CWS Market Review – March 12, 2021

“Just because you buy a stock and it goes up does not mean you are right. Just because you buy a stock and it goes down does not mean you are wrong.” – Peter Lynch

Today is the one-year anniversary of one of the worst days in market history. On March 12, 2020, the S&P 500 plunged 9.5%. The reality of the coronavirus was sinking in, and people were scared. All over the world, businesses were shutting down. It seemed that all the news was bad. The VIX closed at 75 that day.

Even wise market veterans were alarmed:

This is freefall

— Eddy Elfenbein (@EddyElfenbein) March 12, 2020

That wasn’t even the worst day. The following Monday, March 16, the S&P 500 fell another 12%. In 22 trading days, the stock market lost one-third of its value. That’s a staggering loss.

What a difference a year makes. I certainly won’t say things are good, but I will say that things are much improved. On Thursday, the S&P 500 closed at an all-time high. So did the Dow and Russell 2000. Since its low last March, the S&P 500 is up more than 76%.

There’s no way I would have predicted that outcome. That’s one of the benefits of our type of investing. You don’t have to be a magical swami that predicts the future. Instead, we follow a disciplined strategy that serves us well no matter what the environment.

These have been extraordinary times. According to one estimate, central banks around the world have bought an average of $1 billion in assets every hour for the last year.

In this week’s issue, I’ll try to make sense of this market. But I’ll caution you that it’s a confusing one. I’ll also bring you up to date on some of our Buy List stocks. We already have five 10% winners this year. How about little Miller Industries? It’s up by 18% for us. Middleby is up over 32%. But first, let’s look at last Friday’s jobs report.

One Year Later, and We’re at All-Time Highs

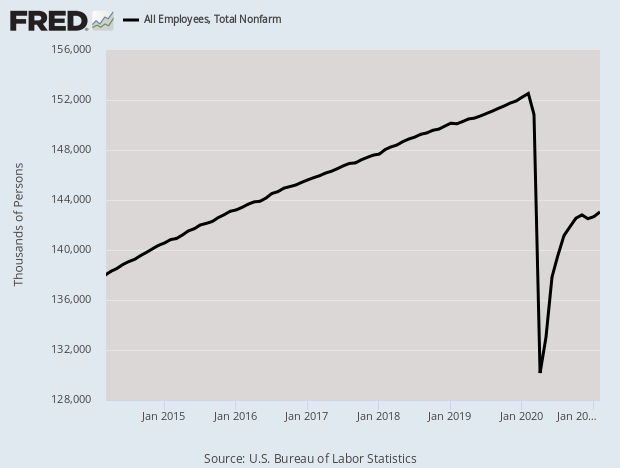

Last Friday, the government said that the U.S. economy created 379,000 net new jobs in February. That’s good news, and it’s more evidence for our thesis that investors are underrating the economy. Let me be clear: we still have a long way to go. I merely mean that things are finally going in the right direction.

In February, the unemployment rate ticked down to 6.2%. That’s high, but it’s lower now than its peak in the 2003 recession. January’s job-creation number was revised up to 166,000. The broader U-6 rate is 11.1%, and the labor force participation rate is 61.4%. The bad news is that December’s job-loss stat was revised downward to a loss of 306,000 jobs.

The equation isn’t a secret. Good COVID news is good economic news. It’s that simple. Here’s an interesting stat: bars and restaurants accounted for 75% of the job gains last month. As things get back to normal, we’ll see more of this. Disney said that Disneyland may be able to reopen in a few weeks.

Very roughly, the economy has lost about 10 million jobs. Of those, 75% have been service-sector jobs, and half of those have been in leisure and hospitality. You can’t install drywall over Zoom, nor can you ride a rollercoaster. Last April’s jobs report showed a loss of 20 million jobs. Since then, we’ve gained back 13 million.

We got more evidence of a growing labor market on Thursday when the weekly jobless-claims report came in at 712,000. In normal times, that’s a terrible number. But nowadays, that came within an inch of being the best jobless-claims report in a year. (One report from late November was 711,000.)

The other big news this week was the signing of President Biden’s $1.9 trillion economic-stimulus package. As usual, I won’t comment on the efficacy of such matters. I steer clear of politics, but I will say that the market reacted positively. The bond market doesn’t appear to be terribly concerned about the massive borrowing. The 10-year Treasury is at a lowly 1.53%. Being the world’s reserve currency has its perks.

There’s also been more concern about a rise in inflation. At some point, I think these concerns are warranted, given how much money the government is spreading around. However, I tend to be an empiricist on these matters. This week’s inflation figures showed that inflation is still well contained.

On Wednesday, the government said that inflation increased by 0.4% last month. That was in line with expectations. Over the last year, inflation is running at 1.7%, which is quite modest. I also like to look at the “core rate” of inflation. The core rate excludes food and energy prices, which can be very volatile. For February, the core rate increased by just 0.1%. With 18 million Americans receiving unemployment benefits, there’s plenty of slack in the labor market. Over the last year, core inflation is running at 1.3%.

The Federal Reserve gets together next week. Jerome Powell, the top banana at the Fed, has made it abundantly clear that he doesn’t mind seeing a rise in inflation. Not only has the Fed lowered interest rates to near 0%, but they’re also buying up massive amounts of bonds. Each month, the Fed buys $80 billion in Treasuries plus another $40 billion in mortgage-backed securities.

