CWS Market Review – April 9, 2024

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Maybe the Fed won’t be cutting rates!

It’s hard to say for certain, but on Wall Street, doubts have started to creep in about what the Fed will do with interest rates.

For months, Wall Street had assumed that the Federal Reserve would jump in and cut interest rates. The Fed admitted it as well. Lower interest rates, quite naturally, would help the stock and housing markets. The line of reasoning was simple: “Why not cut? Inflation’s fading away.”

Now it looks like the economy is stronger than expected, and inflationary indicators are running hot. The prices of gold and silver, for example, have rallied. The price for oil has also moved up. In fact, Mark Zandi, an influential economist with Moody’s, said that higher oil prices is the “most serious” threat to the economy. That’s not supposed to happen when inflation has been defeated.

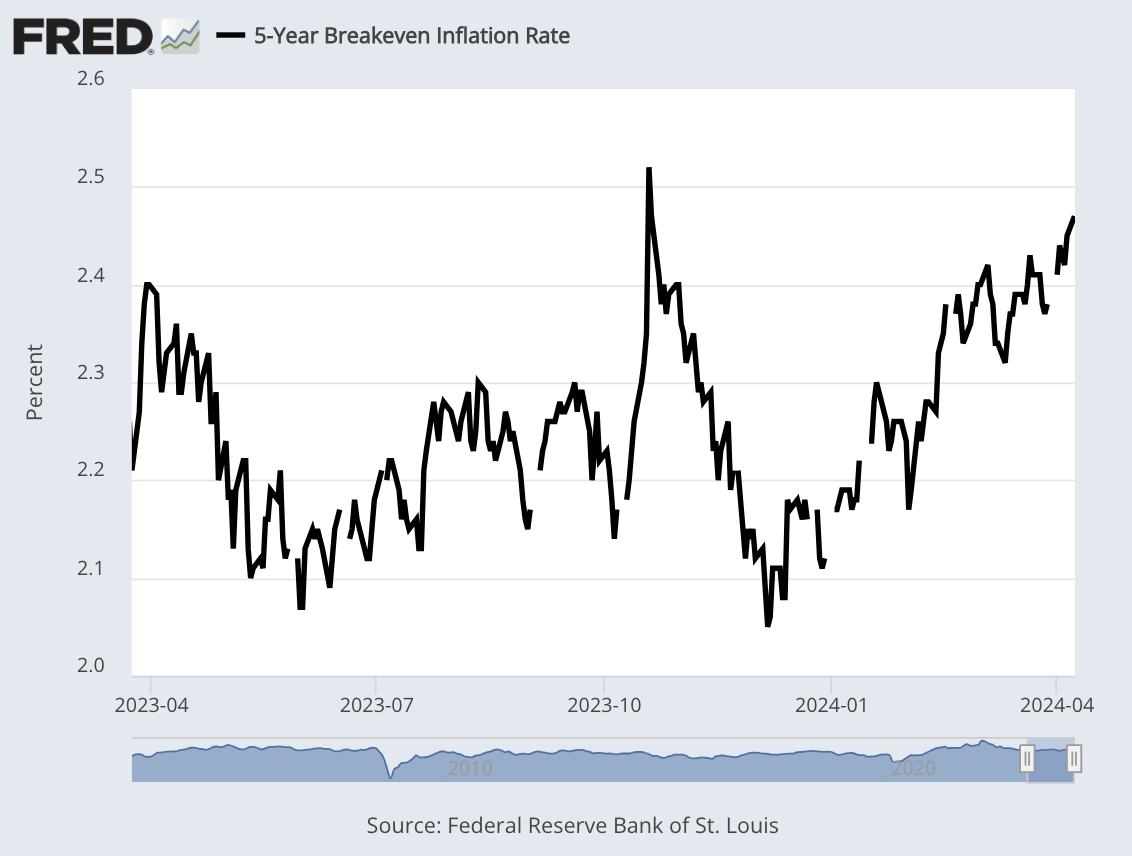

What’s the market thinking? Check out the five-year “breakeven rate:”

This is the market’s bet for what inflation will do over the coming five years. Notice how the breakeven rate has gone up since the start of this year. This is getting hard to ignore.

Now some Fed officials are hinting that rate cuts may not be as generous as assumed. Neel Kashkari, the head of the Minneapolis Fed, said the Fed could delay in cutting rates. Lorie Logan, the President of the Dallas Fed, said it might be too soon to cut rates. Not to be outdone, Jamie Dimon, the top banana at JPMorgan, said interest rates could eventually rise to 8%.

The problem for Wall Street is that so much of the recent rally was predicated on the idea of lower rates. It’s as if the stock market was told it got a bonus, and it quickly ran out and spent all the money before the bonus appeared in its bank account. Now it’s being told that the bonus may be canceled.

Even subtly, the stock market appears to be getting nervous. I’ve noticed that a few times recently, the stock market has been unable to hold onto early-day gains. Until recently, the bears were easily scared away. Now they’re able to push back and reverse morning rallies.

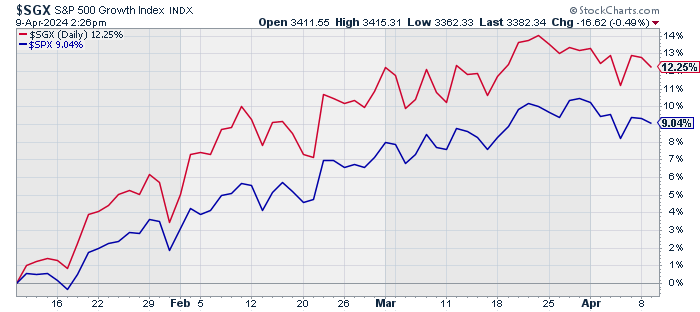

It’s interesting to note that growth stocks (in red) strongly led the market (blue) from the start of this year until two months ago. Since then, growth stocks have largely performed in line with the overall market, perhaps slightly trailing.

