CWS Market Review – February 1, 2022

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The Stock Market Stumbled Into January

The stock market certainly didn’t get off to a good start this year. For the month of January, the S&P 500 lost 5.26%. That was the market’s worst month since March 2020 and it was the worst January since 2009.

Actually, it could have been worse. The S&P 500 posted big gains on the final two trading days of the month. In fact, we came very close to being in an official correction. From the market’s closing high on January 3 to the closing low from last Thursday, the S&P 500 lost 9.80%. The Nasdaq Composite did even worse and it’s still in correction territory.

We’ve got a decent bump on Friday and Monday plus a nice gain today, but it’s too early to say the selling wave is over. How do we know when the coast is clear? That’s hard to say, but one encouraging sign is that the S&P 500 has poked its head back above its 200-day moving average (the green line in the chart below). We still have about 1.8% to go until the index breaks above its 50-day moving average.

Don’t be surprised to see another downswing. The market likes to test and retest its recent low. Wall Street bears are easily startled, but they’ll soon be back, and in greater numbers.

Wall Street has finally acclimated itself to the idea that the Fed is really truly going to raise interest rates. The futures market has literally priced the odds of a March hike at 100%. That sounds pretty certain. There’s even been some recent talk of the Fed hiking rates by 0.50%. Call me a doubter.

The big question for the Fed is how inflation will behave. Consider some facts: Crude oil is up 65% in the last year, and it recently touched a seven-year high. Cotton is at a 10-year high. Orange juice futures got to their highest level since 2018.

This morning, the Institute for Supply Management said that its ISM Manufacturing index fell to 57.6 last month. That’s the lowest number in 15 months. This signals that the factory sector of the economy may be slowing. Goldman Sachs cut its Q1 GDP growth forecast to 0.5% from 2%.

Church & Dwight Rallies on Strong Earnings

One of the ideas I try to stress to investors is understanding what kind of stocks they own. Specifically, investors should know if a stock they own is a defensive stock or a cyclical stock.

It’s not that one kind of stock is better than the other. It’s that both groups move in big waves. That means that no matter how good or bad a given stock is, it can easily get wrapped up in the broader trend.

By defensive stock, I mean a company whose business fortunes aren’t closely tied to the status of the economy. A perfect example from our Buy List is Church & Dwight (CHD). The company owns a broad range of consumer brands. They have everything from Arm and Hammer to Trojan, OxiClean and Nair.

If the economy hits the skids, Church & Dwight’s business won’t be terribly impacted. It makes the kind of things people need all the time. Contrast that with a company like a chemical company or a homebuilder. Those sectors tend to be “feast or famine.” In fact, much of the business for these kinds of companies involves managing themselves between the busts.

Over the summer, CHD warned us that Q3 was going to be weak. It saw earnings coming in at 70 cents per share. The official word was that they were “temporarily constrained by supply.”

Apparently, they weren’t as constrained as advertised. CHD had a great Q3, earning 80 cents per share.

Over the last few months, shares of Church & Dwight have performed quite well. Much of that is due to the market’s recent concerns that the economy may be slowing down. Lots of defensive stocks have done well. Another good example from our Buy List is Hershey (HSY).

A few months ago, Church & Dwight told us to expect Q4 earnings of 61 cents per share. On Friday we got the report and again, CHD underestimated themselves. The company made 64 cents per share for its Q4. That’s up 20.8% from a year ago. Wall Street had been expecting earnings of 60 cents per share.

For the year, the company made $3.02 per share. That’s up 6.7% from a year ago. Full year net sales grew 6% to $5.19 billion.

