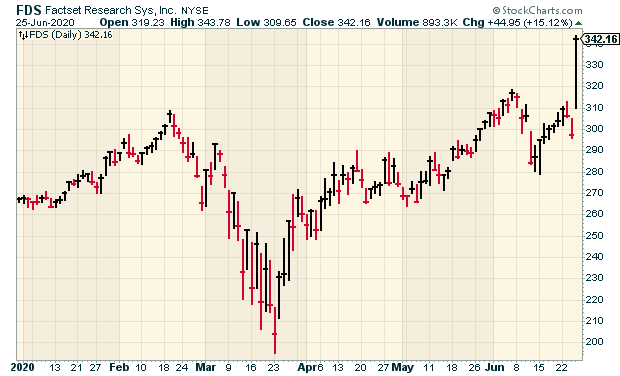

Instead, FactSet blew past the Street’s consensus. For its fiscal Q3, FactSet earned $2.86 per share. That was 43 cents better than estimates. On Thursday, the stock shot up 15%. Not only was I wrong, but I’m quite happy I was. FactSet is now our #2 performer this year.

I’ll tell you all about FactSet’s earnings report in just a bit. More seriously, it’s important for us to examine our mistakes and focus on what went wrong. I also have good news from Sherwin-Williams. The paint folks guided higher for their Q2 sales. We haven’t heard much news guidance-wise from anybody, so it’s good to get some positive news.

Also in this issue, I’ll discuss some of the recent economic news. The U.S. economy is gradually getting back on its feet, but there’s still a long way to go. First, though, let’s look at the great earnings news from FactSet.

FactSet Jumps 15% on Earnings Beat

On Thursday, FactSet (FDS) reported very good earnings for its fiscal third quarter, which ended on May 31. Quarterly revenues rose 2.6% to $374.1 million, while organic revenues climbed 2.6% to $375.3 million.

FactSet’s adjusted operating margin increased by 1.5% to 35.5%. That’s an important stat to watch. Adjusted diluted earnings rose by 9.2% to $2.86 per share. That beat estimates by 43 cents per share.

In May, FactSet increased its dividend by five cents to 77 cents per share. I’ll let you in on something. In the company’s press release, FactSet said that it has raised its dividend for 15 consecutive years. That’s actually incorrect; it’s longer than that. I suspect they haven’t adjusted for stock splits, but FactSet has increased its dividend every year since 1999. I contacted the company but never heard back. (Thanks to Dividend Growth Investor for the assist.)

“We had a strong third quarter and executed well in challenging circumstances,” said Phil Snow, FactSet CEO. “I am inspired by the efforts I see across the Company as FactSetters go above and beyond to support our clients and each other. The steps we have taken position us well to finish our fiscal year on target as we continue to evaluate and solve for evolving industry needs.”

Another key stat to watch for FactSet is Annual Subscription Value (or ASV). At the end of May, ASV plus professional services stood at $1.52 billion. This is important because annual ASV retention is over 95%.

At the end of the quarter, FactSet’s client count stood at 5,743. User count rose by 2,199 to 131,095, and employee count now stands at 10,065. That’s up 7.5% in the last year.

During Q3, FactSet bought back 46,689 shares for a total cost of $12.4 million. That’s an average price of $266.09. I’m generally not a fan of buybacks, but given the current FDS share price of $342, that turned out to be a shrewd investment in itself. In March, FactSet’s board added another $220 million to its existing buyback authorization. As of Thursday, there’s $288 million available to repurchase shares.

Now for guidance. FactSet expects full-year revenues to range between $1.485 billion and $1.49 billion. The high ASV numbers help a lot with revenue-forecasting. FactSet also expects full-year earnings to range between $10.40 and $10.60 per share. That’s an increase from the previous range which was $9.85 to $10.15 per share.

Basically, the company is adjusting for the strong Q3 numbers. That’s an increase of 55 cents per share to both ends of the guidance range. Very roughly, I’d say that’s 45 cents per share from the Q3 results and adding 10 cents per share to the Q4 results. That’s only a guess. The fiscal year ends on August 31.

Wall Street was very pleased with this news. On Thursday, the shares gapped up 15.1% and hit a new all-time high. FactSet is now a 27.5% winner for us this year. That’s second only to Trex (TREX). This week, I’m raising our Buy Below on FactSet to $360 per share.

Sherwin-Williams Raises Q2 Sales Guidance

On Monday, Sherwin-Williams (SHW) increased its sales guidance for Q2. Sherwin now expects sales to decrease “by a mid-single-digit percentage” compared with last year. That may not sound so great, but remember that the prior guidance was for sales to decrease “by a low- to mid-teens percentage.”

That’s welcome news, especially in this environment. Here’s an extended quote from the CEO.

We are encouraged by the sequential improvement in all three of our business segments during the second quarter. In The Americas Group, we rapidly adapted to the pandemic by implementing curbside pickup in our stores, utilizing our fleet of over 3,000 delivery vehicles, and leveraging our e-commerce platform. We have gradually and safely reopened nearly all of our sales floors over the last month. DIY growth in our stores remains strong, while our residential repaint and new residential segments have improved at a faster rate than our property management, new commercial and protective and marine segments. In the Consumer Brands Group, the unprecedented demand from most of our retail partners has remained robust, driven by consumers who are nesting during the pandemic and focused on DIY projects. In the Performance Coatings Group, demand has been variable by end market and geography. Packaging remains our strongest performer, while demand in our coil business has been choppy following the slower reopening of many commercial construction projects.

