CWS Market Review – August 26, 2016

“Reversion to the mean is the iron rule of financial markets.” – Jack Bogle

I’m enjoying a little time off in sunny Florida. Apparently, the rest of Wall Street is on vacation as well, as the stock market continues its lazy summer.

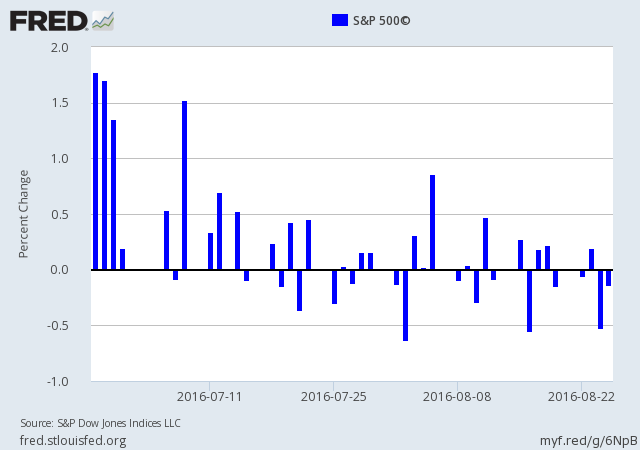

The market’s daily volatility ain’t just low, it barely registers a pulse. Since Brexit, the S&P 500 has now gone 42 straight sessions without a daily decline greater than 0.7%. Compare that with the first 42 days of this year when it happened 15 times!

We also had a very nice earnings report this week from HEICO, our top-performing Buy List stock this year. The company raised guidance for the third time this year, although the shares pulled back on Thursday. I’m actually raising my Buy Below price for HEICO. I’ll have more details in a bit.

Wall Street is looking ahead to Janet Yellen’s speech in Jackson Hole. The speech will come later today. I’ll discuss what it means for us. But first, let’s look at what’s happening just beneath the surface of a very quiet stock market.

Wall Street Warms Up to More Risk

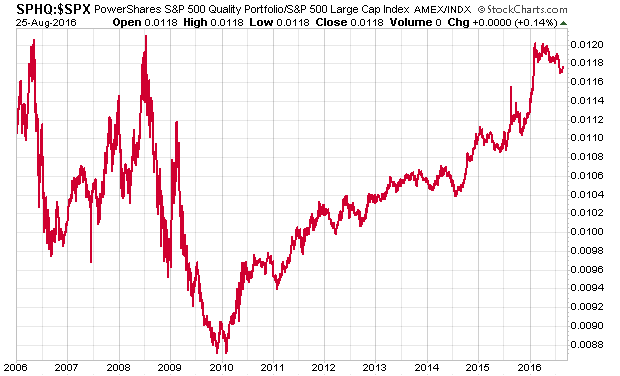

In last week’s issue, I discussed the “low quality rally.” I want to expand on that subject a little bit this week. Standard & Poor’s runs a “High Quality” index for the bluest of the blue chips in the S&P 500. There’s an ETF geared to this index, with the symbol SPHQ. I like to track how well the SPHQ is doing against the broader market. I think of this as a quick-and-easy way of reading the market’s mind, particularly the market’s willingness to take on risk.

High-quality stocks have led the stock market almost continuously since late 2009. But that outperformance really took off at the end of the last year, and it continued into the first few weeks of this year. If you recall, 2016 started out as the worst year on record for stocks. (How times have changed!) By February 11, the market was down more than 10% for the year.

What happened is that everyone got scared and rushed, insanely, to own blue chips at the expense of nearly everything else. Since April, however, high quality has lagged the market. There are two things going on here. First is the unwinding of the fear trend that sent everyone rushing to own high quality. Second, for the first time in a long time, investors are willing to shoulder more risk. Investors need to understand that this is a key turning point for the market.

