CWS Market Review – May 15, 2020

“Selling your winners and holding your losers is like cutting the flowers and watering the weeds.” – Peter Lynch

Shortly after I sent you last week’s issue, the Labor Department reported that the U.S. economy shed 20.5 million jobs during April. That’s a staggering loss. The unemployment rate jumped to 14.7%. That’s a level we haven’t seen since the Great Depression.

Federal Reserve Chairman Jerome Powell said, “Among people who were working in February, almost 40% of those in households making less than $40,000 a year had lost a job in March.” Interestingly, Powell made those remarks in an online speech. A sign of the times.

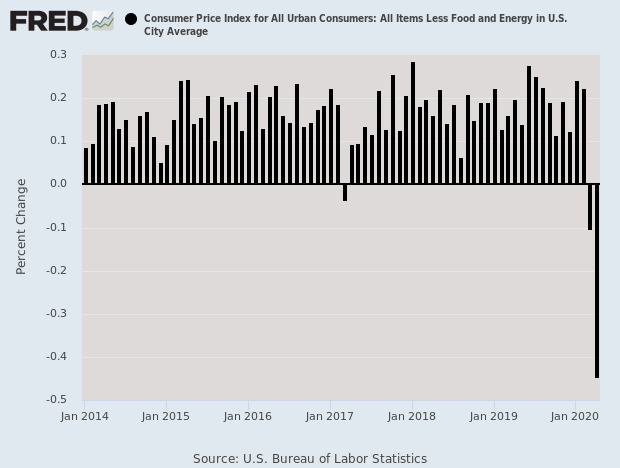

It doesn’t end there. On Tuesday, the government’s Consumer Price Index report showed that consumer prices fell 0.8% in April. In other words, we had actual deflation. That’s also something we had during the Depression. This is the second month in a row of lower prices. Core inflation was down 0.4% (see below) which is the lowest drop since the government started tracking the data in 1957.

Our last three issues have been devoted to earnings. This week, I want to shift back to the economy and stock market. While the economic news is quite dire, the stock market is holding up reasonably well. I’ll explain what’s going on.

I’ll also discuss the final earnings report we had this season, which was from Broadridge Financial Solutions. And I’ll close by previewing two earnings reports coming our way next week. These are for companies whose reporting quarter ended in April.

But first, let’s talk…basketball.

We’re Not Going Back to Normal

I want to talk about basketball and the three-point shot, but what I’m really talking about is economics and incentives—i.e., psychology and behavior. Bear with me for a brief digression.

In the 1979-80 season, the NBA introduced the three-point shot. It had actually been used in the old ABA. At first, the three-pointer was a complete flop. Few teams used it. The Los Angeles Lakers won the NBA championship that year and only made 20 three-pointers all season. That’s fewer than one for every four games. The next year, three-pointer attempts dropped by nearly 30%.

Then in 1994, the NBA decided to act. The league moved the three-point line forward by 21 inches to increase its popularity. Seen through the lens of economics, the authorities incentivized the tactic. The next year, three-pointers took off. Teams tried more three-pointers, and their success rate increased. Successful three-point shots jumped by 65%.

Here’s the interesting part. After three seasons, the league moved the three-point line back to where it had been. What did teams do? The number of attempts fell, but it was still far higher than it had been.

What happened is that teams had been incentivized to try a new tactic. They saw its benefit, and even after the incentive was removed, they still used the tactic. Once you see a new way of doing things, you may not want to go back. Nowadays, teams try twice as many three-pointers as they did in the mid-1990s when the line was 21 inches closer.

Now let’s look at the current economy. Imagine a student who has borrowed fantastic amounts of money to attend college. For the last few weeks, he or she has been taking classes online. Seems pretty easy. Just open your laptop and presto: you’re in class. What’s the benefit to leaving your house to go to class when technology can bring it to you? On top of that, there are other costs like commuting in a car on a congested highway.

Now let’s say you work at, for example, an accounting firm or publishing company. How many employees need to be in the physical office each day? I recently had an afternoon packed full of Zoom meetings. I’m sure many of you have had the same.

As the economy reopens, I don’t see us returning to status quo ante. Most companies will adjust, but some are in trouble. In 1978, Polaroid employed 21,000 people. It doesn’t anymore. The world changes very quickly.

The Plunge in Financial Stocks Gives Us Some Bargains

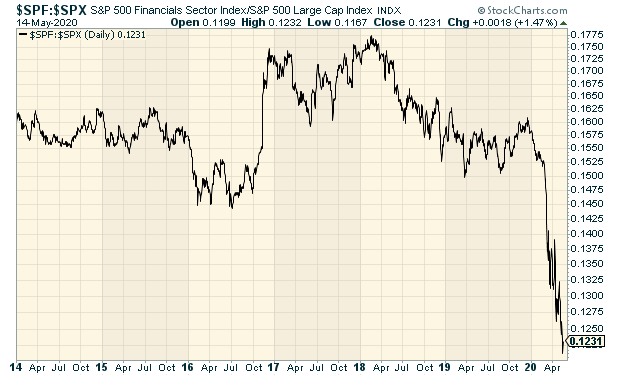

Financial stocks have been lagging badly recently. In fact, they lagged during the last gasps of the bull market earlier this year. They then lagged during the big plunge, and they’re lagging again during the market recovery. What’s going on?

I suspect that we’re getting used to a new world of low interest rates. In fact, I think there’s a good chance rates will soon go negative. When you have deflation—or rather, increasing deflation—that means that even when the Fed holds rates at next to nothing, real rates are increasing. Thanks to deflation, the Fed is tightening money by doing nothing. The financial sector is flailing.

