CWS Market Review – August 6, 2024

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The Stock Market’s Worst Day in Two Years

Yesterday was the stock market’s worst day in nearly two years. The S&P 500 plunged to a loss of 3%. At the start of trading, things were looking even worse. The Nasdaq opened lower by more than 1,000 points, or 6%. The Volatility Index shot up to a high of 65. That’s one of the highest levels it’s ever been. To be fair, it didn’t stay there long.

Many large-cap tech stocks got pummeled yesterday, the Mag 7 in particular. The market managed to rally a bit after a terrible open but by midday, the bears took control again and sent share prices downward. The Nasdaq 100 is having its worst start to a month since 2008.

We should remember that pullbacks are very normal, and they happen all the time. By historic measures, this isn’t a big one.

By general consensus, the problems started in the Asian markets, especially in Japan. On Monday, the Japanese stock market had its worst day since 1987. Then on Tuesday, it had its best day since 2008. The Nikkei was up more than 10% today. I don’t think that market will settle down soon.

The story begins last week when the Japanese Fed decided to raise interest rates. Well, sort of. More accurately, the Bank of Japan raised rates to “around” 0.25%. That’s up from the previous range of 0% to 0.1%.

That may not sound like a lot, and it’s not, but it’s the highest rate since 2008. The Bank of Japan also said it will reduce its monthly purchases of Japanese government bonds.

Unfortunately, in the U.S., we had a weaker-than-expected jobs report on Friday. This led to speculation that the U.S. economy is slowing down. I’ll discuss that in more detail in a bit.

Combine these two and you have fears that the “carry trade” is unwinding. Let me take a moment to explain, because the carry trade is what currently drives the world.

The carry trade is when investors can borrow money in a low-rate currency, such as the Japanese yen, and invest it in a currency with a higher interest rate, such as the U.S. dollar. The investors “carry” the money across the borders, and presto! It’s instant money.

The carry trade has been hugely popular in recent years, and many investors have cashed in. Bear in mind that as recently as April, Japan still had negative interest rates. The carry trade was a simple and easy path to free money.

Well, sort of. The carry trade is all fine and dandy as long as the currencies are far apart. Once that gets tripped up, you suddenly have a mad dash towards the exits, and that’s what happened. I’m sure many hedge funds had margin calls on their carry trade positions. There’s an old saying on Wall Street: “if you can’t sell what you want, sell what you can.” That’s pretty much what happened.

Kit Juckes, the chief foreign exchange strategist at Société Générale, said, “You can’t unwind the biggest carry trade the world has ever seen without breaking a few heads.” Indeed. Over the last three weeks, the global stock market has lost $6.4 trillion.

The Japanese yen had been gradually sliding against the dollar, until a few weeks ago. Then, all of a sudden, the yen started soaring versus the dollar (see the chart above).

What happened is that the weak jobs report caused investors to think that interest rates in the U.S. will soon go down.

Oddly, the carry trade isn’t over just yet, but a lot of folks are quickly closing their positions. No one wants to be the last one standing when the music stops.

