CWS Market Review – May 18, 2021

“I have no idea how this works.” – Dave Portnoy

(This is the free version of CWS Market Review. Don’t forget to sign up for the premium newsletter for $20 per month or $200 for the whole year. Thank you for your support.)

You’re not alone, Dave. I recently said that I’ve been waiting 15 years for Nike (NKE) to pull back. Alas, it’s never hit the bargain bin. The sneaker company only seems to climb higher.

See that flat blue line? That’s actually a 1,075% gain for the S&P 500. It just looks flat in comparison to 26,000% for Nike.

For the overly literal who missed my point, I meant to say that sometimes it’s worth paying a premium for a company. Especially if it’s a premium company. There’s little point in trying to save 15% on the buy while missing the next 1,500% move. Pennywise and billions foolish.

This is a key point in stock analysis. Nike is a wonderful company and by most conventional metrics, it’s over-priced. It’s almost always overpriced. Even now it’s going for 43 times this year’s earnings. Yet it’s still done so well.

What are we missing? When you’re overly focused on a stock’s value you may overlook its most important asset, that being its ability to grow. All investing is at some level growth investing. A good investment may double its P/E Ratio. It’s rare but it happens. But a company often can grow the E in the P/E Ratio (the earnings) by many, many fold.

Here’s a thought exercise. Imagine if you know beforehand that a stock will grow its earnings by tenfold in, say, ten years. Are you going to haggle much over 10 cents on the buy price? I wouldn’t.

Warren Buffett often cites Ben Graham as his mentor. Buffett worked for Graham, and his eldest son is named Howard Graham Buffett. But there’s another inspiration to Buffett’s thinking and that’s Philip Fisher (the father of Ken Fisher). Fisher as much as anyone can be called the father of growth investing. His best-known book is Common Stocks and Uncommon Profits. Fisher stressed the importance of a long-term perspective and buying for growth.

John Train said that Warren Buffett is 85% influenced by Benjamin Graham and 15% by Philip Fisher. That sounds about right. Of course, too much of a focus on growth investing can be a pitfall as well. It can lead you to vastly overpay for a stock. With investing, there’s a magic formula outside of discipline and patience.

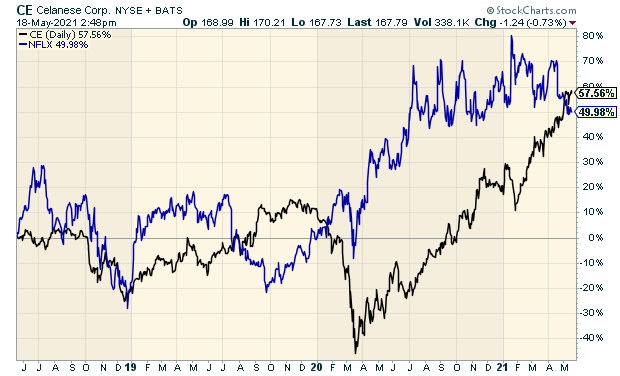

I was recently looking at the stock of Celanese (CE). This is one of those big companies that doesn’t get much attention in the trading universe. The company has a market cap of $20 billion and about 8,000 employees. Still, you rarely hear it mentioned in investing circles.

What do they do? Celanese is the world’s leading producer of acetic acid. Sexy, I know. Still, the stock has outperformed Netflix over the past one, two and three years. Who would have guessed that?

The truth is, there are lots of companies like Celanese but too many investors shy away from investing in all but a few well-known stocks. There are thousands of stocks out there and they’re not all overpriced.

A good clue that a company has a strong market position is what I call the nice, smooth earnings line. This is when companies consistently increase their earnings-per-share.

Here’s an example. This is the earnings-per-share history of AmerisourceBergen (ABC).

2005: $0.83

2006: $1.08

2007: $1.31

2008: $1.46

2009: $1.69

2010: $2.17

2011: $2.54

2012: $2.76

2013: $3.14

2014: $3.97

2015: $4.96

2016: $5.62

2017: $5.88

2018: $6.49

2019: $7.09

2020: $7.90

2021: $8.53 (est)

2022: $9.10 (est)

2023: $9.93 (est)

Notice how it’s a nice, steady climb.

My Watch List

I’m often asked how I go about finding the stocks for my Buy List. What I do is track a Watch List of about 100 stocks. These are stocks that I generally define as good stocks. They usually have thriving businesses and consistent operating histories.

