CWS Market Review – December 28, 2021

(This is the free version of CWS Market Review. In our premium issue, I’ve recently unveiled our Buy List for 2022. To see the new list, make sure you’re a premium subscriber. You can get the premium newsletter for $20 per month or $200 for the whole year.)

The Honey Badger Market

This continues to be the Honey Badger Market. It just doesn’t care. The stock market seems to effortlessly brush aside every problem standing in its way.

Highest inflation in 40 years? No problem.

Supply-chain issues? Move over.

Omicron? Please.

Higher and higher the market goes. Since October 4, the stock market has gained more than 11%. This looks to be one of the strongest quarters for the stock market in years.

Earlier today, the S&P 500 broke through 4,800. Although we closed down by a small bit today, the index is getting close to doubling from its March 2020 low. Who would have predicted that?!

Yesterday, the S&P 500 closed at its 69th record high this year. That’s nearly a record high for record highs. Only 1995 had more.

Not only that, but the Santa Claus Rally is off to its best start in 20 years.

There are lots of definitions for what the Santa Claus Rally entails, but if we say it’s the last week of December and the first two trading days of the new year, then the rally got off to a big start this year.

On Monday, the S&P 500 gained 1.4%. That’s the biggest start to the season in two decades. Every time the Santa Claus Rally has started with a gain of 1% or more, the whole period has been a positive one for the market.

By the way, the S&P 500 first broke 480 on January 31, 1994, nearly 28 years ago. That means that despite all the sturm und drang of the last 28 years, the stock market still rose tenfold, which comes to more than 8.5% per year—and that doesn’t include dividends.

Despite being the final week of trading for this year, this is a slow week for financial news. That will change next week with the December jobs report due out on January 7. There’s a decent chance that the unemployment rate will fall below 4%.

Soon after that, the Q4 earnings season will begin. That’s Judgment Day for Wall Street. Let’s take a closer look at what we can expect.

Preview of the Q4 Earnings Season

What’s the reason for the market’s bullishness? It’s not always so easy to divine the market’s thinking from its behavior. As we know, the market likes to be a bit of a drama queen. Still, I suspect that Wall Street is starting to feel that the upcoming Q4 earnings season will be a good one. After all, Q3 was pretty good.

Also, expectations for Q4 have improved markedly. That’s counter to the usual playbook. Typically, earnings estimates start out too high and are gradually pared back as earnings season approaches. They’re lowered just enough so Wall Street can beat expectations.

Ironically, it’s expected that your company beat expectations. If you merely meet expectations, well…no one saw that coming and your stock can get clobbered. The stock market is all about exceeding expectations.

Let’s look at some numbers. In early 2020, before Covid wrecked the economy, Wall Street had been expecting very good earnings for Q4 of 2021. Of course, it’s always a little sketchy to predict something that far in advance.

For Q4 2021, Wall Street was expecting the S&P 500 to report Q4 earnings of $49 per share. That’s the index-adjusted number (every one point is about $8.5 billion). As Covid set in, the number crunchers on Wall Street lowered their forecasts.

By the start of this year, Wall Street was expecting Q4 earnings of just $44 per share.

Since then, the news has been much better. It’s the twin effects of very diminished expectations and actually good earnings. The S&P 500 earned over $52 per share for both Q2 and Q3. That compares with less than $20 per share in Q1 of 2020. That was a scary time.

According to the latest figures, Wall Street now expects the S&P 500 to earn $50.45 per share for Q4 of 2021. If that’s right, that would be a remarkable turnaround in just a few months. Now you can see what has the stock market so excited. It’s not just fluff. Corporate earnings have improved by an impressive degree.

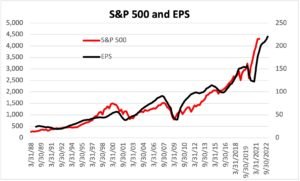

Here’s a look at the S&P 500 (red line, left scale) and its earnings (black line, right scale. The two lines are scaled and a ratio of 20 to 1. That means whenever the lines cross, the market’s P/E ratio is exactly 20.

Assuming Wall Street’s Q4 estimate is correct (and it’s probably pretty close), then the S&P 500 will have earned $202 per share for this year. For 2022, Wall Street forecasts earnings of $220 per share. That means the S&P 500 is going for 21.7 times earnings. The earnings yield, which is the inverse of the P/E Ratio, is 4.6%.

