CWS Market Review – September 30, 2016

“If I had to live my life again, I’d make the same mistakes, only sooner.”

– Tallulah Bankhead

Today is the final day of the third quarter, and for the fourteenth time in the last fifteen quarters, this looks to be a positive one for the S&P 500. Despite a modest uptick in volatility this month, the S&P 500 is still less than 2% from an all-time high.

But there’s still a lot of uncertainty for Wall Street, and at the top of the list is Election Day. The polls indicate that it’s a close race between Hillary Clinton and Donald Trump. In this week’s CWS Market Review, I want to address the very sensitive subject of politics and financial markets.

Don’t worry—you won’t hear me spouting off on politics. Quite the opposite. I want to tell you why politics and investing are a bad mix. I always encourage investors to keep their political passions far away from their investing strategies. Going about your investments should be as coldly rational a process as possible. I’ve seen too many investors let their politics ruin a good portfolio.

Later on, I’ll cover some recent news from our Buy List and the economy. The good news is that the economy continues to move along, but at a slow and meandering pace. For the market, we have Q3 earnings season to look forward to in a few weeks. Before we get to that, let’s take a closer look at the dangerous intersection of politics and the stock market.

Keep Politics out of Your Portfolio

Election Day is now less than six weeks away. The election news seems to dominate everything on television, as well as most people’s conversation. Personally, I can’t wait for election season to pass.

There’s a story that Richard Nixon was once asked what he would do if he wasn’t president of the United States. Nixon said that he’d probably be down on Wall Street buying stocks. This led one old-time Wall Streeter to say that if Nixon weren’t president, he too would be buying stocks.

It’s a funny story, but I don’t think it makes for good advice. This often surprises investors, but I don’t believe partisan politics has a strong influence on the stock market. Stocks have done well under both Republicans and Democrats, and they’ve also done poorly under both.

I have many friends who insisted to me that President Obama is a radical socialist, yet the stock market has done very well under his tenure. I also have Democratic friends who think the president deserves most of the credit for the bull market. I’m skeptical. The fact is, the stock market doesn’t really care much who’s president.

This type of analysis misses the point on both what the stock market is, and the powers of the office of the presidency. People assume that presidents are like players in a game, and the stock market is the scoreboard. In my opinion, it’s the exact opposite. The market is always the market. It’s never up for reelection: instead, it’s the politicians who alter their beliefs to assuage the market gods.

James Carville, one of Bill Clinton’s advisors, famously said that if reincarnation is real, he’d like to come back as the bond market because “you can intimidate everybody.”

What the stock market wants is actually quite simple—money. Or more specifically, the net present value of all future cash flows. A strong economy obviously helps, but even the relationship of the market to the economy isn’t always so close. The markets rely on a mystical combination of faith, confidence and patience. Meanwhile, the president is merely the leader of one branch of one of our governments. We’ve seen many times where a president´s agenda has been tripped up by Congress or the courts. Or sometimes, they’re simply overtaken by events.

In 1981, Francois Mitterand, a Socialist, was elected president of France. Soon French money found a new home in New York. The franc dropped sharply, and it threatened to hurt the economy. Mitterand chose reality over his beliefs. That happens all the time.

Let me be clear that government policy does impact the economy, and by extension, the stock market. But those policy decisions are usually well removed from the standard partisan debate. The government shutdown is a good example of a partisan effort that riled investors, but even that didn’t last long. Of course, what the Federal Reserve does is important, but that’s rarely an election issue. Plus, there’s no reason to think that a change at 1600 Pennsylvania Avenue will have a great impact on monetary policy.

My advice is to resist the urge to make a market call based on your opinion of the president. The market truly doesn’t care. Instead, focus on strong companies going for good values. Now let’s look at this week’s economic news.