The Fed admitted that it sees itself cutting rates three times this year. Now, many traders think we’ll only get one or two cuts this year. There’s a growing number of people who think we won’t get any cuts this year.

The futures market currently thinks there’s a 60% chance that the Fed will cut rates by 0.25% in June and a 75% chance that it will come by July. Traders see only two rate cuts over the next seven months. That recession that was promised to us seems to be taking its time.

The Economy Created 303,000 New Jobs in March

Last Friday, the government reported that the U.S. economy created 303,000 net new jobs last month. That was an impressive number. Economists on Wall Street had been expecting a gain of only 200,000. Also, the unemployment rate ticked down 0.1% to 3.8%, and the labor force participation rate increased by 0.2% to 62.7%.

But there were some concerning stats in the report. For example, the jobs gain for February was revised lower to 270,000. Also, the broader U-6 rate was unchanged at 7.3%. The revision for January was an increase of 27,000 to 256,000, but that’s still below the initial estimate of 353,000. I’m also suspicious when too many of the new jobs are in government.

Growth came from many of the usual sectors that have powered gains in recent months. Health care led with 72,000, followed by government (71,000), leisure and hospitality (49,000), and construction (39,000). Retail trade contributed 18,000 while the “other services” category added 16,000.

I was particularly interested to hear the number for wages. For March, average hourly earnings increased by 0.3% which matched expectations. Over the last year, average hourly earnings are up by 4.1%. That’s not bad, but it needs to be better.

Workers have seen that the rate of earnings growth has slowed down considerably (see above). To be clear, wages are increasing but at a slower rate.

However, the household survey, which is used to calculate the unemployment rate, posted an even more robust gain in March, up 498,000, more than absorbing the 469,000 increase in the civilian labor force level.

Gains tilted heavily to part-time workers in the household survey. Full-time workers fell by 6,000, while part-timers increased by 691,000. Multiple job holders rose by 217,000, to 5.2% of the total employment level.

The next inflation report is due out tomorrow. The last report showed that headline inflation increased by 0.4% in February, and the year-over-year rate is running at 3.2%. The core rate also rose by 0.4%, and it’s up by 3.8% over the past year. For tomorrow’s report, Wall Street expects to see both the core and headline rates increase by 0.3%.

Why Shorting Is a Very Tough Game

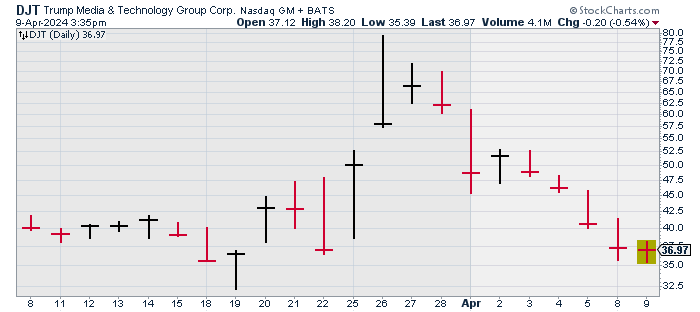

Two weeks ago, Trump Media (DJT) started publicly trading. The company merged with Digital World Acquisition Corp., a publicly traded shell company.

By any rational measure of value, Trump Media is wildly overpriced. The company currently has a market value of $5 billion even though it had total revenue last year of $4.1 million. That’s probably equivalent to a few 7-11 stores.

For the year, the company lost $58 million. On its first day of trading, DJT nearly hit $80 per share, but lately, it’s around $37 per share. I bring this to your attention not for any political reason but to show you how dramatic Wall Street can be.

Trump Media is currently the most expensive stock to short, meaning to bet against. In fact, it’s the most expensive to short by far. If you want to borrow shares of DJT to sell them short, you’d have to pay financing costs that run at an annualized rate of 750% to 900%. That compares with the average stock to finance at 0.71%.

This means that if you took a short position in DJT, you’d have to pay about $1 per day in financing costs. According to CNBC, “to break even on a new trade after one month, a short seller would have to see the share price of Trump Media drop by more than $30.”

I use this as a lesson that on Wall Street, even if you’re right, you can be wrong. The folks shorting DJT are betting on a sudden collapse. Even if the company turns out to be terrible, it could be a long, painful death. In fact, that’s what happens to many stocks.

I generally steer clear of shorting stocks. To be sure, it’s not hard to find stocks that are overpriced. But with a short, you’re making a few bets and only one is that the stock is too high. You also need to get your timing right. You need to see folks convinced that you were right all along. That’s not so easy.

Bear in mind that with a heavily shorted stock also runs the risk of a short squeeze. That happens when a widely-shorted stock starts to rise. Investors who are losing money then cover their short which pushes the shares even higher.

That can spark a cycle of ever higher prices, which essentially happened with Game Stop (GME) three years ago. Shares of GME rose from $5 to $87 in just 10 trading days. Now it’s at $11.

This is one of the many reasons why I prefer the long-only approach with no margin. Even if I’m wrong, time is on my side.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

P.S. If you want more info on our ETF, you can check out the ETF’s website.

Posted by Eddy Elfenbein on April 9th, 2024 at 5:31 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His