CWS Market Review – October 4, 2022

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The Stock Market Rallies 5.7% in Two Days

The stock market put on a furious rally over the last two days, but is it just another bear-market rally? After this summer’s rally got blown apart in a few weeks, it’s hard to feel hopeful.

In just two days, the S&P 500 has gained 5.73%. Sadly, big moves like this don’t normally come in healthy markets. Historically, most of the market’s big short-term gains have come during rough markets. They’re usually snapbacks from major lows.

The smart take is to view the last two days with a healthy dose of skepticism. We’ve been fooled before.

Still, I’m willing to take whatever profits Wall Street wants to throw our way. Look at Trex (TREX), our worst-performing Buy List stock this year. It’s up 11.8% over the last two days.

The next big test for the market will come this Friday when the Labor Department releases the September jobs report. It will also update the numbers for July and August. The last report was a good one. According to the government, the U.S. economy created 315,000 net new jobs during August, and the unemployment rate ticked up to 3.7%. For Friday, the consensus on Wall Street is to see a gain of 275,000 jobs in September and that the jobless rate will stay at 3.7%.

One interesting feature of the unemployment rate is that it tends to oscillate between extremes. This is the idea behind the “Sahm Rule,” named for economist Claudia Sahm. My shorthand definition for the rule is that if the unemployment rate goes up a little, then there’s a good chance it will go up a lot.

More technically, the Sahm Rule says that we’re probably in a recession if the three-month average of the unemployment rate rises by 0.5% from its low over the last 12 months. Best of all, it’s easy to calculate.

The lowest unemployment rate of the last 12 months came in July when it got down to 3.5%. That means that we’re not that far away from a recession. Friday’s report will tell us a lot more.

One promising sign is that the jobless-claims numbers have been much improved since the summer. That number tends to be whatever stats people call “noisy,” which means it bounces around a lot. That’s why economists like to look at a rolling average to smooth out the bumps.

If Friday’s jobs report comes in weak, that could take some pressure off the Federal Reserve. On the other hand, if the number is strong, then it could reiterate the Fed’s commitment to higher interest rates.

Interestingly, the bond market shot up yesterday and the rally continued into today. That could be a bet that the Fed may ease up a bit. Still, I think the safe assumption is that the Fed will hike again at its next meeting in November by 0.75%. After that, it’s hard to say. For their part, futures traders are leaning towards a smaller hike in December. That could be right, but it depends on the direction of the economy.

One worrying sign for the economy came out yesterday. The ISM Manufacturing Index fell to 50.9 for September. That’s down from 52.8 in August. Any number above 50 means that the factory sector of the economy is growing; below 50, and it’s contracting. This was the 28th month in a row of a growth.

After the jobs report, the next big report for us will be the CPI report for September. While most people follow the CPI for the official inflation number, the Federal Reserve prefers to follow the Personal Consumption Expenditure stats.

The last PCE report came out on Friday, and as I expected, inflation is still worse than many people think. The core PCE number rose by 0.6% in August which was 0.1% higher than estimates. Over the past year, core PCE rose by 4.9%. Wall Street had been expecting 4.7%.

The non-core rate rose by just 0.3% in August. Falling energy prices played a big role in keeping that number low. Either way, the annual numbers are running well above the Fed’s target of 2%.

Lael Brainard, the Vice Chair of the Fed and someone who is considered more of a dove, nevertheless spoke in strong terms regarding inflation:

“Monetary policy will need to be restrictive for some time to have confidence that inflation is moving back to target,” the central bank official said in remarks prepared for a speech in New York. “For these reasons, we are committed to avoiding pulling back prematurely.”

Earlier today we got the latest JOLTS report. That’s the Job Openings and Labor Turnover Survey which is put out by the Bureau of Labor Statistics. According to the report, the number of job openings dropped by 1.1 million in August. That’s huge.

