CWS Market Review – November 1, 2022

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The Best Month for the Dow in 46 Years

The Dow Jones Industrial Average just wrapped up its best month since January 1976. For October, the index gained 14.1% while the S&P 500 was up “only” 8.1%.

It’s true that the Dow isn’t a very good index as stock indexes go. It’s simply 30 stock prices added up and adjusted by a divisor. The Dow doesn’t care how big or small the companies are. They’re weighted solely by price which seems pretty silly. Of course, the major advantage the Dow has is that it’s very old.

Still, it’s an achievement to claim the best of anything since 1976. It also underscores something I’ve been talking about recently which is that I’m more impressed by this latest rally than by the previous head fakes.

Indeed, this rally may also prove to be phony, but there are reasons to suspend judgment. The difference is that there may be actual improvements in the outlook for inflation, and by extension, the Federal Reserve’s campaign to increase interest rates.

I’ll give you an example. Last week, I said that the Q3 GDP report might come in better than expected. I was right. For the third quarter, the U.S. economy grew at an annualized rate of 2.6% (after inflation). That’s not great, but it’s better than a recession. Expectations were for growth of 2.3%.

Along with the GDP report, the government also reported the personal consumption expenditure price index. This is the Fed’s preferred measure of inflation. The latest figures show that headline inflation measured 6.2% in the 12 months ending in September. That’s high, but it was 7% in June. The 12-month core rate is 5.1%.

These numbers may indicate that inflation has peaked. I don’t want to be premature, and we need more data before making a firm judgment, but the trend is promising. Compare us to Europe where inflation is running at more than 10%.

All of this is weighing on Jerome Powell and his buddies inside the Federal Reserve. In fact, The Fed started its two-day meeting today. Tomorrow afternoon, we’ll get the latest policy statement. Spoiler alert: The Fed will increase interest rates by another 0.75%.

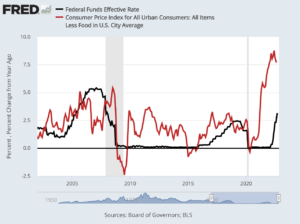

This will be the fourth meeting in a row where the Fed has hiked by 0.75%. This coming rate hike will bring the Fed’s target for short-term interest rates to a range of 3.75% to 4.00%. That means that rates are getting closer to inflation. Soon real rates will actually be positive. That’s something we haven’t seen in a few years.

Here’s the Fed funds rate (black) along with core inflation (red).

With this meeting, I’ll be curious to see if the Fed offers any indication of where it sees interest rates going. After this meeting, the Fed’s outlook will be a lot less clear. The futures market is currently evenly divided on what the Fed will do at its December meeting. Futures traders place about a 50% chance on a 0.50% rate increase and a 50% chance on a 0.75% rate increase. For now, I’d lean towards another 0.75% increase.

These rate hikes are what have hurt the stock market this year. The higher rates have also crushed so many of the former stock market stars. Have you seen Meta Platforms (META) recently? The Zuck has torched an astounding amount of shareholder value. From peak to trough, META has dropped from $384 to $93. That’s a drop of nearly $900 billion.

What’s happened is that higher rates have forced investors to be more conservative. That’s been very good news for our Buy List. Even though it’s been a difficult market, our Buy List has consistently outperformed the S&P 500 since the spring.

At some point, the rate hikes will have to end. That’s good for stocks. It will be clear that the rate hikes are hurting the economy more than inflation. We’re already seeing that in the housing market and with the strong dollar. In Australia, the central bank there recently increased rates by only 0.25%, down from their earlier increases of 0.5%.

The details of the GDP report clearly show what’s happening. Consumer spending is up, but not by a lot. Trade has been quite good, but due to the strong U.S. dollar, that probably won’t last. The most noticeable part of the GDP report is that the housing market is a big drag on the U.S. economy. Housing all by itself knocked 1.4% off of Q3 GDP growth.

I can’t say I’m surprised. Home sales recently posted their longest streak of declines in 15 years. Consumers are getting squeezed by higher prices and slow wage growth. During Q3, Americans saved 3.3% of their after-tax income in the third quarter. That’s the lowest rate in 15 years.

There’s clear evidence of weakness ahead for the economy. Interestingly, Jerome Powell is not a big fan of the 2/10 Spread. Instead, the chairman likes to follow the difference between the three-month Treasury and its implied yield in 18 months. That’s close to inverting. The spread dropped as low as 0.2% recently.