The Economy Continues to Plod Along

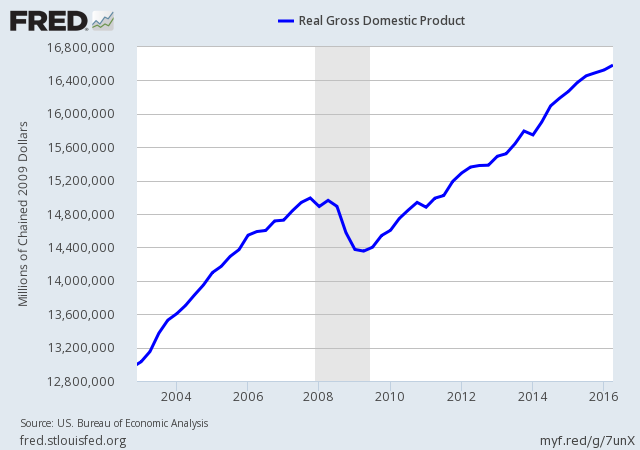

This week, we got more news suggesting that the U.S. economy is moving along, but at a weakly positive pace. On Thursday, the government revised Q2 GDP growth up to 1.4%. This is the seventh quarter in a row where GDP growth has been less than 2.6%. That’s not good.

Of course, the second quarter has long since passed, and we’re not wrapping up Q3. At the end of October, we’ll get our first look at how Q3 did, and the number crunchers at the Atlanta Fed are forecasting growth of 2.8%. That would be very nice to see.

I was very impressed by this week’s consumer-confidence report. Consumer confidence reached its highest level in nine years. That’s very good news, and the resilient stock market may be a reason. I suspect the housing market is playing a role as well.

We also learned that initial jobless claims came in at 254,000. This number tends to bounce around a lot, so economists prefer to look at the four-week average. That number just tied its lowest reading in 43 years. In other words, the jobs market isn’t so bad, but next Friday, we’ll get the big September jobs reports. As much as I want to see the number of new jobs created, I want to see more improvement in wages. The trend here has started to turn positive, but we need more of it. More wages means more buying, which means more sales.

Looking at the housing market, this week’s Case-Shiller report showed that home prices rose 5.1% in the last year. This is key, because housing is the wealth driver of so many Americans. Remember that the business cycle is to a certain degree the same thing as the housing cycle (here’s a good paper on that subject). This recent recession was different because so many homes were built during the bubble, and it’s taken some time for us to burn off the excess inventory. For now, the fundamentals of the housing market are quite solid. Now let’s turn to some recent news impacting our Buy List.

Buy List Updates

There hasn’t been much in the way of earnings lately, but that will change soon. The first Q3 earnings report will come out in two weeks.

I was pleased to see shares of Wabtec (WAB) get a nice bump this week. The company apparently won approval from the EU for its merger with Faiveley. The EU had some anti-trust concerns, but Wabtec said they’d be willing to sell off Faiveley’s brake-pad unit. Shares of WAB had been in a slump, but they’re now close to breaking $80 for the first time since May.

Barclays upgraded Signature Bank (SBNY) to overweight. This stock has been in a downtrend for some time. SBNY may be ready for a turnaround.

More bad news for Wells Fargo (WFC). This time, CEO John Stumpf got grilled by members of the House. He did slightly better this time, but I’m still holding to my belief that he needs to go. Stumpf agreed to forfeit $41 million in compensation, but that’s pocket change for him. If there’s a silver lining, it may lead WFC to break itself up, which would be good news for shareholders.

Societé Generale initiated coverage of Cognizant Technology Solutions (CTSH) with a buy rating. Look for another good earnings report from CTSH next month.

Some large investors are looking to take a big position in Hormel Foods (HRL), and they’re offering a low-ball price for the shares. I think it’s a bad deal, and the company agrees. Stick with Hormel.

That’s all for now. Next week is the start of the fourth quarter. The ISM report will come out on Monday. The last ISM report was pretty weak. We’ll also get a look at auto sales. On Wednesday is the ADP payroll report, plus the ISM Services index. Then on Friday morning, get ready—the government releases the jobs numbers for September. Any strong number will almost certainly be used as evidence that the Fed needs to hike rates in December. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on September 30th, 2016 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His