CWS Market Review – November 20, 2020

”One of the funny things about the stock market is that every time one person buys, another sells, and both think they are astute.” – William Feather

The stock market raced to a new all-time high last week on the news of Pfizer’s encouraging results for a Covid vaccine. The good news continued into this week with a similar announcement from Moderna. Their results were even better. The S&P 500 closed Monday at a new all-time high. Both the index and our Buy List are now up by double digits this year. (Who would have predicted that just eight months ago?!)

There are, however, some worrying signs. Coronavirus cases are surging, and the labor market may be a bit shaky. Also, Uncle Sam’s enormous stimulus may soon be coming to an end, and there are no plans, as of yet, to extend it.

In this week’s issue, I first want to focus on some recent economic news. We also had some very good news from our Buy List stocks. AFLAC hiked its dividend by 18%. This is the 38th year in a row that the duck stock has sweetened its dividend.

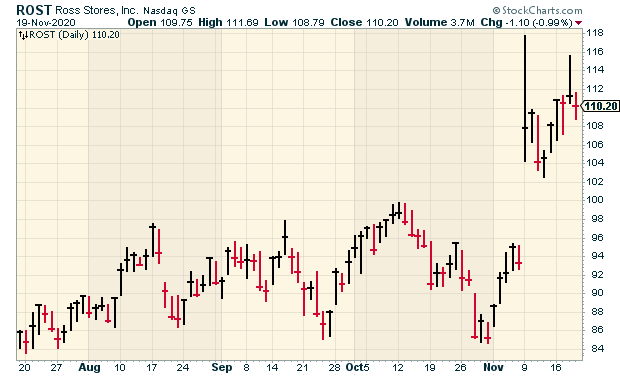

We also got very nice earnings news from Ross Stores. The deep-discounter is doing a commendable job of staying profitable in a very tough environment. I was glad to see Fiserv’s board approve a 60-million-share buyback. That’s a nice wad of cash they’re spending! I’ll have more to say on those stocks in just a bit. But first, let’s see how the economy is faring.

Coronavirus Cases Are Surging

Thursday’s jobless-claims report came in at 742,000. That’s weaker than I had been expecting, and I wasn’t alone. It was above Wall Street’s forecast as well. This could be a minor bump in a long-term downward trend. However, I am concerned about the possibility of cracks reappearing in the U.S. economy.

While the Covid vaccine news is promising, the surging numbers of new cases are alarming. As a result, more areas are falling under new lockdown orders. It appears that Thanksgiving will be a very scaled-down event this year.

These lockdowns are very unequal. While the stock market had an unpleasant few weeks in February and March, we bounced back. My fear is that a renewed lockdown will cause most harm to people who were already hurting. The most recent retail-sales report showed the slowest growth since May. As a friend said to me recently, “You can’t install drywall over Zoom.”

This week, Fed Chairman Jerome Powell said, “The concern is that people will lose confidence in efforts to control the pandemic, and…we’re seeing signs of that already.” The news may be getting worse. On Thursday, Treasury Secretary Steven Mnuchin said he would not extend the Fed’s emergency-lending programs. The programs are due to expire at the end of the year. In a very rare event, the Fed criticized the move. I honestly can’t remember the last time the Fed publicly criticized the Treasury Department.

The move is even more surprising given that Powell recently said that the Fed is committed to using these programs as long as they’re needed. He showed no indication that the time was ripe to wind down these efforts. In fact, most of the money the Treasury allocated to the Fed hasn’t yet been committed to any specific program. Another stimulus bill is on its way, although the details and timetable are uncertain.

The bond market has rebounded over the past week, which could be another sign that Wall Street sees slower growth ahead. This also boosts the theme I’ve covered the past few weeks: namely, value stocks outperforming growth stocks. Whenever the economy catches a cold, higher-quality and more stable stocks typically outperform. If you recall, our Buy List got hammered in February and March, but not as much as the overall market.

Make sure your portfolio has a healthy allocation of high-quality stocks, and pay special attention to those with good dividends. That will help protect you when the storms come. Now let’s look at this week’s earnings report from Ross Stores.

Ross Stores Beats the Street

On Thursday, Ross Stores (ROST) reported very impressive earnings for its fiscal third quarter. Or more accurately, Ross reported impressive earnings, all things considered.

The reason I said that is because this has been a very difficult environment for the deep-discounter, and they’ve managed themselves very well. For the 13 weeks ending November 2, Ross Stores earned 37 cents per share, but that includes a charge of 65 cents per share due to a major debt refinancing. Add that back in, and it works out to a quarterly profit of $1.02 per share. Wall Street had been expecting earnings of just 61 cents per share. Ross earned $1.03 per share for last year’s Q3. Sales for the quarter fell by 2% to $3.8 billion, and comparable-store sales were down 3%.

