CWS Market Review – July 16, 2024

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Leadership Has Changed on Wall Street

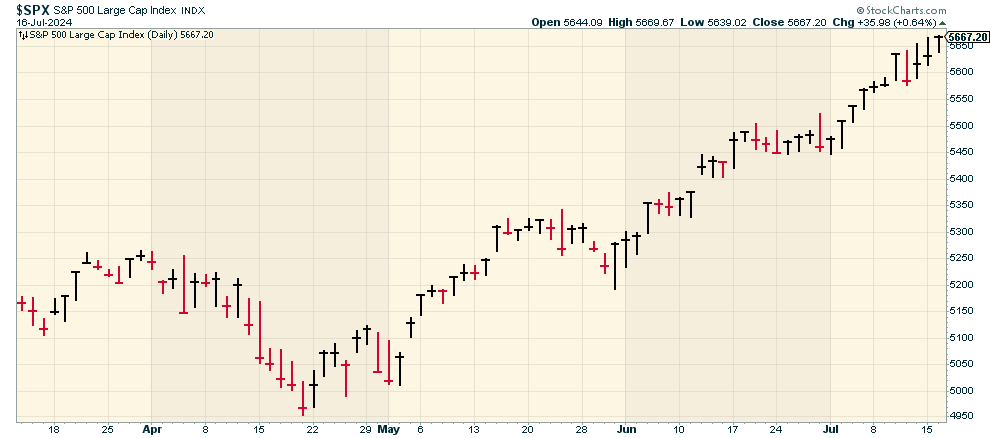

On Thursday, the stock market closed higher for the 13th time in the last 15 sessions. The S&P 500 hit another new all-time high – (take it away, Rita!). This is our 37th new high this year, and we’re only at the All-Star break.

What’s most striking about this rally is that the market’s leadership has abruptly changed.

Technology stocks, especially large-cap tech, had been leading the charge while many value stocks, typically smaller industrial stocks, had been lagging behind. The gap between growth and value had gotten unreasonably large.

That all changed with last week’s inflation report. What happened is that the benign inflation news has apparently given the go-ahead to the Federal Reserve to start cutting interest rates in September. The Fed has been clear that it wasn’t going to cut rates until it saw more evidence that inflation is well-contained. That’s exactly what it got.

The important fact for investors is that lower rates change the risk profile of the stock market. Value stocks usually benefit as rates head downward.

The current stock market has become an either/or market. The two competing camps are best represented by the Russell 2000 Index of small-cap stocks on one hand, and the Nasdaq Composite on the other.

Each day, the stock market seems to greatly favor one of these indexes, and it hates the other. It’s like a giant, multi-trillion dollar game of tug-of-war. Before last week’s inflation report, the Nasdaq was on fire and the Russell 2000 couldn’t do anything right.

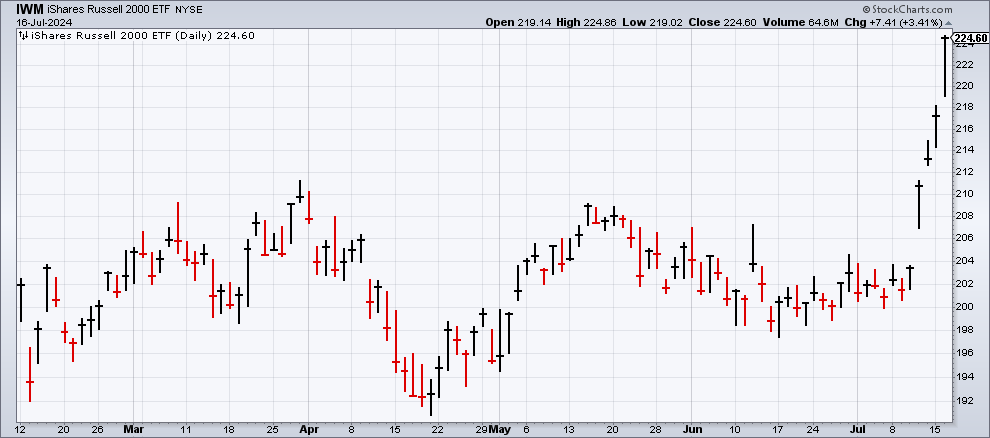

Since the inflation, everything has flipped. Check out this chart of the Russell 2000. It went nowhere for weeks, then suddenly, it lurched forward.