I’m relieved to hear this. Many companies have withdrawn their guidance due to the coronavirus, which is certainly understandable, so I appreciate any background we can get.

Sherwin-Williams will release its Q2 earnings on July 28. The company will update its sales and earnings guidance at that time. Sherwin-Williams is a buy up to $590 per share.

The U.S. Economy Is Gradually Waking Up

As we head towards the midpoint of the year, the U.S. economy is at an odd spot. Much of the economy is reopening. There are also reports of a surge in coronavirus cases, especially in areas that had not been hit as hard. I should caution that the data are still coming in.

You certainly get the sense that people are restless. They’ve been locked up for several weeks. Apparently, consumers are ready to shop! The last retail-sales report was remarkably strong. The government said that retail sales rose by 17.7%. That beat expectations by 10%. I think this also shows evidence of the stimulus checks.

Give people a reason to shop, and they’ll do it.

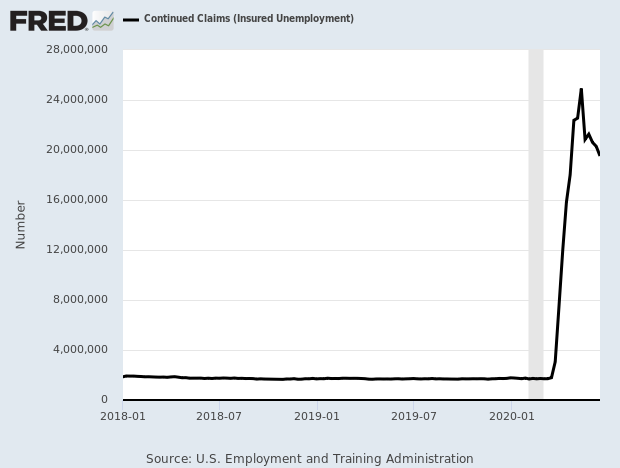

However, the employment outlook is still weak. Thursday’s jobless-claims report came in at 1.508 million. That was the fourteenth=straight week that jobless claims topped one million. While this continues the trend of lower claims, the report was still above the expectations of 1.35 million. This is the second week in a row that claims have come in higher than expectations. The number of people getting benefits fell below 20 million for the first time in two months.

The recent numbers are actually improvements on what we saw earlier this year. Just to give you an idea of how large these numbers are, before the coronavirus, the record for a single week was 695,000 in September 1982.

There’s also a concern about a surge in coronavirus cases. States like Texas and Florida have seen major spikes. Apple closed some of its stores in Houston. The seven-day average of news cases is up 30% from a week ago. There’s even talk of reversing some of the recent re-openings.

On Thursday, the government said that the U.S. economy contracted at a 5% annualized rate during the first quarter. That’s the same number as before. Bear in mind that the first quarter began nearly six months ago and ended three months ago. We’ll get the first report on Q2 GDP in another month.

We got some recent reports on the housing sector. This is important to watch for signs of a rebound. On Monday, the existing-home sales report showed a drop of 9.7% for May. The good news is that the National Association of Realtors expects a “strong rebound” in the coming months. On Tuesday, the new-home sales report showed an increase to 676,000 (that’s the annualized figure). Wall Street had been expecting 640,000. The previous three months were revised down.

Overall, the economic figures look pretty bleak, but I think we’ll see a rebound as the year goes on. I suspect that Wall Street has already figured that out and that’s why stocks have rallied over the last three months. In fact, day-trading is popular again. The Nasdaq Composite has closed higher on 20 of the last 25 sessions. Don’t be suckered in. I suspect the day-traders will again learn a valuable and expensive lesson.

Now let’s look at some news impacting our Buy List stocks.

Buy List Updates

I have a few updates on some of our Buy List stocks.

Check out the appearance by Gil Shwed, the CEO of Check Point Software (CHKP), on Jim Cramer’s Mad Money.

Due to the big increase in coronavirus cases, Disney (DIS) said it’s going to push back its plans to re-open its parks in California. This includes Disneyland and California Adventure. The original plan was for July 17. Disney said they hope to provide more guidance after July 4. The parks have been closed since March 14.

With FactSet’s earnings out of the way, that’s it for earnings reports until the Q2 earnings season starts. We already have a few earnings dates in. Stepan (SCL) is due to report on July 22. Hershey (HSY) is scheduled for July 23. I already mentioned SHW on July 28. Stryker (SYK) will report on July 30. Also, RPM International (RPM), our straggler from the May reporting cycle, will report on July 27. As we get closer to earnings season, I’ll have the earnings calendars as I have done in previous seasons.

That’s all for now. The market will be closed next Friday, July 3 in honor of Independence Day. That will make the economic calendar a little crowded. On Wednesday, ADP will release its private-payrolls report. The Fed will also release the minutes from its last FOMC meeting. Plus, the ISM Manufacturing Index is due out. On Thursday morning, the jobs report for June comes out. At the same time, the jobless-claims report comes out. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on June 26th, 2020 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His