I think of the stocks on the Watch List as the minor leagues and the Buy List is like getting called up to the majors. I’m constantly adding and deleting names to the Watch List. I’m not terribly disciplined, and the list often grows larger than 120 stocks. That’s too many. I’ve recently pared the list back to 100 stocks.

Here’s a sample of 20 stocks that are currently on my Watch List.

You can see the entire list by joining our premium service.

Stock Focus: Tyler Technologies

I’ll highlight one of the Watch List stocks above. Tyler Technologies (TYL) of Plano, Texas is the largest U.S. software company that’s solely focused on the public sector. That’s a nice market to focus on since the government has deep pockets and it never goes bankrupt.

Tyler’s software comes in handy for a local government trying to manage its mission. This includes dozens of different applications. Local governments have to do a lot from managing payroll and accounting to billing and HR management. Tyler helps smooth the process. More importantly, it controls costs.

Tyler divides its software business into six categories: appraisal and tax software and services, integrated software for courts and justice agencies, enterprise financial software systems, planning/regulatory/maintenance software, public safety software, records/document management software solutions and transportation software solutions for schools.

Tyler has implemented 21,000 installations in more than 10,000 local government agencies. Tyler doesn’t just work in the U.S. The company has aided governments in Canada, Australia and many other countries.

Consider some numbers. The software market for state and local governments is currently at $15 billion per year. In the U.S., the government exists at several levels which means there are thousands of government agencies at the state and local level, plus school districts. Moreover, many of the current systems used by governments are outdated and in desperate need of an upgrade. You’d be shocked to learn how many government offices still use filing cabinets.

It looks like this year Tyler will pass the $1.3 billion revenue mark, plus reach 5,600 employees.

Last year, Tyler’s subscription revenue grew 12.6%. Free cash flow was up over 50%. Approximately 30% to 50% percent of Tyler’s new software clients choose their software-as-a-service (SaaS) model, as new business continues to gradually transition toward subscriptions.

Tyler is very popular with its client base. The company maintains a 98% retention rate. That’s very good when two-thirds of your revenue is recurring subscriptions. The company has a solid balance sheet. Since 2002, Tyler has bought back nearly 28 million shares.

Tyler has impressive plans for growth. The problem with local governments is that they often operate on several disparate systems. In simple terms, they don’t talk to each other. They have no incentive to. Tyler wants to bring them all together. That way, the government can be more efficient and more responsive to their constituents.

Here’s Tyler’s remarkable growth in EPS. Another nice, smooth line:

2012: $1.00

2013: $1.51

2014: $2.09

2015: $2.54

2016: $3.49

2017: $3.92

2018: $4.80

2019: $5.30

2020: $5.52

2021: $6.15 est

2021: $7.09 est

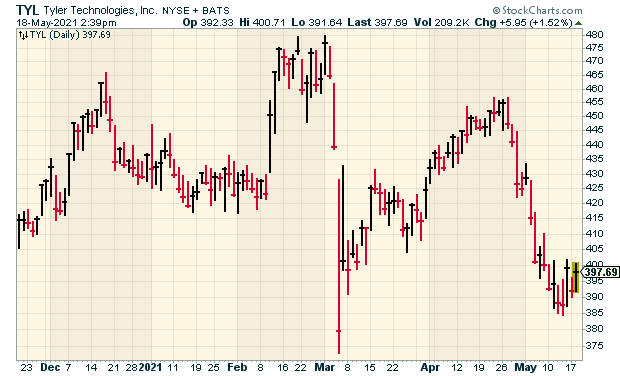

Like Nike, I’ve been waiting for Tyler to get clobbered, and we recently got our chance. The stock had an earnings miss for Q4. The shares also got dinged after Tyler went to the bond market to fund some recent acquisitions.

A few weeks ago, Tyler reported Q1 earnings of $1.43 per share which beat the street by 11 cents per share. That was up 14% over last year’s Q1. Not good enough. In March, Tyler was as high as $480 per share. Lately, it’s around $400.

This year’s estimate for $6.15 per share is ambitious but very doable. Best of all, the American Rescue Plan Act has $350 billion earmarked for state and local governments.

This is a strong growth company with a solid moat. I’d like to see TYL come down a lot more. Still, the ghost of Nike shares lost haunts me.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. Don’t forget to sign up for our premium newsletter.

Posted by Eddy Elfenbein on May 18th, 2021 at 3:49 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His