When the market becomes less afraid of risk, it starts out well, and usually ends very badly. Don’t worry. We don’t have anything to be afraid of on that score. Our Buy List stocks are very high quality. However, we may hit a frustrating patch of underperformance. Again, there’s no need to worry. To everything there is a season—and that includes junky stocks.

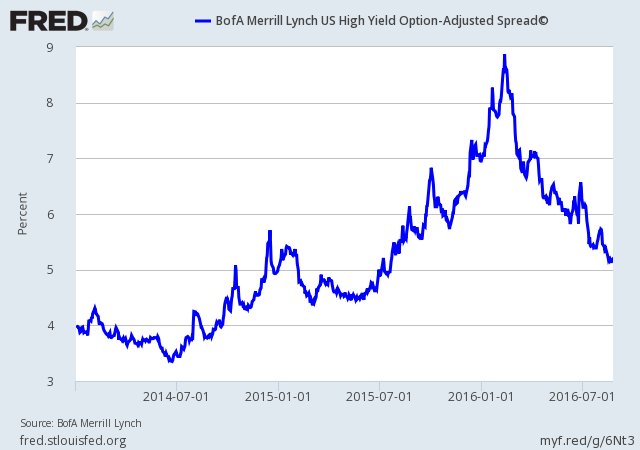

What’s interesting is that we see this same trend being acted out in the junk bond market. When analyzing the market, it’s always important to see if we can spot a similar trend being played out in a different market. At the beginning of the year, everyone was freaking out as they rushed into high-quality stocks; they were also running away from junk bonds. No one wanted any part of anything that had the slightest scent of risk. Junk-bond spreads (meaning the extra yield compared with investment-grade bonds) soared.

The high-yield carnage was also driven by the dramatic plunge in oil prices. Remember that oil will flow as long as credit flows. But once oil gets below around $35 per barrel, lenders get very nervous and demand a greater premium for the honor of using their capital. The oil and junk-bond markets both hit their lows on February 11, along with the stock market. Since then, everything has reversed course. It’s no coincidence that high-quality started to lag a few weeks later.

Here’s the key point I want to convey: oil, stock, high-yield spreads and daily volatility are all interrelated. Many markets, but they all reflect one thing. When daily volatility is so low, there’s more pressure to take on more risk. That means lower junk-bond spreads and lagging performance for investments like SPHQ. When oil rises, lenders are more eager to fund new projects, so yield spreads tighten.

What does this all mean? As investors, we shouldn’t view risk appetite as a good or bad event. It’s more like the tides: it just happens. But I encourage you not to climb the risk ladder in search of better returns. Stick with sound stocks at a good price like you’ll find on our Buy List.

The World Await Yellen’s Speech in Jackson Hole

Fed Chairwoman Janet Yellen is scheduled to speak later today at the Fed’s Jackson Hole conference. The title of the speech is “The Federal Reserve’s Monetary Policy Toolkit.” This has Wall Street a bit nervous. In previous years the Fed has used the Jackson Hole event to announce important policy changes. It’s expected that she’ll sound some hawkish notes, but if you’ve been paying careful attention, that’s pretty much where she’s been this year.

I think the Fed is leaning towards raising rates but they want more evidence that it’s safe to do so. Bill Dudley, the head of the New York Fed, said the central bank could raise rates as soon as next month. John Williams of the San Francisco Fed said he’d hike right now.

The fact is that the economy is improving. The Atlanta Fed GDPNow expects 3.4% growth for Q3. The unemployment rate is holding under 5% and wages are starting to improve. That’s roughly what full employment looks like. The futures market now expects a rate increase in December. Interestingly, they don’t see another rate hike for several months after that.

Still, the bond market seems pretty calm. The two-year yield is good to watch to gauge the bond market’s view of the Fed. The two-year yield has gradually climbed up to 0.79%. That’s up but remember that at the start of the year, the two-year had been yielding over 1%.