I don’t expect to hear any policy changes next week, but at some point, the Fed will talk about tapering off its bond buying. When that happened eight years ago, the market threw a temper tantrum, the infamous Taper Tantrum. I think they’ll be better behaved this time.

The Tech Rebound May Not Last

Earlier I mentioned the indexes that made new highs on Thursday. You may have noticed that I didn’t mention the Nasdaq Composite. That’s because it’s still 5% from its all-time high. That’s a reflection of the recent slump in the tech sector.

Tech has actually improved a lot over the past three days. At the end of Monday’s trading, the Nasdaq was down over 10% from its recent high. Monday, in fact, was a remarkable market day for investing because Wall Street strongly tilted towards our type of investing while shunning the kinds of stocks we steer clear of. For the day, the S&P 500 lost 0.54%, while our Buy List gained 0.82%. That’s a huge gap for one day.

(To be clear, we do have tech stocks on our Buy List such as Thermo Fisher and Ansys. Technically, Fiserv is classified as a tech stock as well, but we don’t have any of the well-known mega-cap tech stocks.)

Frankly, I’m skeptical of tech’s recent bounce. It was too much and too fast. I think the sector is in for more pain. I’ve talked a lot about the market’s shift to cyclical and value stocks, and that’s only grown stronger in recent weeks.

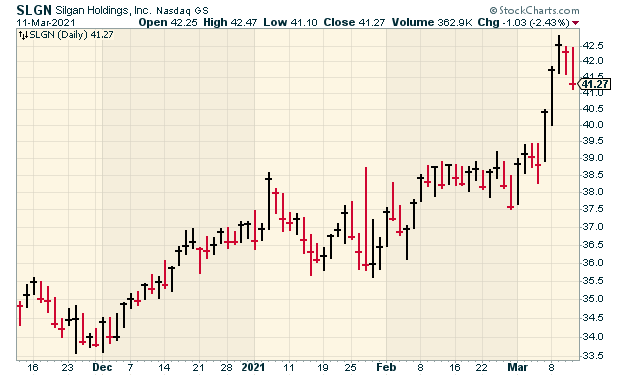

A resurgent economy will be good for cyclicals. In a minute, I’ll discuss Silgan Holdings (SLGN), which is a good example of the kind of stock that is well-positioned for this environment. The company makes containers, and that’s precisely the kind of industry that was held back during the lockdowns. Other examples would be Middleby (MIDD), Miller Industries (MLR) and Trex (TREX). This trend is alive and well, so don’t get distracted by market sideshows like meme stocks. Make sure your portfolio is well diversified among high-quality stocks such as you’ll find on our Buy List.

Buy List Updates

I want to make a few adjustments to some of our Buy Below prices. Remember, these aren’t price targets. Rather, they’re guidance for current entry into our stocks.

Let’s start with Silgan Holdings (SLGN). The container company had a very good Q4 earnings report. The growing economy is very good for them. Silgan made 60 cents per share, which was seven cents better than estimates. For 2021, Silgan sees earnings ranging between $3.30 and $3.45 per share. Going by the midpoint, that’s a 10.3% increase over last year. This week, I’m lifting our Buy Below on Silgan to $45 per share.

I decided against raising Fiserv’s (FISV) Buy Below after its last earnings report, but I’m reversing course this week and raising it. This is a very impressive company. Fiserv just wrapped up its 35th year in a row of double-digit earnings growth. It’s the Joe DiMaggio of Wall Street and I think it’s highly likely that this year will be #36.

For 2021, Fiserv expects revenue growth of 8% to 12%. Fiserv also sees earnings of $5.30 to $5.50 per share. That’s growth of 20% to 24%. Wall Street had been expecting $5.39 per share. I also like that Fiserv’s board approved a new 60-million-share buyback authorization. I’m lifting our Buy Below on Fiserv to $135 per share.

I’m lowering our Buy Below price for Zoetis (ZTS) to $165 per share. Last month, the company released a good earnings report, and it beat expectations. Still, the shares didn’t react as I had hoped. For 2021, Zoetis sees revenues ranging between $7.40 billion and $7.55 billion, and EPS between $4.36 and $4.46. That was more than Wall Street had been expecting. I’m not worried about Zoetis. The shares have rebounded in the past week, but I’m dropping our Buy Below down to $165 per share.

I’m not changing my Buy Below price on Disney (DIS), but I wanted to highlight some recent good news. Thanks to spring-breakers, Disney World’s theme parks are completely booked next week. In California, the government provided new guidance for theme parks, which means Disneyland could reopen on April 1. It’s been shuttered for the last year. Disney+ now has 100 million subscribers. That’s half the number of Netflix, and it’s only 16 months old. Disney remains a buy up to $200 per share.

That’s all for now. The Federal Reserve meets again next week. Don’t expect much in the way of policy changes, but it will be interesting to hear what the central bank has to say. The policy statement is due out on Wednesday afternoon. On Tuesday, we’ll get reports on retail sales and industrial production. Also on Wednesday, the housing-starts report is due out. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on March 12th, 2021 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His