CWS Market Review – April 26, 2019

“Every day, I assume every position I have is wrong.” – Paul Tudor Jones

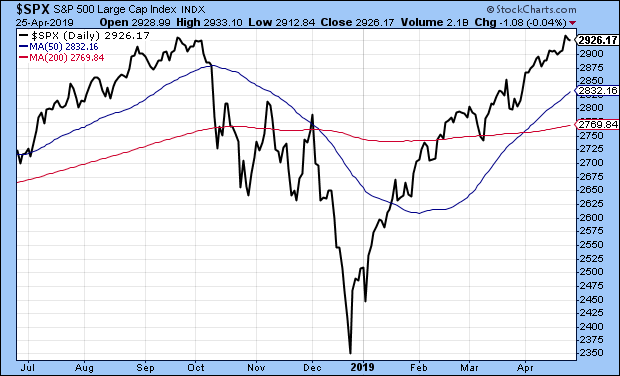

Now that earnings season is in full swing, Wall Street is in its happy place. Truthfully, earnings really aren’t that great this season, but they’re better than they could have been. At least traders are happy. On Tuesday, the S&P 500 closed at a fresh all-time high. This means that we made back everything we lost in a nasty correction that lasted from late September to late December.

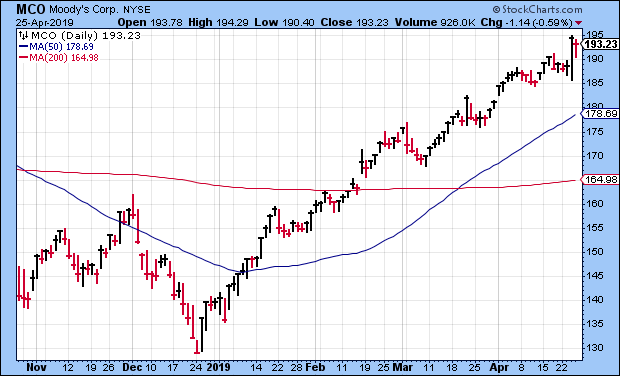

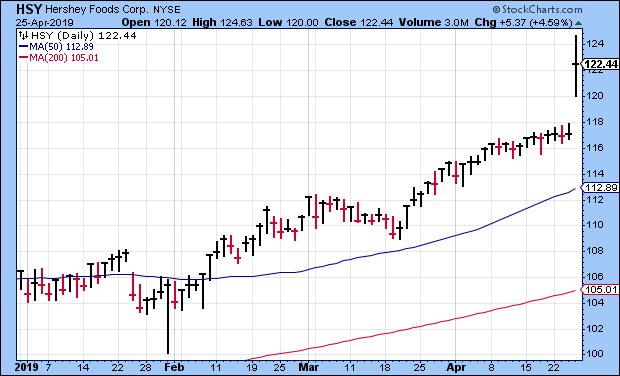

We had lots of Buy List earnings reports this week. Moody’s jumped 3% on a very good report. It’s now a 38% winner on the year for us. Hershey beat estimates and gapped 5% to a new high. Cerner raised guidance. Stryker beat and raised guidance. Raytheon creamed estimates, and AFLAC beat as well. Sherwin-Williams shook off a tepid earnings report. I’ll go over all our earnings reports from this week. I’ll also preview a slew of Buy List earnings reports headed our way next week.

Here’s our updated Earnings Calendar:

Twenty of our 25 Buy List stocks are reporting their Q1 earnings this cycle. Here’s a list of reporting dates, Wall Street’s consensus estimates and actual reported results.

| Company | Ticker | Date | Estimate | Result |

| Eagle Bancorp | EGBN | 17-Apr | $1.12 | $1.11 |

| Signature Bank | SBNY | 17-Apr | $2.77 | $2.65 |

| Torchmark | TMK | 17-Apr | $1.59 | $1.64 |

| Check Point Software | CHKP | 18-Apr | $1.31 | $1.32 |

| Danaher | DHR | 18-Apr | $1.01 | $1.07 |

| Sherwin-Williams | SHW | 23-Apr | $3.69 | $3.60 |

| Stryker | SYK | 23-Apr | $1.84 | $1.88 |

| Moody’s | MCO | 24-Apr | $1.93 | $2.07 |

| AFLAC | AFL | 25-Apr | $1.06 | $1.13 |

| Cerner | CERN | 25-Apr | $0.61 | $0.61 |

| Hershey | HSY | 25-Apr | $1.46 | $1.59 |

| Raytheon | RTN | 25-Apr | $2.47 | $2.77 |

| Fiserv | FISV | 30-Apr | $0.82 | |

| Church & Dwight | CHD | 2-May | $0.66 | |

| Cognizant Technology Solutions | CTSH | 2-May | $1.04 | |

| Continental Building Products | CBPX | 2-May | $0.34 | |

| Intercontinental Exchange | ICE | 2-May | $0.90 | |

| Broadridge Financial | BR | 7-May | $1.50 | |

| Disney | DIS | 8-May | $1.55 | |

| Becton, Dickinson | BDX | 9-May | $2.58 |

There’s a lot to get to this week, so let’s jump right in.