I think Janet Yellen will hint that more rate hikes are coming without saying anything concrete. My hunch is that she wants to convey that rates are going up while trying to reassure investors that the pain will be minimal. Now let’s look at our one Buy List earnings report from this week.

HEICO Earns 62 Cents per Share

On Wednesday, HEICO (HEI) reported fiscal Q3 earnings of 62 cents per share. That’s up 22% from last year’s Q3. HEICO isn’t widely followed enough to have a true earnings consensus, but I did see it reported as 59 cents per share. For the year so far, earnings have risen 18% to $1.64 per share.

Sales for the quarter rose 19.1% to $356.1 million. That’s a company record. Sales for the year so far are up 18% to $1,013.0 million.

Laurans A. Mendelson, HEICO’s Chairman and CEO, commented on the Company’s third-quarter results, stating, “Our record quarterly results in consolidated net sales, operating income and net income reflect the impact of our profitable fiscal 2016 and 2015 acquisitions, as well as organic growth within both the Flight Support Group and Electronic Technologies Group.

(…)

As we look ahead to the remainder of fiscal 2016, we anticipate organic growth within our commercial-aviation aftermarket replacement parts and specialty-products product lines moderated by softer demand for certain component repair and overhaul parts and services. Further, we foresee modest full-year organic growth within the Electronic Technologies Group based on current forecasted product demand. During the remainder of fiscal 2016, we plan to continue our focus on new product development, further market penetration, executing our acquisition strategies and maintaining our financial strength.

Based on our current economic visibility, we are increasing our estimated consolidated fiscal 2016 year-over-year growth in net income to 13% – 15%, up from our prior growth estimate of 12% – 14%. In addition, we continue to estimate consolidated fiscal 2016 year-over-year growth in net sales to approximate 15% – 17%, our consolidated operating margin to approximate 18.5% – 19.0%, depreciation and amortization expense of approximately $62 million, capital expenditures to approximate $32 million and cash flow from operations to approximate $220 million.”

This is the third time this year that HEICO has increased its earnings guidance. The company only provides guidance for net income, not earnings per share. Let’s do a little math.

Last year, HEICO earned $1.97 per share. That means an increase of 13% to 15% works out to a range of $2.23 to $2.27 per share. However, HEICO’s shares are 0.4% higher this year, so that will dilute that range by about one penny per share. Since the company has already made $1.64 per share so far this year, we can expect 58 to 62 cents per share for Q4. Wall Street’s consensus, such as it is for little HEICO, was for 64 cents per share. As a result, shares of HEICO lost about 3.4% on Thursday. This week, I’m raising my Buy Below on HEICO to $76 per share.

Buy List Updates

I wanted to pass along some updates on our Buy List stocks.

This week, I want to lower my Buy Below on Alliance Data Systems (ADS) to $220 per share. ADS has pulled back since it had a pretty good earnings report last month. I’m not worried about ADS.

In June, Bad Bath & Beyond (BBBY) said it was buying One Kings Lane. This was part of the company’s effort to beef up its online business. Since the deal was so small, BBBY didn’t have to disclose the price it paid, but we did know that at one time One Kings Lane was valued at $900 million. This week, Recode reported that BBBY paid less than $30 million for One Kings Lane. In other words, it was practically a steal compared to its peak value.

This week, Hormel Foods (HRL) was upgraded by Credit Suisse and Edward Jones. The Credit Suisse analyst raised his price target to $43 per share.

Shares of Express Scripts (ESRX) got dinged for 6% on Thursday. The concern is that Mylan’s plan to cut the cost of EpiPen could hurt their bottom line. Mylan has blamed the “middleman” for higher drug prices. That’s a charge ESRX has strongly denied.

That’s all for now. Next week is the last full trading week before Labor Day. I think we can expect volatility to increase once traders get back from the Hamptons. On Monday, the government will report on personal income and spending. On Thursday we’ll get the ISM and productivity reports. Then on Friday, we’ll get the August jobs report. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on August 26th, 2016 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His