CWS Market Review – June 15, 2021

(This is the free version of CWS Market Review. Don’t forget to sign up for the premium newsletter for $20 per month or $200 for the whole year. The premium version contains more detailed analysis and I cover our Buy List stocks in greater depth. Join us today!)

The stock market closed at another all-time high yesterday. That was its third record close in a row, although the S&P 500 closed a bit lower today. The stock market has now gone 17 days in a row trading in less than a 1% daily range.

For now, Wall Street is focused on this week’s Fed meeting. The policy statement will come out tomorrow afternoon. The central bank is nearing an important juncture. The Fed went to extraordinary lengths during the pandemic to help the U.S. economy.

Now that the economy is getting better, the Fed needs to unwind these efforts. We know that’s coming, but we don’t know when and how just yet. The Fed already said it’s going to pare back its holding of corporate bonds.

To be fair, that’s a minor item for the Fed. The big issue is the Fed’s massive buying of Treasury and mortgage bonds. Sometime soon, in all likelihood, the Fed will announce that it will gradually taper its bond purchases. However, the Fed doesn’t want a repeat of the infamous Taper Tantrum of 2013. That’s when the bond market went into a hissy fit at the mere mention of less support from the Fed.

In a Congressional hearing in May 2013, Ben Bernanke said that if the economy continued to improve, then Fed would gradually pull back on its quantitative easing. The bond market freaked out and yields soared. Bernanke quickly walked back his comments. (The bond market isn’t happy unless it’s upset.)

In late August, the Kansas City Fed will host its annual shindig in Jackson Hole, WY. My guess is that that’s when the Fed will address the issue of any sort of tapering. The Fed has been buying $120 billion in bonds every month, so I expect that any tapering will leave a big footprint.

Fortunately, I don’t expect any tapering to have a big impact on our Buy List stocks. For one, the tapering is widely expected. Also, our stocks are in much better shape than other companies so they did not need the support like others did.

Highest Producer Inflation on Record

The market and inflation news appear to be moving in opposite directions. The news, which is lagging, continues to show evidence of higher inflation. The bond market, which looks ahead, appears to be chilling out in its view of inflation.

Remember all those stories about the soaring price of lumber. Well, lumber is down 40% since May. Corn is also down as is copper. We’ll also seeing a break in home prices.

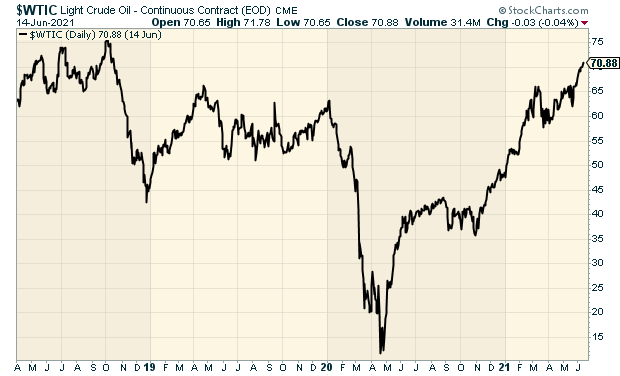

But it’s a mixed market. Today, for example, oil prices got to their highest level since 2018. This story ain’t so complicated. That’s the natural outcome of greater demand and lower supplies. But that’s not the only inflation warning we got today.

This morning, the Labor Department said that producer prices (PPI) rose 0.8% in May. That’s a big increase and it easily beat Wall Street’s forecast of 0.5%. Typically, inflation shows up at the producer level first before it works its way down to consumers.

Over the last year, producer prices are up by 6.6%. That’s the largest year-over-year increase since they started collecting the data in 2010. It’s not just food and energy. The “core” PPI is up by 5.3% over the past year. That’s the highest since they started tracking that data in 2014. Still, the bond market has been pretty chill. The 10-year yield is currently around 1.5%. Just a few weeks ago, it was close to 1.7%.

We also had the retail sales report come out this morning. For May, retail sales fell by 1.3%, but the details are more complicated. What’s really happened is that consumers have been shifting their spending to services which aren’t included in retail sales.

This made for an unusual retail sales report. For example, online sales fell as more folks wanted to go shopping in person. That’s certainly understandable. Spending at restaurants and bars rose 1.8% last month. Spending at casinos rose nearly 17% and theme parks were up 9%. Gyms saw an increase of 4%. These numbers compare May to April, but if we compare last month’s numbers with May 2020, then retail sales were up 28%. Clearly, people want to go out after being cooped up for so long. That ties into the demand for more labor.

