CWS Market Review – January 12, 2018

“Stock market: a place where events with a <1% probability are discussed >90% of the time.” – Urban Carmel

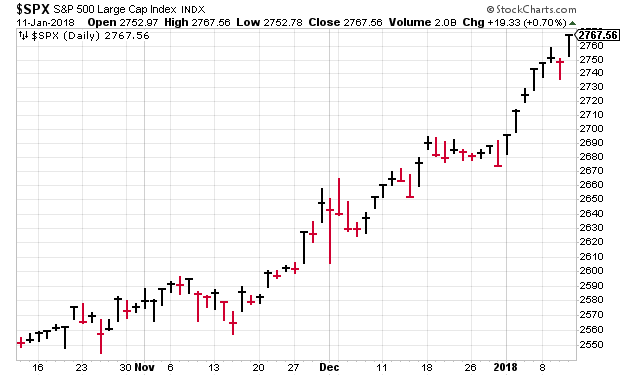

The year 2018 is picking up where 2017 left off. The market has risen for seven out of eight days this year. In fact, this is one of the best starts to a year in market history. The S&P 500 is already up 3.5% this year, and we’re not even at the Super Bowl.

The good news is that the economy continues to do well. We’re probably growing at the strongest rate in several years. Very soon, we’re going to get a lot more evidence for stronger growth as the fourth-quarter earnings season beings. This looks to be a good one for corporate America, and expectations are high. Naturally, we’ll also get a look at how well our Buy List stocks did.

In this issue of CWS Market Review, I want to focus on the upcoming earnings season. I also want to look at the impact of tax reform on the stock market and discuss the recent uptick in long-term yields. Later on, I’ll have some updates on our Buy List stocks (good news from Danaher!). But first, let’s see why corporate tax reform was so important for us.

The Impact of Tax Reform on Our Portfolios

As we know, the stock market has been in a good mood lately. Actually, it’s been this way for close to two years without interruption. On February 11, 2016, the S&P 500 closed at 1,829.08. Since then, the index has advanced 51.3%. Not only that, it’s been a very stable market as well. Since March 2016, the S&P 500 has spent exactly one day below its 200-day moving average.

Part of the reason for the buoyant outlook is tax reform. Last month, Congress passed and President Trump signed a major tax bill. I won’t go into the wisdom of the policy proposals because that’s a political decision and not what we focus on around here.

I do, however, want to make a few comments about the change in corporate taxes and how it impacts investors. The tax law lowers the corporate rate from 35% to 21%. Effectively, what that means is that the U.S. government is a silent partner in every American business.

Previously, they had an odd relationship with the partners as the government owned no part of the business yet was entitled to 35% of the final cash flow. All the other shareholders got the other 65%.

With this new law, the shareholders’ stake rises from 65% to 79%. They get an extra 14% at no cost. Imagine if you had a silent partner who said to you, “here, take my 14% and you don’t owe me anything.” Of course, that’s not literally what’s happened. But effectively, it’s pretty darn close.

This is a huge benefit for shareholders. It’s almost like overnight you got 20% more shares of all your stocks. This is especially good for many of our Buy List stocks because they’re very profitable. That’s why they pay a lot of taxes.

I tend to be skeptical of any models that try to determine a fair price for the entire market. This is an instance where the entire climate has changed. If I were a modeler, I’d have to update several of my variables (and not a few of my constants).

As good as this is for shareholders, and it is good, we should keep in mind that the government may easily change its mind at some point. The political climate, alas, is ever fickle.

Keep an Eye on Rising Long-Term Yields

Last Friday, the government reported that the U.S. economy created 148,000 net new jobs in December. That was less than expected, but the trend is still very much intact. The unemployment rate stayed at 4.1%. The important number is that average hourly earnings were up 2.5% for the year. That really needs to increase. Higher wages means more shopping which means more profits.

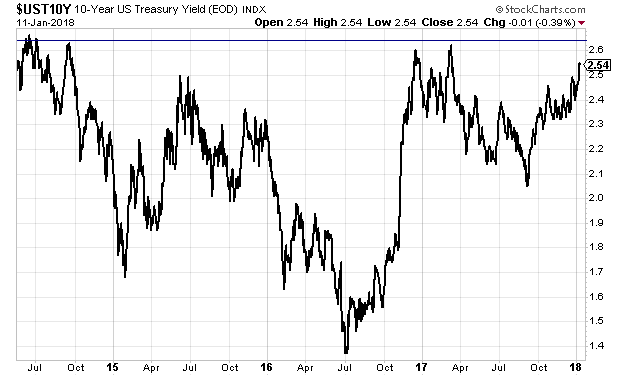

While inflation has remained quite low, I’ve started to notice that long-term interest rates have gradually crept higher in recent weeks. This week, the 10-year broke above 2.5%. One more push and the yield can easily touch a three-year high.

Some of this is due to the improving economy. As cyclical stocks improve, that’s usually matched by a rise in long-term rates. What happens is that investors shun lower-risk bonds and rotate into higher-risk stocks. That’s also part of the reason why defensive sectors like Consumer Staples (like Hormel and Church & Dwight) have sat out this latest rally. We’ll get the first look at Q4 later this month and I think it will be a good report. We might even top 4% growth.

Some of the rise in long-term rates is related to the Fed’s aggressive posture. The central bank sees three more rate hikes this year. The futures market has priced in a rate hike in March (68%) and a second by September (71%), but they’re currently divided on a third (45%) by December.

The reason why the rise in long-term rates is important is that it’s a crucial factor in stock valuations. Whenever someone asks, “are stocks expensive?,” the proper answer is “compared to what?”