CEO Barbara Rentler said, “Sales trends accelerated during the third quarter following a slower start in August, driven by an improvement in our merchandise assortments, a later back-to-school season, stronger performance in our larger markets, and our return to more normal store hours.”

She also noted that “Core-business results improved during the quarter, demonstrating consumers’ continued focus on value, and our ongoing ability to deliver the bargains our customers have come to expect from us.”

Ross continues to have a strong financial position, with over $5.2 billion in total liquidity. The company also repaid its $800 million revolving-credit facility. That will significantly cut down on interest costs.

What about the current quarter, which includes the big holiday shopping season? Unfortunately, the outlook is very uncertain. So far, sales are down in November. The big concern is how Ross will be impacted by a new wave of lockdowns. Ross has wisely decided not to provide any sales or earnings guidance for Q3.

The good news is that this was a solid quarter for Ross. As long as the company is allowed to make a profit, it will. I’m lifting my Buy Below on Ross Stores to $120 per share.

Earnings Preview for Hormel Foods

Hormel Foods (HRL) is due to report its fiscal Q4 earnings before the market opens on Tuesday, November 24. This will be for the three months ending on October 31.

Hormel had a decent quarter for Q3. The Spam people earned 37 cents per share, which beat the Street by three cents per share. Overall sales rose 4% to $2.4 billion. Sales volume also rose by 4%. That’s important, because you don’t want to rely overly on price increases. Hormel’s operating free-cash flow rose 72% to $242 million.

Hormel has four key operating segments: refrigerated foods, grocery products, Jennie-O Turkey and international. For Q3, the grocery products had a great quarter, while the turkey biz was weak.

Hormel has a solid balance sheet. Its cash on hand is now $1.7 billion. That’s due to a bond offering, and also halting share buybacks. Total debt is up to $1.3 billion from $0.3 billion a year ago.

Hormel expects to see Q4 mirror the strength of Q3. Hormel’s CEO said he expects the food service to post a year-over-year decrease for Q4. The consensus on Wall Street is for earnings of 44 cents per share. That’s down from the 47 cents per share HRL made in last year’s Q4.

Buy List Updates

Fiserv (FISV) has had a tough year in 2020. The company delivered good news this week in the form of a massive stock buyback. Fiserv’s authorized a 60-million-share buyback program.

It’s a huge block of shares. In dollar terms, that’s around $6.5 billion. Fiserv currently has 660 million shares outstanding. This week, I’m raising my Buy Below on Fiserv to $120 per share.

We also received good news this week from AFLAC (AFL). The duck stock raised its quarterly dividend from 28 cents to 33 cents per share. That’s a hefty increase. It adds up to a 17.9% increase.

What’s most impressive is that this is AFLAC’s 38th annual dividend increase in a row. That’s a remarkable streak.

Commenting on the announcement, AFLAC Incorporated Chairman and Chief Executive Officer Daniel P. Amos said: “I am pleased with the Board’s action to increase the first-quarter-2021 dividend. We treasure our record of 38 consecutive years of dividend increases, and we are looking to reward our shareholders by extending that track record in 2021. We remain committed to maintaining strong capital ratios on behalf of our policyholders and balance this financial strength with a focus on increasing the dividend, repurchasing shares and reinvesting in our business. Our dividend track record is supported by the strength of our capital and cash flows.”

The new dividend will be payable on March 1 to shareholders of record at the close of business on February 17. Based on Thursday’s closing price, the new dividend yields just over 3%.

I’m going to keep AFLAC’s Buy Below price at $44 per share, but our other financial stocks have been rallying quite well lately (it’s about time).

Globe Life (GL), for example, is up 15% for us this month. I’m lifting our Buy Below on GL to $100 per share. Our other financial stock that’s been soaring for us has been Eagle Bancorp (EGBN). The little bank has rallied nearly 50% in two months. This week, I’m raising our Buy Below on Eagle to $42 per share.

That’s all for now. There will be no newsletter next week. I’m taking my traditional Thanksgiving break. The U.S. stock market will be closed on Thursday for Thanksgiving, and it will close at 1 p.m. on Friday, November 27. There’s not much in the way of economic news scheduled for next week. On Wednesday, the jobless-claims report is due out. On that same day, we’ll also get a revision to Q3 GDP. The initial report said that the economy grew by 33.1% last quarter. Be sure to keep checking the blog for daily updates. I’ll have more market analysis for you in the next issue of CWS Market Review!

– Eddy

Posted by Eddy Elfenbein on November 20th, 2020 at 7:08 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His