CWS Market Review – June 14, 2022

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

It’s Official. We’re in a Bear Market

Yesterday was a terrible day for Wall Street. The stock market plunged, and it looks like the battle to defeat inflation will be a lot more difficult than many folks had originally anticipated.

On Monday, the S&P 500 lost 3.88% which made it the index’s second-worst day of the last two years. If you’re really into market history, it was the 161st worst day since 1928. In the entire S&P 500 on Monday, only five stocks closed higher.

More importantly, the S&P 500 closed below the 20% drawdown line which is the traditional definition of a bear market. At today’s market close, the S&P 500 is down 22.12% from its all-time high close reached on January 3 of this year.

Today was the lowest close for the stock market in more than 17 months. At one point, the stock market was up 26% during the Biden presidency. Now that’s all gone.

What driving the selling? The answer is easy. It’s the same thing that’s been happening, only more so. Inflation has spooked Wall Street and traders now believe the Federal Reserve needs to keep raising interest rates. To give you an example, since Friday, the yield on the two-year Treasury jumped from 2.83% to 3.45%. The two-year is often seen as a proxy for the market’s opinion for where rates ought to be. The two-year yield is now at a 15-year high.

Again, what we’re seeing is risky stocks getting slammed while more conservative stocks are down but not by nearly as much. On Monday, the S&P 500 Low Volatility Index fell by 2.97% while the S&P 500 High Beta Index dropped by 6.54%. The tech-heavy Nasdaq Composite is now down by one-third since November.

What’s really happening is that many stocks are giving back gains they never should have had in the first place. To give you an example, shares of Moderna (MRNA) are now trading at one-quarter of their value in August. Shares of Zoom (ZM) are down more than 80% from their high. Netflix (NFLX) is off by 70% just this year, and we’re not even at July 4!

Everything seemed so easy before that meddling inflation showed up! The bull market that recently ended was one of the fastest on record, and it was the quickest ever to double. Now the bill has come due.

Over four trading days (Wednesday to Monday), the losses got progressively worse. On Wednesday, the S&P 500 lost 1.1%. Then on Thursday, it fell 2.4% followed by another 2.9% on Friday. Today was the market’s best day of the last week, and that’s still a loss of 0.38%.

I’m pleased to say that our conservative-oriented Buy List keeps chugging along. Since June 1, the S&P 500 is down by 8.92% while our Buy List is off by “just” 7.30%. I know it sounds odd to point out that we’re down but by less, but that’s where a lot of long-term outperformance comes from. Our stocks are generally much higher quality and that protects them during a storm like this. I’ve used this quote before, but it’s a good one from Shelby Cullom Davis: “You make most of your money in a bear market; you just don’t realize it at the time.”

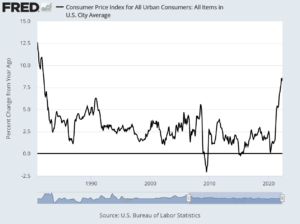

Worst Inflation Since 1981

What spurred the bad news on Friday was another troubling inflation report. There had been some hope that we might see some evidence that inflation had cooled off during May. Well, that didn’t happen. The government said that consumer prices rose by 8.6% in the 12 months ending in May. That’s the highest inflation rate since December 1981.

Digging into the details, the picture is not encouraging. Instead of cooling off, it seems that inflation is getting worse. The monthly rate of inflation increased from 0.3% in April to 1.0% in May. That’s the second-highest monthly rate of the last 10 years.

At that rate of inflation, if you’re paid in dollars at a fixed rate for one year, that means you effectively work one month of the year for free, and that doesn’t include taxes. Inflation is also taking its toll on wages. Last month, inflation-adjusted wages fell by 0.6%.

It’s true that food and energy have been driving much of the inflation, but the core rate also remains stubbornly high. For the 12 months ending in May, the core rate of inflation increased by 6.0% which was higher than expectations. For the month, the core rate increased by 0.6%. To give you an idea of how much things have changed, the core rate of inflation for the 12 months ending in February 2021 was just 1.3%.

Look for the Fed to Hike by 0.75%

The Federal Reserve is meeting again in Washington. The policy statement is due out tomorrow at 2 p.m. Yesterday afternoon, the stock market got another shock when the Wall Street Journal reported that the Fed was considering raising interest rates by 0.75%. I should explain that when the Wall Street Journal reports that the Fed is considering something, you can be pretty sure this is coming from the top.

A string of troubling inflation reports in recent days is likely to lead Federal Reserve officials to consider surprising markets with a larger-than-expected 0.75-percentage-point interest-rate increase at their meeting this week.