Here’s a chart of the S&P 500 Finance Index divided by the S&P 500.

This has had a big impact on the three financial stocks in our portfolio: Eagle Bancorp (EGBN), Globe Life (GL) and AFLAC (AFL). I’m not worried about any of them. I think AFLAC is an especially good buy if you can add shares below $35. Based on Thursday’s close, AFL’s dividend yields 3.4%.

As a general rule, a stock is impacted by three variables: the overall stock market, the industry group, and the nature of the company itself. The last one is the most important in the long run, but the first two can play a big role in the near term. Even the best stocks will get swept up by a ferocious bear market. That’s why, as a stock-picker, I like to look at the best names in the weakest sectors.

In addition to AFLAC, there are a few good bargains on our Buy List. I like Middleby (MIDD) below $60 per share. I also like Stryker (SYK) here. The last earnings report was quite good. Now let’s look at our final earnings report for the Q1 earnings season.

Earnings from Broadridge Financial Solutions

On Friday, Broadridge Financial Solutions (BR) reported fiscal Q3 (ending in March) earnings of $1.67 per share. That was five cents below Wall Street’s estimate.

The CEO noted that recurring revenues rose 9% and adjusted EPD increased by 5%. That’s quite good in this environment. Traders didn’t seem terribly worried about the earnings miss as the shares initially advanced after the earnings report. On Tuesday, the stock briefly cracked $120 per share.

This report was actually a bit reassuring to me because Broadridge had bombed the previous report. The company also updated its guidance for this fiscal year which has just one quarter left.

Broadridge expects recurring revenue growth of 8% to 10%. They expect overall revenue growth to be at the low end of their range of 3% to 6%. BR lowered its EPS growth range from 8% to 12% down to 5% to 7%.

Let’s do some math. Last year, the company made $4.66 per share, so the new range means they expect earnings between $4.89 and $4.99 per share. Since BR has already made $2.88 per share in the first nine months of this fiscal year, that implies Q4 earnings of $2.01 to $2.11 per share. Wall Street had been expecting $2.11 per share.

Broadridge Financial Solutions is a buy up to $130 per share.

Earnings Preview for Hormel Foods and Ross Stores

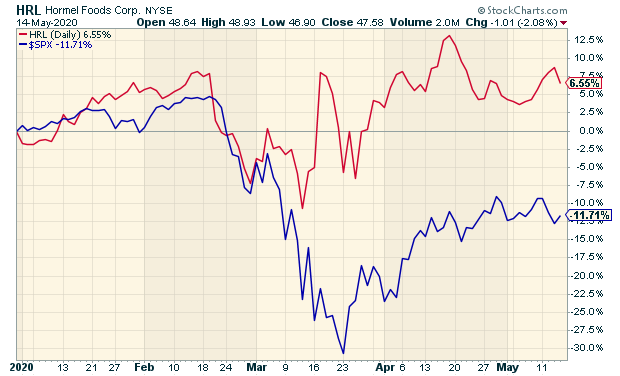

We have two earnings reports scheduled for May 21. Let’s start with Hormel Foods (HRL). The Spam people ended their fiscal Q2 on April 30.

For Q1, Hormel made 45 cents per share which matched Wall Street’s expectations. For the quarter, organic sales were up 4%. The company reiterated its full-year 2020 forecast for sales ranging between $9.5 billion and $10 billion and EPS between $1.69 and $1.83.

What’s interesting is that Hormel does a lot of business in China, so they were one of the first to see an economic impact from the coronavirus. For Q2, Wall Street expects earnings of 42 cents per share. Hormel hasn’t, as of yet, changed its full-year guidance.

Hormel is a classic recession-resistant company. The stock is holding up well against the market this year (see below). Remember that Hormel is a lot more than Spam. The company owns several strong brands.

Ross Stores (ROST) is also due to report next Thursday after the closing bell. We’ve come to expect Ross’s strategy of low-balling guidance and then delivering better-than-expected results.

In March, Ross reported fiscal Q4 earnings of $1.28 per share. That was above the company’s guidance range of $1.20 to $1.25 per share.

For any retailer, the key stat to watch is same-store sales. For Ross, that figure rose by 4% last quarter. Ross has been expecting same-store sales growth of 1% to 2%. For all of 2019, Ross made $4.60 per share. That’s up from $4.26 in 2018. Annual sales rose 7% to $16.0 billion.

Operating margin, another key for a company like Ross, came in at 13.3% for Q4. I know that may sound low, but for Ross’s business, it’s quite good. In March, Ross raised its quarterly dividend by 12% to 28.5 cents per share. Ross has raised its dividend every year since 1994.

The company shut all of its stores on March 20. It also furloughed most of its employees, although there was no change to their health benefits. Barbara Rentler, the CEO, has decided to forgo any salary. The Chairman of the Board did the same.

Ross’s Q1 guidance had been for $1.16 to $1.21 per share. On March 19, they withdrew that. Honestly, I’m not terribly concerned about Ross’s result because it will show an operating loss. No one can make a profit when all their stores are shut. Still, I’m very confident that Ross will do well once the economy reopens.

That’s all for now. There will be no issue next week. I’m taking off for Memorial Day. There’s not much on tap for economic news next week. The housing-starts report comes out on Tuesday. Of course, we’ll get another jobless-claims report on Thursday. The existing-home sales report is also on Thursday. The stock market will be closed on Monday, May 25 for Memorial Day. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on May 15th, 2020 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His