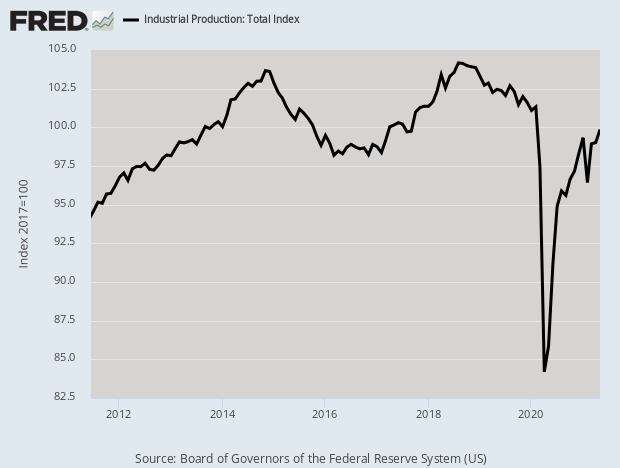

Also this morning, the Federal Reserve said that industrial production rose by 0.8% in May. That’s a good number. Production of autos rose by 6.7%. I often hear people say that America “doesn’t make anything anymore.” That’s not true. America is a manufacturing superpower. The difference is that a lot fewer people do it.

The plunge and recovery in industrial production is something to behold:

List of Meme Stocks

A number of readers have asked about “meme” stocks. Obviously, I’m not a big fan of that type of investing, which is really gambling. I’ll give you a good example. Shares of Koss are up roughly 20 times their 52-week low. The shares are also off about 80% from their 52-week high.

There isn’t a precise definition of what makes up a meme stock, but here’s a list of 12 names that are often included in the meme universe.

AMC Entertainment (AMC)

Bed Bath & Beyond (BBBY)

BlackBerry (BB)

Clean Energy Fuels (CLNE)

Express (EXPR)

GameStop (GME)

Koss (KOSS)

Rocket Companies (RKT)

Sundial Growers (SNDL)

Tilray (TLRY)

Wendy’s (WEN)

Workhorse Group (WKHS)

Stock Focus: Waters Corporation

Now, for a much better stock. A company that’s been a finalist for our Buy List a few times but never a member is Waters Corporation (WAT). I like this company a lot. Even though it’s not well-known to investors, Waters is one of the world’s leading specialty measurement companies. Waters is focused on improving human health and well-being through the application of high-value analytical technologies.

The company was founded in 1958 by James Waters. He passed away a few weeks ago at the age of 95. Waters got his big break in 1972 when he solved a complicated problem for Robert Woodward, a Nobel Prize-winning chemist at Harvard. Waters went to Woodward’s lab with a liquid chromatograph and helped solve the problem within a few weeks.

Waters is headquartered in Milford, Massachusetts. After 73 years, it’s become a pretty big outfit. The company currently has over 40,000 customers and a workforce of 7,400 employees. Waters went public in 1995 and the shares are up 90-fold since then. This year, Waters is on track to register $2.7 billion in revenue. The current market cap is $21 billion. Waters is also a member of the S&P 500.

So what do they do? The company makes, sells and services high-performance liquid chromatographs, ultra-performance liquid chromatographs and mass spectrometers. Waters operates through two segments, Waters and TA (for thermal analyzers).

If you’re like me, then you probably rarely find yourself in the market for a spectrometer. Or maybe never. But there are lots of businesses who love them and buy them. But what do these things do? Spectrometers help identify chemical compounds. This is important for drug development, food testing, and air and water quality testing. Waters also designs and sells thermal analysis, rheometry and calorimetry instruments through its TA product line.

This is normally a very good business to be in. Waters has a high “moat” which means it’s well-protected from competitors. That’s the kind of company I like to buy. Waters often delivers operating profit margins near 30%. That’s quite good.

Unfortunately, Waters had a difficult year last year and also in 2019. I’ll give you an example. For Q1 2020, Waters reported earnings of $1.15. That was 32 cents below estimates. Wall Street was not pleased. During the pandemic bear market, the stock lost nearly 40% in a few weeks. Lately, however, business has greatly improved. Last month, Waters reported Q2 earnings of $2.29 per share. That beat estimates by 72 cents per share. Earlier today, the shares hit a new all-time high. From its 2020 low, Waters has gained more than 135%.

Check out its long-term performance:

Focusing in on the Q1 earnings report, I was glad to see that recurring revenue increased by 20%. Instrument systems sales were up by 49% and the pharmaceuticals market was up 32%. The sales results from Asia were also very good.

Waters’s President and CEO Dr. Udit Batra said, “There is much to be pleased about with our first quarter results, driven by strong growth across each of our major end markets, with pharma leading the way. Thanks to solid execution and instrument sales growing in double-digits, we saw revenue increases across every region, with China’s sales more than doubling. Our transformation plan is well underway, with commercial momentum and a strong leadership team in place, we now turn towards developing a new strategy as we work to more closely align our portfolio with higher growth areas of the market.”

What to expect for the rest of this year? Waters expects to see full-year sales growth of 8% to 11%. For earnings, Waters sees earnings ranging between $9.85 and $10.05 per share. That’s optimistic, but certainly doable.

For Q3, Waters expects sales growth of 14% to 16%. For earnings, Waters forecasts a range of $2.15 to $2.25 per share. Wall Street had been expecting $2.11 per share.

As much as I like this company, the stock is way too high. The shares are going for roughly 34 times this year’s earnings. However, if we were to see a 20% or so pullback, then I’d be very interested in Waters Corporation.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. Don’t forget to sign up for our premium newsletter.

Posted by Eddy Elfenbein on June 15th, 2021 at 5:32 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His