Before officials began their premeeting quiet period on June 4, they had signaled they were prepared to raise interest rates by a half percentage point this week and again at their meeting in July. But they also had said their outlook depended on the economy evolving as they expected. Last week’s inflation report from the Labor Department showed a bigger jump in prices in May than officials had anticipated.

The Fed was also shocked by two recent reports showing that consumers are starting to expect higher inflation. This is why inflation is so difficult to fight. It becomes a self-fulfilling prophecy. Once consumers expect it, they get it.

Before the WSJ scoop, investors had been expecting an increase of 0.5%. In fact, the Fed basically said so. In May, Fed Chairman Jerome Powell said that the Fed was not “actively considering” larger increases. Apparently, that’s all changed. One week ago, the futures market pegged the odds of a 0.75% rate hike at 4%. Now it’s at 94% and a slew of major Wall Street investment houses say they expect to see a 0.75% hike tomorrow. The Fed hasn’t done a 0.75% hike since 1994.

I’m glad to see the Fed finally realize the problem is more acute than they had initially believed. The problem is that the Fed’s main tool is short-term interest rates. That’s a very blunt tool. The Fed thinks it can enact precise fine-tuning with rate hikes. They think they’re using scissors when they’re really using an axe.

I think there’s a very good chance that we’ll see another 0.75% at the Fed’s next meeting in July. That would bring the Fed’s target range to 2.25% to 2.5%. How high will the Fed go? That’s a good question. The place to look is long-term rates. I would guess that the Fed wants to make the yield curve flat, even a little negative. With the 30-year yield at 3.45%, that means the Fed could go as high as 4% within the next six to nine months.

The larger story remains the same. The Fed overreacted to Covid by lowering rates to the floor. That radically changed the math on Wall Street as high-risk stocks became no-brainers. There was a big bull market in everything risk. Not just riskier stocks, but also crypto and NFTs. Higher rates are tripping up all those high-risk, high-volatility sectors. In less than two months, the price for bitcoin has been cut in half. Bitcoin is now down 69% from its peak. Remarkably, this is only its seventh-steepest correction in the last 12 years.

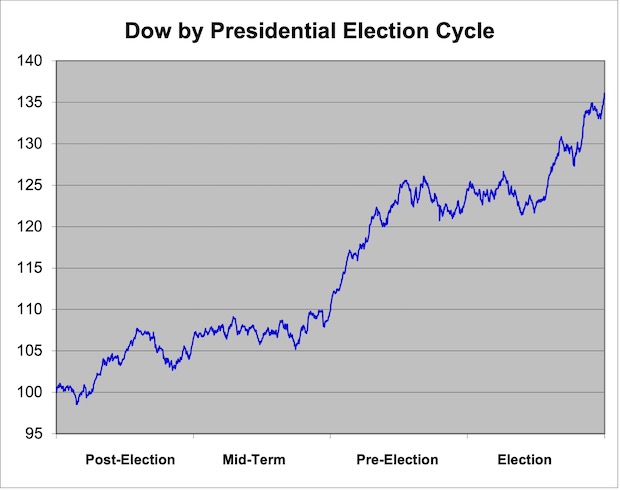

The Low in the Presidential Election Cycle

I’m not much of a fan of historical patterns in the stock market, but I’ll highlight one for you today. The stock market has traditionally reached a low point during midterm years in the presidential election cycle. As it turns out, this is one such year and the midterm elections are less than five months away.

I’ve crunched over 130 years of data on the Dow Jones Industrial Average and found that the low point of the presidential cycle comes on September 30 of the midterm year. Historically, the 15 months prior to September 30 of the midterm have been pretty blah for stocks.

However, after September 30, the stock market has done quite well. From September 30 of the midterm year until July 22 of the pre-election year, the Dow has gained an average of 19.3%. That’s more than half of the market’s entire gain coming in less than 11 months.

Here’s what the average presidential election cycle has looked like:

That’s the average of 125 years of the Dow. I set the chart to start at 100 on January 1 of the post-election year.

My point is not about timing the market. Rather, it’s that there tend to be broad cycles in the stock market. Though we’re in a painful bear market, this too shall pass. In fact, we’re seeing excellent bargains right now.

Last week, we had a very strong earnings report from Science Applications International (SAIC) which is our #2 performing Buy List stock this year. The company beat earnings and raised guidance.

That’s all for now. The stock market will be closed this Monday in honor of Juneteenth. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. Don’t forget to sign up for a premium subscription: $20 per month or $200 for the whole year!

Posted by Eddy Elfenbein on June 14th, 2022 at 7:37 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His