CEO Matthew Farrell said:

Our brands once again experienced strong consumption in Q4 2021. In the U.S. we grew consumption in 11 of the 16 categories in which we compete. Five of our brands experienced double digit consumption growth including ARM & HAMMER® Scent Boosters, ARM & HAMMER® Clumping Litter, OXICLEAN® stain fighters, BATISTE® dry shampoo and ZICAM® zinc supplements. Consumption continues to outpace shipments as supply chain disruptions continue. This strong consumption would likely have been higher if not for the ongoing supply chain challenges. This demonstrates the strength of our brands as we gained share on 6 of the 13 power brands in a difficult supply environment. Global online sales grew 12.7% in 2021, and as a percentage of total sales has expanded to 15% for the full year.

Church & Dwight said rising material costs have pinged their gross margins. The company also said it’s facing higher transportation costs and labor shortages. While they expect supply issues to gradually abate, the company is raising prices. By the end of this month, Church & Dwight expects to have taken pricing action on 80% of their portfolio brands. Fortunately, most CHD brands have a strong position in their respective markets so they can command higher prices. Companywide gross margins were 42.5% in Q4.

The company also raised its quarterly dividend from 24.25 cents per share to 26.25 cents per share. That comes to $1.05 for the year. That’s a yield of a little over 1%. This is CHD’s 26th consecutive annual dividend increase.

The market apparently liked the report as shares of CHD rallied 4.40% to close at $103. I continue to rate CHD a strong buy up to $110 per share.

Rollins Is Worth a Look

One of the best ways to find good investment opportunities is to follow excellent companies and wait for their share prices to fall apart.

A good example is Rollins (ROL). The company is in the pest control business. In plainer terms, they kill bugs for money. Rollins is the parent company of Orkin.

I realize it sounds icky, and it is, but that doesn’t mean it’s a bad investment. Quite the opposite. In his book One Up on Wall Street, Peter Lynch wrote, “Better than boring alone is a stock that’s boring and disgusting at the same time. Something that makes people shrug, retch, or turn away in disgust is ideal.” Yep, that’s Rollins.

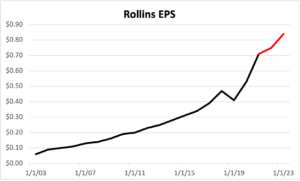

Check out the growth in its EPS:

The red part of the line is the estimate.

It’s amazing how few people know about this stock. Only five analysts on Wall Street bother following Rollins even though it has a market value of $15 billion. Years ago, Rollins was a diversified company with lots of holdings. They eventually spun off their oil and gas units into another company. What was left was the pest control business which is a very nice business to own.

The company is able to maintain gross margins in excess of 50%. As it turns out, killing bugs is very profitable. Since 2000, shares of Rollins are up more than 55-fold.

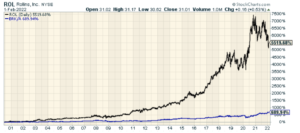

Check out this chart of ROL’s performance since May 2000. For context, see that blue line down there? That’s Berkshire Hathaway:

Rollins now has two million customers at 700 locations around the world. The company currently pays a quarterly dividend of 10 cents per share, but it’s been known to hand out special dividends at the end of the year. I like companies that do that.

Despite the company’s long-term success, the stock hasn’t done that well lately. Shares of ROL peaked at $43 in October 2020. Last week, the stock got as low as $28.51 per share.

The earnings report came out last Wednesday and Rollins said it had Q4 earnings of 14 cents per share. That was one penny below estimates. This was the second quarter in a row that Rollins has missed estimates.

Rollins has faced some serious issues over the past year. The SEC said it was investigating the company’s accounting. Rollins doesn’t appear to be consistent in how they’ve reported revenue. The company is working with the SEC to resolve these issues. The takeaway for us is that the stock is down a lot. I wouldn’t say the shares are cheap, but they’re much cheaper than they used to be.

If Rollins can again command the earnings multiple that it used to have (around 45X), and if it can manage the earnings growth it used to have (12% to 14%), then this is a very inexpensive stock. Of course, that’s a lot of ifs. I’m going to keep a close eye on Rollins.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. Don’t forget to sign up for our premium newsletter.

Posted by Eddy Elfenbein on February 1st, 2022 at 6:12 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His