CWS Market Review – September 8, 2017

“Investing without research is like playing stud poker and never looking at the cards.” – Peter Lynch

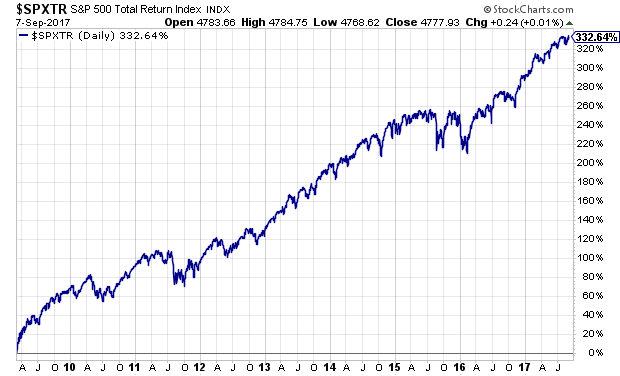

Tomorrow will mark 8-1/2 years of the great bull market. On March 9, 2009, the S&P 500 reached its closing low of 676.53. The previous Friday, March 6, the index touched its sinister-sounding intra-day low of 666.79. To give you an idea of how bleak things were, that morning the government reported that the unemployment rate touched a 25-year high, and the non-farm payrolls report for February came in at -651,000. Yikes!

Things are quite different today. Going by Thursday’s close, the S&P 500 Total Return Index has gained 332.64% in this bull market. That’s enough to turn every $1 into $4.32. This has been one of the longest and strongest bull markets in history, but what’s fascinating is how hated it’s been. Some people just can’t stand to see the indexes rise higher and higher.

We’re constantly told that it’s a reckless bubble that’s all about to crash. Or it’s all due to manipulation from the Fed, and it’s all about to crash. Please. Predicting that the world is about to end is one of the favorite pastimes on Wall Street. Still, the bull marches on. In fact, this year may turn out to be the lowest year on record for the stock market’s volatility.

If there’s a golden rule for long-term investing, it’s that betting on disaster is always overpriced, and betting on “it’ll all work itself out” is always a bargain. In this week’s CWS Market Review, we’ll look at some of the recent economic news. I’ll update you on some Buy List stocks. First, we’ll survey what’s in store for the Federal Reserve. Soon, the Fed will be down to just three members left on the seven-member board.

What’s Next for the Federal Reserve?

Stanley Fischer, the vice-chair of the Federal Reserve, announced this week that he’s stepping down next month. This brings us to an unusual moment for the Fed since there will be four vacancies on the Federal Reserve Board. By law, the FRB has seven slots. By my math, this means that the labor force participation rate for Fed governors is only 43%.

It will soon go even lower since Janet Yellen’s term as Fed chair ends in February. This gives President Trump a big opportunity to put his stamp on the Fed. Officially, Trump has not ruled out reappointing Janet Yellen to another term as Fed chair, but that probably won’t happen. She recently defended some of the post-crisis financial regulations which Trump has promised to repeal.

Quick side note: The appointments to the Fed and of the Fed chair are separate presidential appointments. So if President Trump doesn’t reappoint Yellen as chair, she would still be a Fed member. However, it’s generally assumed she would resign if she were no longer Fed chair.

Fed watchers had assumed that Gary Cohn was Trump’s top choice to replace Janet Yellen. But this week, the Dow Jones reported that it’s “unlikely” Cohn will get the nod due to his criticisms of the president’s response to the terrible events in Charlottesville. Jake Tapper tweeted that one White House source said that Cohn was more likely to get the electric chair than the Fed chair. Ouch.

GOP source close to WH tells me: Cohn "more likely to get electric chair than Fed Chair" https://t.co/5IGR0Db1wU

— Jake Tapper (@jaketapper) September 6, 2017

So who’s next for the position of Fed Poobah? A few names have been thrown around. I would guess that John Taylor at Stanford would be a front runner. He’s widely known for the “Taylor Rule,” which is a guideline for determining where interest rates should be. Frankly, I’m a skeptic on these rules. They’re great in theory, but I’m not sure how they work in real time. But there’s no doubt that Taylor is a highly-qualified choice. Some other contenders are Kevin Warsh, Glenn Hubbard and Jerome Powell.

President Trump has described himself as a “low-interest-rate person,” but I doubt he’s very ideological on monetary matters. This is an important time for the Fed. The central bank wants to unwind its gigantic balance sheet at the same time it’s looking to raise interest rates. It’s not an easy task. With low rates, that weakens the dollar. The euro is near a 33-month high versus the greenback.

I’ve been critical of the Fed lately because I think they’ve moved too quickly on rates. Lately, however, I think the Fed is coming around to my side (more on that in a bit). I think the Fed will remain on a pragmatic and accommodative course over the next few years, and that’s good for investors.

