CWS Market Review – February 6, 2024

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

You Can Forget About That March Rate Cut

Well, maybe the Fed won’t be raising interest rates next month!

Over the last few days, we’ve gotten some important news that’s completely shifted our expectations for what the Fed’s plans are. It looks like the Federal Reserve probably will not be cutting interest rates at its March meeting. This new outlook is having a major impact on Wall Street. In two days, the yield on the three-year Treasury rose from 3.96% to 4.27%.

This change in outlook has impacted the stock market as well. On Friday, the S&P 500 closed at a new all-time high, but it was a very narrow market. By that, I mean that most of the heavy lifting was being done by a few stocks. Facebook, for example, gained more than 20%. Even though the S&P 500 rallied more than 1% on Friday, the average stock in the index was down for the day.

J.C. Parets noted that on Monday, we saw the fewest stocks on the NYSE above their 200-day moving average since early December, and the fewest above their 50-day moving average since mid-November.

The stock market finished just shy of a new all-time close today.

This is a confusing and temperamental market. Let’s breakdown what’s going on. We’ll start with last week’s jobs report.

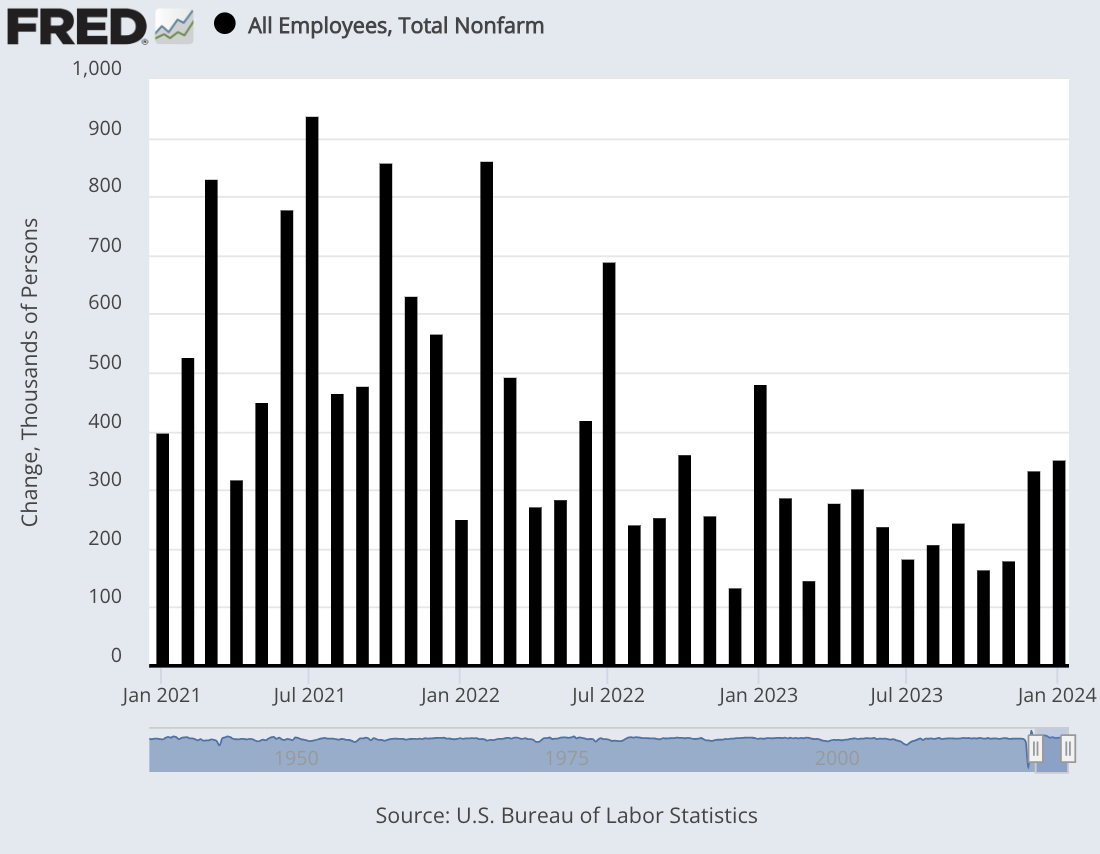

Wall Street got a big shock on Friday when the January jobs report came in much better than expectations. Wall Street had been expecting a gain of 185,000 net new jobs. That wasn’t even close. Instead, the Labor Department said that the U.S. economy added 353,000 new jobs last month.

Who would have guessed that an aggressive interest rate policy from the Fed seems to have had little impact on the labor market? Not me.

Wall Street had been expecting the unemployment rate to rise to 3.8%. Instead, it stayed at 3.7%. If you work out all the decimals, then the current unemployment rate is lower than it was during every single month in the 1970s, 80s, 90s and 00s. All the way through 2018. (To be fair, the methodology hasn’t remained consistent over that time.)

We’re also seeing a pickup in wages. In January, average hourly earnings grew by 0.6%. That doubled Wall Street’s forecast. Over the last year, wages are up by 4.5%. The problem is that any previous wage growth had largely been eaten up by inflation. That’s not so much the case anymore.

Not only was January a good month for job growth, but the Labor Department also revised higher its numbers for November and December. The original estimate for December was for a jobs gain of 117,000. Now the Labor Department says it was 333,000. The number for November was revised upward by 9,000.