Today we learned that the ISM Manufacturing Index fell to 50.2 last month. That’s barely in the positive range. It means that the manufacturing sector of the economy is still expanding, just very slowly. That’s down from 50.9 in September.

At Bloomberg, they have a model which gauges the odds of a recession starting in the next 12 months. The latest numbers show the odds at 100%. Well, that seems pretty certain. They also polled some economists and they put the odds of a recession at 60%.

The next big test for the market will come this Friday. That’s when the government will release the jobs report for October. In September, the jobless rate was just 3.5% which is low by historical standards. The consensus on Wall Street is to see an increase of 205,000 nonfarm payrolls. However, one weak point is that wages aren’t rising as fast as inflation. The real question is how much the tight labor market is to blame for inflation or, rather, if inflation is due more to supply-chain issues and the war in Ukraine. We’ll find out soon.

Stock Focus: Celanese

This week, I want to look at Celanese (CE), which is one of the more interesting companies around. The company is the world’s leading maker of acetic acid. That’s one of those things that few people even think about, but it’s used in dozens of applications.

Each year, Celanese makes about two million tons of the stuff. That’s about 25% of the world’s supply. The company is based in Irving, Texas and they have manufacturing facilities all around the world. Celanese is also the world’s leading maker of vinyl acetate. That’s a key ingredient in furniture glue. They also make 25% of the world’s supply.

The important fact is that Celanese dominates the market in important things. This is what you think of when Warren Buffett talks about companies that have a strong “moat.” That means that it’s not so easy for a competitor to come along and knock them off their perch.

That’s why I wasn’t surprised when Warren Buffett said that he added Celanese to his portfolio earlier this year. The stock jumped more than 7% on the news. Celanese really is a classic Berkshire kind of stock. The company generates tons of free cash flow.

The big news for Celanese this year is that it agreed to buy the Mobility and Materials division from DuPont for $11 billion in cash. The deal was announced in February, and it was completed today.

The unit had sales last year of $3.5 billion. From the press release, “As part of the transaction, Celanese has acquired a broad portfolio of engineered thermoplastics and elastomers, industry-renowned brands and intellectual property, global production assets, and a world-class organization.”

Celanese has been around for over 100 years. In the 1980s, they spun off their pharmaceutical business, and that’s Celgene. In 1987, Celanese merged with Hoechst to become Hoechst Celanese. That lasted for a few years until Hoechst spun off Celanese. After that, Blackstone bought out Celanese and then quickly IPO’d it in 2005.

There are two important facts to mention about Celanese. The first is that the stock has been a terrible performer lately. In June, the shares were over $160. Lately, it’s been as low at $87. The stock is lower than where it was four years ago.

When I see that a good stock has been behaving badly lately, that scares most people off. It’s natural to judge a stock on its recent performance. Still, I like to find good stocks that have gotten beaten up. The difference is that high-quality companies often bounce back.

I also like the steady dividend. Celanese’s quarterly dividend has gradually increased from four cents per share in 2010 to 70 cents per share this year. At Celanese’s current price, the dividend yields close to 3%.

The other important fact is that Celanese’s profit tends to be very volatile. That’s not necessarily a bad thing. It’s simply the nature of some businesses. Last year, Celanese earned $18.12 per share. That gives the company a trailing Price/Earnings Ratio of about five. Wall Street sees CE’s earnings falling to $17.59 per share this year, and $14.28 per share next year.

It can be a challenge to value a company with such wildly changing numbers. With a consumer staple, it’s pretty easy, but a chemical entity can be frustrating. A better way to look at its earnings is by comparing longer cycles to each other instead of each year.

For Q2, Celanese earned $4.99 per share. Sales were up 13% over last year’s Q2. The company has been able to navigate well with price increases. Having pricing power is also a key ingredient of a business with a wide moat. For the quarter, Celanese had operating cash flow of $495 million and free cash flow of $368 million.

Celanese will report its Q3 earnings on Friday. The company said it expects earnings at the low end of its range of $4.00 to $4.50 per share. Wall Street expects $3.98 per share. CEO Lori Ryerkerk said, “we expect to deliver 2022 adjusted earnings per share approximately in line with our 2021 adjusted earnings per share performance.”

Celanese’s stock is down, but that may not last long.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want to learn more about the stocks on our Buy List, please sign up for our premium service. It’s $20 per month, or $200 per an entire year.

Posted by Eddy Elfenbein on November 1st, 2022 at 6:48 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His