CWS Market Review – February 8, 2022

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The Blowout January Jobs Report

Last Friday, the government released the jobs report for January and the numbers were quite good. In fact, they were so good that they’ve had a major impact on what the Federal Reserve has planned, and by extension, the outlook for the stock market.

The bottom line for us is that this is a very good time to own conservative and defensive stocks, just like we have on our Buy List. In this issue, I want to lay out the case in more detail.

First, though, let’s look at the jobs report. During January, the U.S. economy added 467,000 net new jobs. That more than tripled expectations of 150,000. On top of that, the numbers for November and December were revised much higher.

Although the unemployment rate ticked higher to 4.0%, that’s still quite low by recent historical standards. Some of that is driven by fewer people looking for work, but make no mistake, there is underlying strength in the labor market.

For context, in March and April 2020, the U.S. economy shed 22 million jobs. That’s a staggering loss. Since then, the economy has added back 19.1 million jobs. We’re not that far from hitting a record high for number of employed folks.

This is a shift in the outlook for the economy. When the December jobs report came out, it was a complete bust. The Bureau of Labor Statistics said that only 199,000 new jobs were created in December. That was less than half of what was expected. On Friday, that number was revised upward to a gain of 510,000 new jobs.

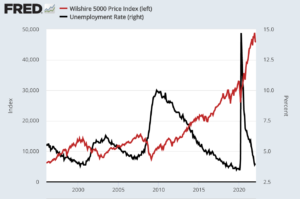

Here’s a look at the stock market (in red) along with the unemployment rate (n black).

For November, the number of jobs created was revised from a wimpy 249,000 to a brawny 647,000. I should add that these revisions are part of a larger annual revision.

Digging into the report, we see that the largest gains came from leisure and hospitality which added 151,000 jobs. Of that, 108,000 jobs were in bars and restaurants (I did my part). Retail added 61,000 and professional and business services added 86,000. Kathy Jones, the chief fixed income strategist at Charles Schwab, said, “It’s hard to find a weak spot in this report.” I have to agree.

The broader U-6 unemployment rate is nearly back to where it was pre-Covid. It’s now at 7.1%. The last pre-Covid low was 6.8% in December 2019. That number can be a better stat to watch for the true health of the economy.

The Labor Force Participation Rate rose 0.3% to 62.2%. That’s the highest since March 2020. This tells us how many people are out there working or looking to work. It’s not that far from where it was before Covid.

The LFPR can be distorted because of the growing ranks of retired folks. But the LFPR for prime working age (25 to 54) is back to 82.0% which is higher than where it was in 2017 and much of 2018. (Frankly, some people tend to overemphasize the importance of the Labor Force Participation Rate.)

Higher Rates Are Good for Defensive Stocks

The blowout jobs report has caused some investors on Wall Street to speculate that the Federal Reserve could hike interest rates next month by 0.5%. That was an outlandish view a few weeks ago, but since Friday’s jobs report, it’s now gone mainstream.

It could happen, but I won’t venture a guess as to what precisely the Fed will do. I’m more concerned with its general policy for this year. I think it’s very likely that the Fed will raise rates at each of the next four meetings, give or take. After that, it may take a more gradual approach. If this is right, that’s very good news for defensive investing.

The key point is that the Fed wants to convey to us investors that they’re not behind the curve regarding inflation (which, of course, they are). The Fed also wants to make a clear break from their “transitory” language that they used much of last year. In plainer terms, the Fed wants to seem hawkish now due to their own laxity over the previous two years.

As Milton Friedman said, there’s no such thing as a free lunch. That’s especially true with monetary policy. You’ll pay now or you’ll pay later, but you will pay.

Ideally, I suspect the Fed wants to have short-term interest rates at or near 2% between one year and 18 months from now. The next key test comes this Thursday when the government releases the inflation report for January.

The last inflation report showed that consumer prices rose by 0.47% in December. That was more than expectations of 0.4%. The good news is that energy prices finally started to ease up in December. For the month, energy prices fell by 0.4%. Within that, gasoline was down 0.5% and fuel oil was off by 2.4%. Still, we had significant energy inflation last year. Energy was up 29.3% in 2021 and gasoline increased by nearly 50%.

In the most-recent CPI report, Wall Street was really spooked by the core rate, which excludes volatile food and energy prices. For December, core inflation rose by 0.55%. That was more than expectations of 0.5%. Used car prices have been a particular trouble spot for inflation. During 2021, used car prices increased by 37.3%.

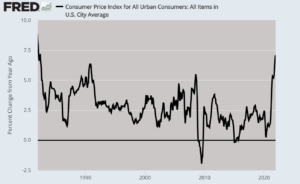

For all of 2021, headline inflation ran at 7.12%. That was the highest rate since June 1982 (see the chart above). The core rate increased by 5.49%. That’s the highest since February 1991. So we’re looking at 30- or 40-year highs for inflation depending on which measure. You can see why Wall Street is less than convinced by the Fed’s projections.

For Thursday, Wall Street expects to see both headline and core inflation of 0.4%. If that comes in high, Wall Street will not be pleased.

The Fed doesn’t meet again for another five weeks so a lot could happen between now and then. At the futures market, traders currently think there’s a 29% chance that the Fed will hike by 0.5%. The traders said that there’s a 71% chance of a 0.25% rate hike. According to the futures traders, there’s literally a 0% chance of the Fed doing nothing.

Earnings from AFLAC and Hershey

I want to home in on the point that this is a good time for conservative, defensive stocks. In the premium issues, I’ve been talking about our recent earnings reports. (Reminder, sign up!).

I was particularly impressed by last week’s reports from AFLAC and Hershey. These are very good examples of the kinds of stocks that can prosper in this environment.

Last week, AFLAC (AFL) said it made Q4 earnings of $1.28 per share. That’s an increase of 19.6%. The weaker exchange rate pinged earnings by five cents per share. Wall Street had been expecting $1.27 per share. This was another very good quarter for AFLAC.

For the year, AFLAC made $5.94 per share. That’s up nicely from $4.96 per share in 2020. Forex pinged this year’s bottom line for six cents per share. Adjusting for that, AFLAC’s earnings were up 21% last year to $6 per share.

AFLAC is already up 13.1% for us this year. That’s not bad for a little over one month. On Thursday, the shares hit a new 52-week high of $66.30. AFLAC has always been a good stock but it’s gotten a lot more attention recently because the Fed raising rates won’t hurt it.

Check out this chart:

On Thursday, Hershey (HSY) said it made $1.69 per share for Q4. That topped the consensus of $1.61 per share. Business is so strong that Hershey has boosted its capacity, yet it still can’t keep up with demand. Thank you, Covid!

Hershey said it expects 2022 earnings of $7.84 to $7.98 per share. That’s a very optimistic outlook. The consensus on Wall Street had been for $7.57 per share. Hershey is a 7% winner for us so far this year. On Thursday, shares of HSY rallied to an all-time high of $207.21. The stock has more than doubled in four years.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. Don’t forget to sign up for our premium newsletter.

Posted by Eddy Elfenbein on February 8th, 2022 at 7:42 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His