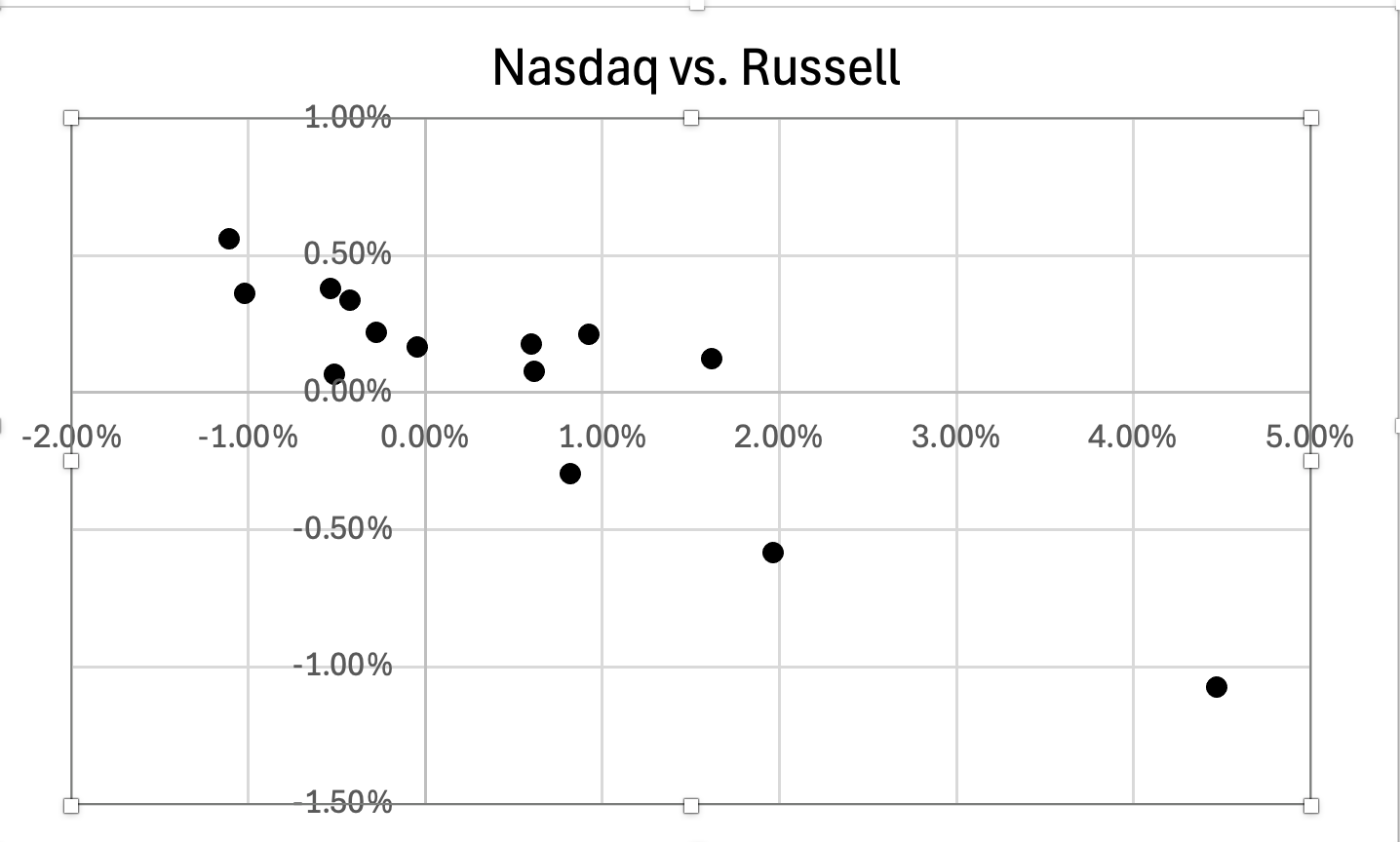

Here’s a chart that shows you how this has become an either/or market.

I made a scatterplot of the daily excess gain of the Nasdaq and the Russell 2000. By excess gain, I mean how much better or worse the index did compared with the S&P 500. The horizontal axis shows the excess gain of the Russell, and the vertical is the excess gain of the Nasdaq.

You can see how the dots make up a downward sloping line. In simpler terms, when one index leads the market, the other lags and vice versa. One side of Wall Street is yelling “Go Nasdaq!” and the other is yelling “Go Russell!” It’s as if there’s no middle ground. The Russell was up another 3.5% today while the Nasdaq was up only 0.2%.

The Nasdaq did well on days when we thought rates were going to stay high, but the Russell did well on days when we thought rates would fall. Since Thursday, we’ve strongly moved from the first camp to the second camp.

Notice the dot at the lower right? That was last Thursday, the day of the inflation report. The Nasdaq fell 2% that day and the Russell was up by more than 3.5%. That’s one of the largest spreads between the two in decades.

Will small-caps continue to lead the market? I’m inclined to think they will, but perhaps not as dramatically as the last four days.

It looks like the Fed may only be getting started with its rate cuts. The latest futures prices indicate a 93% chance of a rate cut in September. There’s a good chance that we may see two more rate cuts this year, plus a few more next year. It’s possible that interest rates may be 1% lower by this time next year.

Yesterday, Jerome Powell said, “We didn’t gain any additional confidence in the first quarter but the three readings in the second quarter, including the one from last week, do add somewhat to confidence.” The fact is that the labor market has cooled off a bit and the inflation news has improved.

The recent change in leadership has been good for our Buy List. From May to July, the Buy List had been lagging the market, but now things are looking better. That reminds me of a quote from Michael Gayed: “There are no gurus, only cycles.”

One of our Buy List stocks that’s perked up is the Federal Agricultural Mortgage Corporation (AGM), better known as Farmer Mac. Lower rates are clearly good for its business. In the last month, the stock has gained more than 24% despite no real news being released.