The number of available positions fell by 10% to 10.05 million. Wall Street had been expecting 11.1 million. This was the biggest drop since the early days of the pandemic. A major problem for the Fed has been to manage inflation during a very tight labor market. There used to be two jobs for every unemployed person. Now it’s 1.67.

One interesting side note is that lumber prices are back to where they were before the pandemic. That’s a good sign of normalcy. The construction spending report should show a decline of 0.7% in August. Construction spending is still 8.5% above the number from one year ago.

I still think the economy is likely to fall into a recession sometime next year. I suspect it will be a fairly shallow recession, but a lot of this will be determined by how successful the Fed will be in fighting inflation.

Elon Musk to Buy Twitter

It’s really happening! Well, maybe it’s really happening.

This afternoon, news broke that Elon Musk has agreed to buy Twitter (TWTR) for the original offer price of $54.20 per share. (Yes, Musk worked “420” into his offer price.)

If you recall, Musk had originally offered to buy Twitter in April for $54.20 per share, but then he seemed to get cold feet. Instead of simply admitting that, he claimed that Twitter was less than upfront about its user data.

Then the lawyers got involved, and it looked like Twitter was ready to take the matter to court. It’s difficult to imagine a scenario where a person is forced to buy a company even when making commitments to do so, but it looked like that was about to happen. The trial was scheduled to start on October 17.

I’m making a few guesses. The first is that Musk’s lawyers told him that he if were to take it to court, then there’s a very good chance he would lose. In many of the pre-trial motions, the judge repeatedly sided with Twitter.

Musk and Twitter’s management have had a, shall we say, less-than-cordial relationship. Ever since Musk made his original offer, he’s been a constant critic of Twitter, and most importantly, he’s accused Twitter of lying about its number of users.

Another guess of mine is that Musk was simply impulsive, and the “bot issue” was his strategy to back out of the deal. Once it became clear that that wasn’t going to work, Musk chose the best way to lose.

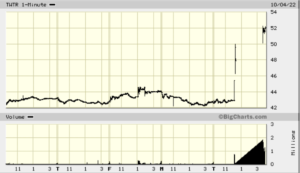

Twitter stuck by the original offer and last month, Twitter shareholders voted to approve the deal. According to a filing with the SEC, Musk made the offer to Twitter yesterday. The stock immediately shot up higher on the news and trading in Twitter was eventually halted. Twitter said it aims to close the deal at the original price.

If you look very closely at this chart, you can make out when the Musk news broke:

How did this all begin? Earlier this year, Twitter suspended the satirical news site called the Babylon Bee for referring to a trans woman as “Man of the Year.” That seems to have spurred Musk on. Twitter has received a lot of criticism for its suspension policies which seem to be arbitrary and politically motivated. I suspect that once Twitter is private, it will allow former President Trump back on the platform.

Given that shares of Twitter closed today at $52 per share, this suggests to me that the market is taking this offer seriously. In fact, the deal may happen quickly. Of course, this is a very different stock market than what we had this past spring.

Another guess is that Twitter’s people told them that the deal is a lot more than Twitter is truly worth. Let’s look at some numbers. Wall Street expects Twitter to earn $1.20 per share this year and 60 cents per share next year. I should add that that’s a major decrease in expectations. Three months ago, Twitter was expected to make $1.68 per share for this year and $1.31 per share for 2023.

Frankly, Twitter simply isn’t that profitable, and it never has been, Personally, I’d be skeptical paying half of Elon’s price. The only hitch is if there’s some way to alter Twitter’s business model to be more profitable. If there is, I don’t know it and I’m not sure Musk does, either. He has said he could get Twitter to 500 million daily users, which is a significant part of the planet.

The lesson here is to be cautious in your business dealings. It may cost you $44 billion.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want to learn more about the stocks on our Buy List, please sign up for our premium service. It’s $20 per month, or $200 per an entire year.

Posted by Eddy Elfenbein on October 4th, 2022 at 7:16 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His