Earnings from Stryker and Sherwin-Williams

We had two earnings reports on Tuesday. Before the opening bell, Sherwin-Williams (SHW) reported Q1 earnings of $3.60 per share. That was below estimates of $3.69 per share. Sales rose 1.9% to $4.04 billion.

Here’s the important fact for investors: The company didn’t alter its full-year outlook of $20.40 to $21.40 per share (that excludes acquisition costs). That compares with $18.53 per share a year ago. For Q2, Sherwin expects sales to rise by 2% to 5%. For the full year, they expect sales to rise by 4% to 7%. This isn’t terrible news.

Here’s what the CEO had to say:

Commenting on the first quarter, John G. Morikis, Chairman and Chief Executive Officer, said, “We made good progress on our pricing initiatives across all segments during the quarter and effectively managed SG&A spending, but volumes fell short of expectations due to a slower start to the architectural painting season in North America and continued challenging conditions in many end markets outside North America. Despite the volume shortfall and higher year-over-year raw material costs, consolidated Company adjusted gross margin, which excludes acquisition-related costs, improved sequentially and was flat year-over-year. We expect the positive trend in gross margin and operating expense control to continue as the year progresses, and volume growth should also improve over the balance of the year, particularly in the back half.

“Looking at our performance by segment, in The Americas Group, despite a strong backlog and project pipeline reported by many of our professional customers, volume growth in the quarter was slower than expected. We continued to invest by opening 15 net new store locations in The Americas Group during the quarter. In our Consumer Brands Group, most of the softness in demand in the quarter was in markets outside North America. Consumer Brands Group adjusted segment operating margin in the first quarter expanded sequentially and year-over-year, and we are very well positioned across all North American retail channels heading into the important spring selling season. Performance Coatings Group achieved modest sales growth and increased adjusted segment operating margin in the quarter against year-over-year raw material pressure.”

Sherwin is fundamentally sound. I think the weakness they had in Q4 is behind them. Reaffirming guidance is a key move. I’m lifting my Buy Below on Sherwin to $460 per share.

Last week, I told you Stryker (SYK) had a good shot at beating expectations, and I was right. The company reported Q1 earnings of $1.88 per share, which beat the Street by four cents per share. That’s an increase of 11.9% over last year. Net sales rose 8.5% to $3.5 billion, and organic net sales increased by 7.3%. For the quarter, Stryker’s adjusted operating margin was 25.1%.

Now for guidance. For Q2, Stryker expects earnings between $1.90 and $1.95 per share. Wall Street had been expecting $1.96 per share. For the full year, Stryker sees earnings between $8.05 and $8.20 per share. That’s an increase of five cents per share to the low end. Wall Street was at $8.13 per share.

This is a really good stock. Stryker remains a buy up to $192 per share.

Moody’s Is a Buy Up to $200 per Share

On Wednesday, Moody’s (MCO) released a very good earnings report. The credit-ratings agency reported Q1 earnings of $2.07 per share. That beat estimates by 14 cents per share. The stock gapped up 3% on Wednesday.

Revenue at Moody’s Analytics rose 16%. The company stood by its full-year forecast of $7.85 to $8.10 per share. Moody’s is our top-performing stock this year with a YTD gain of 38%. I’m lifting my Buy Below on Moody’s to $200 per share.

Earnings from AFLAC, Hershey, Cerner and Raytheon

On Thursday, we had four more Buy List earnings reports. Let’s start with AFLAC (AFL). The duck stock had another good quarter. For Q1, AFLAC had adjusted operating earnings, not including currency, of $1.13 per share. That beat estimates by seven cents per share.

The supplemental insurer expects to buy back between $1.3 billion and $1.7 billion in shares this year. AFLAC recently raised its dividend for the 36th year in a row. For 2019, AFLAC is standing by its previous guidance for earnings of $4.10 to $4.30 per share. That assumes the yen trades at ¥110.39 to the dollar.

This means AFLAC is currently going for about 12 times this year’s earnings. Buy up to $50 per share.

Last quarter, Cerner (CERN) did what I pretty much expected. The healthcare-IT folks earned 61 cents per share. That was in the center of their guidance. Sales rose 8% to $1.39 billion.