While that’s certainly low, it’s not out of line when you compare it with the 10-year Treasury which is currently yielding around 1.5%. In other words, the stock market has run up a lot, but there’s been good reason for it. I wouldn’t be so quick to call this a speculative bubble. It’s probably closer to saying that the fear bubble from last year has popped.

Here’s a brief aside. Look at this headline from CNBC:

How would you interpret the news? I would assume that it means that home prices rose 18.4% for the month of October. Right? But that’s not what happened.

Instead, home prices rose 18.4% in the 12 months ending in October. Maybe I’m being pedantic, but that’s quite a big difference between headline and payoff.

Closer Look at Trex

Jack Bogle once said that “reversion to the mean is the iron rule of financial markets.” One exception to that may be Trex (TREX). We added it to our Buy List last year and it was our top-performing stock. During 2020, shares of Trex gained more than 86%.

Instead of reverting to the mean, Trex is having another stellar year, and it looks to repeat as our top-performing stock with a YTD gain of 61%.

If you’re not familiar with Trex, the company is a major maker of wood-alternative decking and railing. In my opinion, what they make looks a lot like wood, but it’s cheaper and involves a lot less maintenance.

Trex is also better for the environment. Pressure-treated wood still dominates which means there’s plenty of room for Trex to grow. It’s also nice to know that with Trex, you don’t have to take another tree out of the Amazon rainforest to make your backyard deck.

Check out their products at their homepage (www.trex.com), and you’ll see why Trex has become so popular.

One of the reasons why I like Trex is their commitment to sustainability. Trex is made from 95% recycled material. Every year, the company effectively takes 500 tons of plastic out of landfills and uses it for alternative wood. It’s not just good for the planet, but it’s smart business.

Trex takes all those used bags and bottles and combines them with recycled sawdust from cabinet and furniture manufacturers – and that’s what Trex is made of. By the way, this also saves a lot of water.

Some other key advantages are that Trex weighs less than wood and is also more resistant to mold and insects. You don’t need expensive staining or sanding, and repairs are much less frequent.

You’ll often hear people say that Trex looks fake. I think that used to be true, but it’s much less the case today. Commercial railing is another big business for Trex. Their railings are especially common at stadiums and arenas across North America.

Trex is sold in 40 different countries and at over 6,700 retailers. The company IPO’d 20 years ago, and it’s been a big winner for shareholders. I don’t think we’re anywhere near the end of this story.

Now let’s look at some numbers. Trex will probably do about $1.2 billion in business for 2021. I think that can rise to $1.4 billion, give or take, in 2022.

For earnings, last year Trex made $1.55 per share. When the final numbers are in for 2021, Trex will have probably made about $2.10 per share. But for 2022, I think Trex can make as much as $2.60 per share. That’s an optimistic forecast, but it’s possible.

Last month, Trex reported Q3 earnings of 64 cents per share. That was six cents higher than expectations and 73% higher than a year ago. Quarterly sales rose 45% to $336 million.

I’ve been impressed by the way Trex is managing itself. On one hand, the company faces higher prices for raw materials and higher labor costs. Trex was able to expand its gross margins by 150 basis points last quarter. Some of these comparisons are distorted because last year was so unusual. The important fact is that Trex has been able to pass along higher prices without damaging sales. There will be more price increases in 2022.

Here’s an interesting stat. On the earnings call, management said that composites have been gaining market share at the rate of 1% each year. Now that’s accelerated to 2%.

Trex said it sees Q4 revenue of $295 million to $305 million. The midpoint is up 31% from last year’s Q4. The company also expects “strong double-digit revenue gains” next year. Trex plans to open a new manufacturing facility on 300 acres in Little Rock, Arkansas.

I like that Trex can maintain an operating profit margin near 25%. That’s very impressive. Also, Trex has a solid balance sheet and doesn’t carry a dime in long-term debt. The price isn’t dirt cheap but there’s a lot of potential for Trex.

That’s all for now. I want to wish everyone a happy and healthy New Year. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. Don’t forget to check out our ETF.

Posted by Eddy Elfenbein on December 28th, 2021 at 7:49 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His