In terms of risk, stocks are closest to long-term bonds. That means that higher yields from bonds provide tougher “competition” for stocks. (This is why so many market models use long-term yields as an input variable.) If stocks want to compete for investors’ money, they may have to lower their valuation. This doesn’t necessarily mean lower prices. It just means that prices will rise less than earnings.

Mind you, we haven’t reached a breaking point yet. Long-term yields are still quite modest. But there is some math involved, and stock valuations can’t hold out forever—even with tax reform.

The key takeaway is that the market is taking a more relaxed attitude toward risk. This isn’t necessarily a bad thing. Marginal assets serve an important purpose. Fortunately, our Buy List is pretty conservative, so it’s more protected against a broad-based change in valuations.

When the 10-year yield was 1.4%, as it was 18 months ago, stocks were an easy call. Heck, even if they went nowhere, you were still getting a 2.2% yield. But what happens if the 10-year gets to 3%? Or 4%?

In 1994, the bond market tanked, profits soared and stocks were flat. That’s another way of saying valuations plunged. Sometimes the bear growls, and sometimes he does his work in silence.

This Quarter’s Earnings Calendar

Like I do each quarter, I’ve posted an earnings calendar for our Buy List stocks. For Q4, companies tend to report a little later than they normally do in other quarters. Twenty of our Twenty-five stocks will report from mid-January to mid-February. I do my best to compile the info. Let’s just say that some companies are more forthcoming than others.

I want to add a side note on the earnings report for Signature Bank (SBNY). The company hasn’t said yet when they’ll report earnings. Going by previous quarters, the report may come next week. Signature is usually one of our first stocks to report. Unfortunately, I wasn’t able confirm the earnings date by the time I’m sending you this. So if you see Signature’s earnings next week, don’t be surprised. Wall Street expects $2.23 per share for Q4. Please check the blog for updates. The week after next will be a busier week for earnings. Now let’s look at some recent news from our Buy List stocks.

Buy List Updates

On Tuesday, Stryker (SYK) released preliminary quarterly results. For Q4, sales rose by 10% to $3.5 billion. Taking out the impact of the dollar, sales were up 8.1% last quarter. Stryker said that based on those numbers, they expect 2017 earnings of $6.35 to $6.45 per share. Since Stryker has already made $4.53 per share for the first three quarters, that implies Q4 earnings between $1.82 and $1.92 per share. Stryker’s earnings report is due out on January 30.

Shares of Danaher (DHR) got a nice bounce this week after the CEO gave some optimistic comments at an investor conference. See “Danaher Simply Blew It Away at This Big Healthcare Conference Tuesday” at The Street. Danaher’s CEO said that earnings will come in at the top of their range, which is $1.12 to $1.16 per share. Last month, Danaher said they expect 2018 earnings between $4.25 and $4.35 per share.

Before I go, I want to update a few of our Buy Below prices. Remember that these prices are not “price targets.” I’m not a fan of those. Rather, they’re guidelines for current entry into the stock.

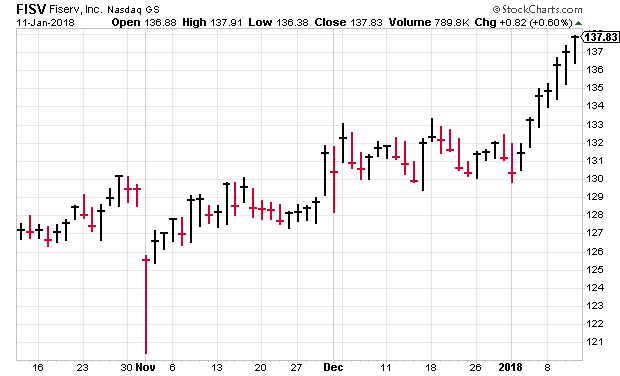

I’m lifting my Moody’s (MCO) Buy Below to $164 per share. The credit-agency stock is already up more than 5% for us this year. I’m also lifting Intercontinental Exchange (ICE) to $79 per share. ICE is due to report earnings on February 7. Look for another good earnings report. Lastly, I’m lifting Fiserv (FISV) to $144 per share.

A quick reminder on Fiserv. In their last earnings report, the company missed Wall Street’s consensus by four cents per share. The next day, the stock dropped as low as $120.53 which was a 7% loss.

Here’s what’s interesting: In the earnings report, Fiserv also narrowed its earnings guidance. Traders naturally skipped over the good news and ignored the fact that Fiserv raised the lower end of its guidance.

Now here we are two months later, and Fiserv closed out Thursday at $137.83 per share. This is another example of how we kept our heads and focused on the details and thereby made a nice profit.

That’s all for now. The stock market will be closed on Monday in honor of Dr. Martin Luther King’s birthday. Dr. King would have been 89. We’ll start to get some big-name earnings reports next week. The industrial-production report is due out on Wednesday. On Thursday, the housing-starts report comes out. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

P.S. Important update. Shareholders of my AdvisorShares Focused Equity ETF (CWS) should have received proxy voting materials in mid-November. If you have not already done so, it is very important to record your vote.

For many shareholders, proxy materials are available online through the brokerage firm where the account is located. The proxy materials will include instructions on how to vote online, by phone or by mail. Below are these voting options. As noted in the proxy materials, the Board of Trustees recommends voting “For” each proposal.

INTERNET: Go to www.cesvote.com. Have your proxy card available when you access the above website. Follow the prompts to vote your shares.

PHONE: Call (888) 693-8683. Use any touch-tone telephone to vote your proxy. Have your proxy card available when you call. Follow the voting instructions to vote your shares.

MAIL: Mark, sign, and date your proxy card, then detach it, and return it in the postage-paid envelope provided.

Your efforts are greatly appreciated. You may also call the team at AdvisorShares at 877-843-3831 if you have any questions.

Posted by Eddy Elfenbein on January 12th, 2018 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His