For Q1, Cerner had operating cash flow of $317.1 million and free cash flow of $123.5 million. For Q2, Cerner expects earnings of 63 to 65 cents per share on revenue of $1.41 to $1.46 billion.

For all of 2019, Cerner sees earnings of $2.64 to $2.72 per share. That’s up from the previous guidance of $2.57 to $2.67 per share. Cerner recently said it had reached an agreement with Starboard Value to start paying a dividend and increase its buyback authorization by $1.5 billion. Cerner is a solid stock. Buy up to $66 per share.

Hershey (HSY) rebounded well after the disappointment from Q4. For Q1, the chocolatier had adjusted Q1 earnings of $1.59 per share. That’s an increase of 12.8% over last year. It also beat Wall Street’s consensus by 13 cents per share.

Hershey reiterated its full-year guidance of $5.63 to $5.74 per share. The shares jumped 4.6% on Thursday and broke out to a new 52-week high. Notice how good companies always bounce back. I’m raising my Buy Below on Hershey to $126 per share.

Raytheon (RTN) shot a tomahawk missile at its earnings estimates. For Q1, the company made $2.77 per share which was 30 cents more than expectations. Wow! Raytheon made $2.20 per share for last year’s Q1.

The company is doing especially well with cyber-security and its intelligence and information unit. Despite the impressive earnings beat, Raytheon didn’t change its full-year earnings guidance of $11.40 to $11.60 per share and sales guidance of $28.6 billion to $29.1 billion. I think that disconcerted some traders, and the shares pulled back 4.4% on Thursday.

Last month, Raytheon hiked its dividend by 8.6%. That was its 15th annual dividend increase in a row. Raytheon remains a buy up to $190 per share.

Five Buy List Earnings Reports Next Week

We have five more Buy List earnings reports next week. Let’s start with Fiserv (FISV), which reports on April 30. Three months ago, the company had an uncharacteristically underwhelming earnings report. They missed the Street by two cents per share, and earnings came in at the low end of their guidance.

Am I worried? Not at all. Despite the earnings miss, Fiserv had Q4 earnings growth of 24%, and operating margin came in at 33.4%. For the year, Fiserv made $3.10 per share. This was their 33rd year in a row of double-digit earnings growth. On top of that, Fortune named Fiserv to their list of most-admired companies for the sixth year in a row.

For 2019, Fiserv expects earnings to range between $3.39 and $3.52 per share. They’ll need to get above $3.41 to extend their double-digit streak. Fiserv also said they expect the First Data deal to close in the second half of 2019. For Q1, Wall Street expects 82 cents per share.

We have four more earnings reports on May 2.

Three months ago, Church & Dwight (CHD) missed Q4 estimates by a penny per share. The stock got clobbered, but I wasn’t too worried. The CEO noted that they were hitting 2019 “with momentum,” and that they have price increases on the way. Wall Street expects Q1 earnings of 66 cents per share.

The big news at Cognizant Technology Solutions (CTSH) is that Brian Humphries has taken over as CEO on April 1 from Francisco D’Souza, who has been CEO since 2007. D’Souza has done a great job, and he’ll remain a member of the board.

For 2019, Cognizant sees earnings of at least $4.40 per share. Wall Street had been expecting $4.45 per share. The company didn’t provide EPS guidance for Q1, but they said sales growth should be between 7.5% and 8.5%. Wall Street expects $1.04 per share, which sounds about right.

Continental Building Products (CBPX) may be our most dramatic stock. In February, the wallboard company soared 8% after its Q4 earnings report matched expectations. Of course, that makes you wonder what expectations really were. I suspect Wall Street has been secretly expecting much worse.

Yet after the initial surge, Continental turned around and gave it all back. The company gives guidance on several metrics but not EPS. For 2019, Continental sees SG&A of $40 million to $42 million and capital expenditures of $28 million to $32 million. Cost-of-goods-sold inflation per unit compared with 2018 is expected to be 4.5% to 6.5%. For Q1, Wall Street expects 34 cents per share.

Last year was Intercontinental Exchange (ICE)’s 13th straight year of record revenues. I think they have a good chance of making this year number 14. For 2018, ICE made $3.59 per share. That’s up 21% over 2017. ICE’s operating margin was an impressive 58%. ICE provides guidance for several metrics except EPS. For Q1, Wall Street expects 90 cents per share, which should be beatable.

That’s all for now. Next week will have it all—more earnings, the April jobs report, the new ISM report, and if that’s not enough, there’s a Fed meeting as well. On Monday, we get personal income. The Federal Reserve meets on Tuesday and Wednesday. The policy statement will come out on Wednesday at 2 pm. Don’t expect any change on rates. Then on Friday, the government releases the April jobs report. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on April 26th, 2019 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His