AGM hasn’t said yet when it will report earnings for this quarter, but going by past years, it will probably report around August 6. Wall Street currently expects Q2 earnings of $4.11 per share. Even after the recent rally for AGM, the stock is going for less than 12 times next year’s earnings.

Good Retail Sales Report for June

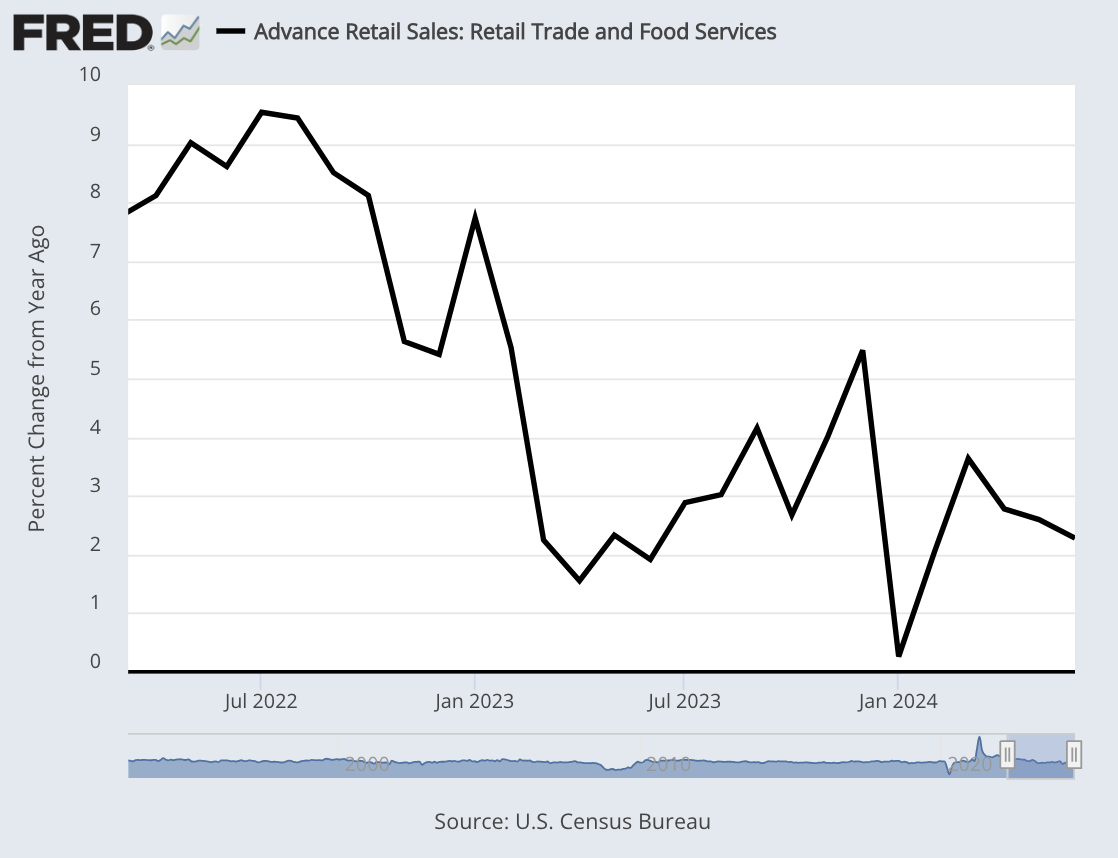

The stock market was helped this morning by a surprisingly strong retail sales report. Last month, retail sales, except for autos, rose by 0.4%. That’s the most in three months. Wall Street had been expecting an increase of 0.1%.

If we include autos, then retail sales were unchanged, but that includes a 2% drop of auto dealers. Wall Street was expecting a drop of 0.3%. The retail sales number for May was revised up to 0.1%.

These numbers suggest that consumers were in good health as they headed towards the close of Q2. Thursday’s numbers are good to see because the consumer hasn’t appeared terribly healthy this year. While wages have gone up, so has inflation. Also, higher interest rates from the Fed have made it more difficult to finance new buying.

Of the 13 categories tracked by the Commerce Department, only three registered declines. Those included sales of gasoline, reflecting lower prices in the month. Sales at sporting goods stores also edged lower.

If we exclude auto dealers and sales at filling stations, then retail sales rose by 0.8%. That’s the most since early 2023. Bloomberg notes that “sales at health and personal care stores rose by the most since October, while sales at building material and garden equipment stores increased by the most since February.”

Shoppers were active last month. Sales for online retailers rose by close to 2%, and home building stores saw an increase of 1.4%.

The reason why it’s good to exclude auto sales for June is that many car dealers were impacted by a cyberattack. AutoNation said it will take a big hit to its earnings report.

The housing starts report is out tomorrow. We’re going to have lots more earnings reports coming up soon. The next big economic report will come next Thursday when the government releases its first estimate of Q2 GDP growth. I’m expecting a number that’s low but positive.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on July 16th, 2024 at 6:12 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His