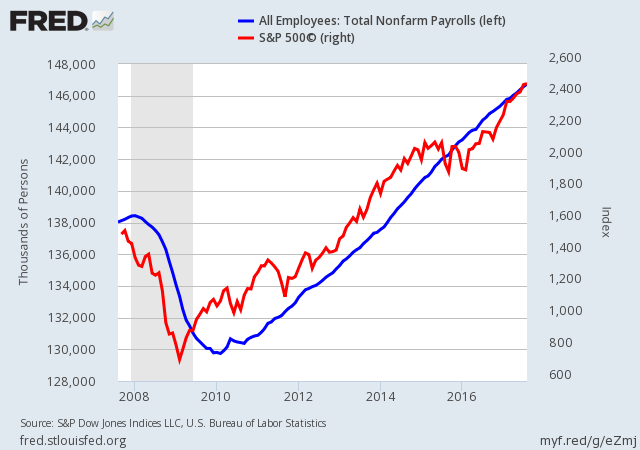

The U.S. Economy Is Gaining Strength

Speaking of the Fed, last Friday we got the August jobs report. It was on the weak side, but nothing too dramatic. Last month, the U.S. economy created 156,000 net new jobs. The numbers for June and July were revised downward. The unemployment rate ticked up to 4.4%, but it’s still near a 16-year low. For the most part, the U.S. economy has created an average of 200,000 jobs a month every month for the last seven years. The numbers haven’t deviated very far from that trend.

While this report wasn’t that bad, I think it finally clued in the bond market that the Fed isn’t going to move on interest rates anytime soon. The equation is simple. When someone asks, “Are stocks cheap?,” the answer is always, “Compared with what?” (Yes, we answer questions with questions.) That’s why interest rates are so important to equity valuations.

Last Thursday, the government released personal-income and spending numbers for July. That report includes the PCE price index, which is the Fed’s preferred measure for tracking inflation. The core PCE number for July rose by just 0.1%. It was the same in June. For the past year, core PCE is up 1.4%. In other words, inflation is hardly a problem. Next week, we’ll get the CPI report for August, and I expect to see much of the same.

With so little happening with inflation the Fed may be convinced to back down. The FOMC is set to meet again on September 20, and I strongly doubt they’ll do anything. The futures market thinks there’s only a 26% chance the Fed will raise rates before the end of the year. I’d say that’s about 20% too high. The Fed funds futures are now priced to show a 54% chance of no rate hike in the next 12 months. That’s a stunning reversal of sentiment. Late last year, the Fed was calling for three hikes this year, plus three more in 2018 and three more in 2019. All that’s gone now.

One potential roadblock for the economy could be the impact of Harvey and Irma. We don’t know yet the full measure of these events. On Thursday, we got our first glimpse of what Harvey could mean. Initial jobless claims soared to 298,000. That’s a rise of 62,000. As a metric, initial jobless claims have the benefit of being early, but that’s at the expense of being noisy. We saw similar jumps with previous storms.

The recent economic numbers look quite good. Q2 GDP came in at 3%. Last week, we learned that personal income rose by 0.4% in July while personal spending rose by 0.3%. That’s quite good. Also, Friday’s ISM report was the best in six years. This suggests the economy got off to a strong start for Q3. The Atlanta Fed’s GDPNow model now says that Q3 GDP grew by 3.3%. I’m wary of such models, but I hope that number is right.

Buy List Updates

Cinemark (CNK) got trashed for a 5% loss on Thursday. What happened? Disney came out with details on its streaming service. Marvel and Star Wars will be exclusive to Disney and not on Netflix. This was a rough summer for the movie biz, but as far as earnings go, Cinemark is doing well. They missed earnings last quarter by one penny per share, yet the stock has been hammered. Cinemark is now going for less than 14 times next year’s estimate. As of now, there’s no evidence that the recent news is hurting CNK’s business. I’m looking for a turnaround for shares of CNK.

Cerner (CERN) broke out to a new 52-week high this week. CERN is still shy of its all-time high of $75 from two years ago. The stock is having a great year for us (+45.7%). I’m going to hold off raising my $68 Buy Below price for now. Cerner could turn into a big winner for us.

I’m ready to declare Signature Bank (SBNY) a very good bargain. The shares are now down to $122. The bank has basically erased nearly everything it gained in the post-election boom. Yes, SBNY has its issues, but the numbers have been solid. I think it’s possible SBNY can earn $10 per share next year.

That’s all for now. There’s not much in the way of economic news next week. I’ll be keeping an eye out for Wednesday’s report on the Federal Budget. The deficit is shaping up to be worse than originally thought. This comes after years of decreasing deficits. On Thursday, we’ll get the CPI report for August. Inflation has been quite tame for the last few months. Let’s see if that trend continues. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on September 8th, 2017 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His