Here are some more details from the jobs report:

Job growth was widespread on the month, led by professional and business services with 74,000. Other significant contributors included health care (70,000), retail trade (45,000), government (36,000), social assistance (30,000) and manufacturing (23,000).

The broader U-6 rate increased to 7.2%. Also, the labor force participation rate stayed the same at 62.5%. If we look at the labor force participation rate for prime-working age folks (25 to 54), that rose to 83.3% which isn’t far from a 20-year high.

One interesting bit in the jobs report is that hours worked declined even though wage is holding up well. That may suggest that employers are opting to reduce hours instead of cutting jobs. It’s hard to say if this is a trend just yet, but it’s worth watching.

The jobs report came one day after the strong Q4 GDP report. That report said that the U.S. economy grew at a real annualized rate of 3.3% during the final three months of 2023. That’s quite good. The Atlanta Fed’s GDPNow model just raised its forecast for Q1 GDP growth from 3.0% to 4.2%.

With the economy growing and creating new jobs, why is the Fed in such a rush to raise interest rates? Well, it turns out that the Fed isn’t in a hurry to raise interest rates.

Fed Chairman Jerome Powell was interviewed on 60 Minutes. The interview aired on Sunday. In it, Powell said that although he’s pleased with the direction in inflation, he and the FOMC aren’t fully convinced that the battle is over.

PELLEY: You’ve avoided a recession. Why not cut the rates now?

POWELL: Well, we have a strong economy. Growth is going on at a solid pace. The labor market is strong: 3.7% unemployment. And inflation is coming down. With the economy strong like that, we feel like we can approach the question of when to begin to reduce interest rates carefully.

And, you know, we want to see more evidence that inflation is moving sustainably down to 2%. We have some confidence in that. Our confidence is rising. We just want some more confidence before we take that very important step of beginning to cut interest rates.

PELLEY: What is it you’re looking at?

POWELL: Basically, we want to see more good data. It’s not that the data aren’t good enough. It’s that there’s really six months of data. We just want to see more good data along those lines. It doesn’t need to be better than what we’ve seen, or even as good. It just needs to be good. And so, we do expect to see that. And that’s why almost every single person on the, on the Federal Open Market Committee believes that it will be appropriate for us to reduce interest rates this year.

I added the boldface. In short, Powell wants to see more good data, and the FOMC thinks rates need to be cut sometime this year.

In the trading pits, Wall Street traders think there’s only a 20% chance that the Fed will cut at its next meeting. That’s a big change in a short amount of time. Just one month ago, the odds of a March cut were at 64%.

The odds of a cut in May were at 95%. Now they’re at 67%.

We’re still in the thick of Q4 earnings season. Frankly, the results haven’t been that great. The first batch of earnings were weak, but the numbers have gotten a bit better.

According to the most recent numbers, 46% of the stocks in the S&P 500 have reported results. Of that, 72% have beaten on earnings and 65% have beaten on revenue. That’s actually not that good. (On Wall Street-istan, you’re expected to beat expectations.) The five-year average is a 77% beat rate for earnings and a 68% beat rate for revenue.

The old Wall Street formula is to lower the expectations bar so low that you can easily step over it. Then declare victory.

Earnings are tracking growth of 1.6%. The average report is 2.6% above estimates. That’s below the five-year average of 8.5%.

Follow-Up on the WillScot/McGrath Deal

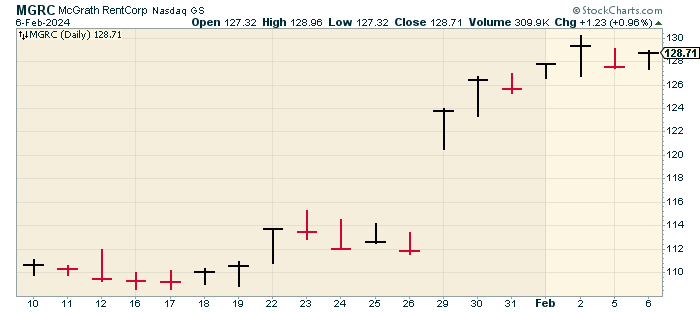

Last week, I told you about WillScot Mobile Mini Holdings (WSC) and its offer to buy out McGrath RentCorp (MGRC).

I bring it up again because the behavior of both stocks has been unusual. Normally, the acquirer’s stock falls, but not this time. Shares of WSC have rallied. Meanwhile, McGrath has rallied well above its cash buyout price.

Here’s how it’s supposed to work. The deal is 60% cash and 40% stock. McGrath shareholders have a choice. For each share of MGRC they own, they can either get $123 in cash or 2.8211 shares of WillScot Mobile Mini, but MGRC closed today at $128.71 per share. That’s well above the cash offer price. Meanwhile, WSC closed today at $50.13 per share. That values MGRC at $141.42 per share which is 10% above the current share price, and 15% above the cash price.

Normally, the buyout target wants the cash portion of the deal so they’re protected from a sudden plunge in the acquirer’s stock. This time, it seems that the cash side of the deal is an anchor. I won’t be surprised if the details of this deal are refined in the coming weeks. WillScot will report its Q4 earnings on February 20, and McGrath reports the next day.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

Posted by Eddy Elfenbein on February 6th, 2024 at 8:13 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His