The July Jobs Report Was a Big Miss

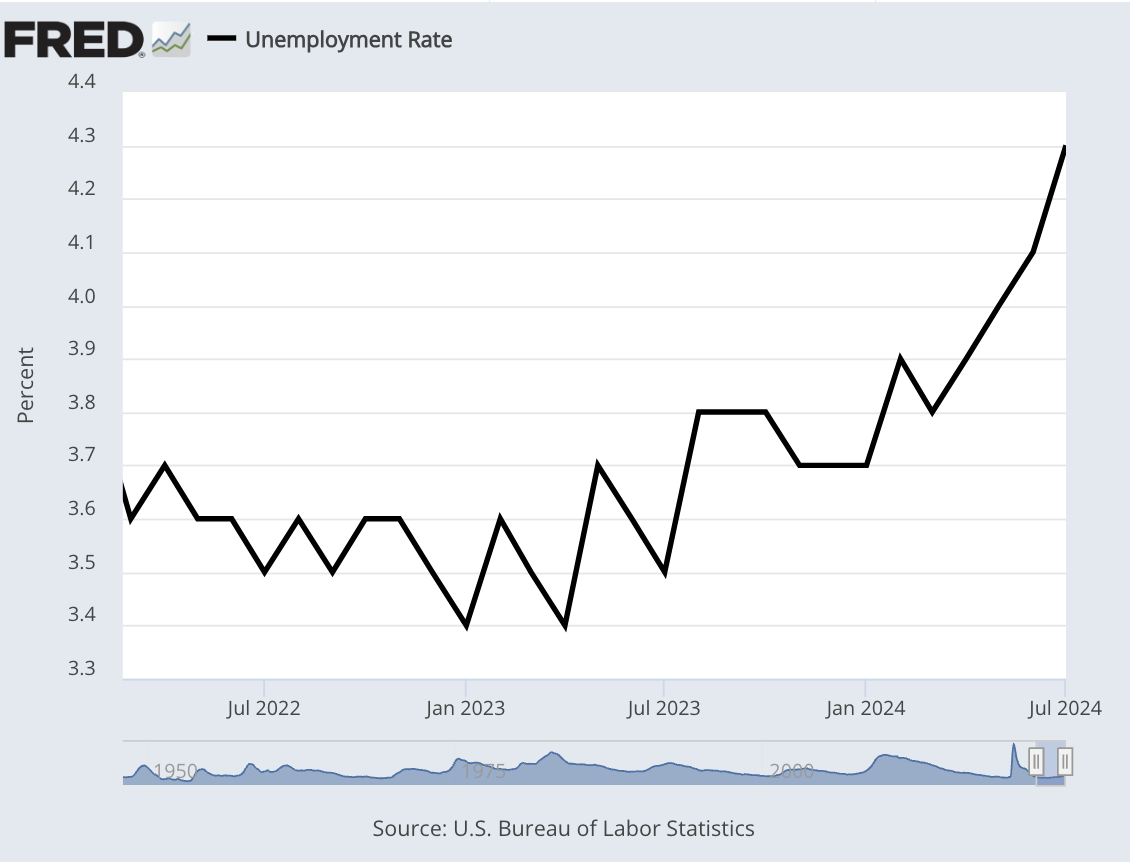

Let’s take a closer look at last week’s jobs report because that was another catalyst for the recent unpleasantness. On Friday, the Labor Department said that the economy created 114,000 net new jobs last month. That was a big miss. Wall Street had been expecting a gain of 185,000. The number for June was revised downward to a gain of 179,000.

The unemployment rate rose to 4.3%. That’s still quite low, but it’s the highest rate since October 2021. The U-6 rate, which includes discouraged workers, increased by 0.4% to 7.8%. That’s also the highest since October 2021.

Average hourly earnings increased by 0.2%. That was also below Wall Street’s forecast for 0.3%. That’s bad news for workers, but it will probably help lower inflation. Here are some more details:

From a sector standpoint, health care again led in job creation, adding 55,000 to payrolls. Other notable gainers included construction (25,000), government (17,000), and transportation and warehousing (14,000). Leisure and hospitality, another leading gainer over the past few years, added 23,000.

The information services sector posted a loss of 20,000.

While the survey of establishments used for the headline payrolls number was discouraging, the household survey was even more so, with growth of just 67,000, while the ranks of the unemployed swelled by 352,000.

Wall Street has quickly shifted from being bullish because rates are going lower to adopting a cautious outlook due to a fragile economy, and that’s sending rates down.

The change in sentiment has been dramatic. Now I hear investors complaining that the Fed is acting too slowly and that the elevated rates are hurting the economy.

Traders don’t believe the Fed’s forecasts anymore. Wall Street now narrowly expects a 0.5% rate cut next month. That would be followed by 0.25% cuts in November and December. After that, the market expects an additional three cuts before the end of April 2025.

Add it all up, and Wall Street sees the Fed targeting short-term rates between 3.50% and 3.75% within nine months. A few weeks ago, that outlook would have seemed looney. Now it’s the conventional wisdom.

What was interesting about yesterday’s stock market is that the biggest gap wasn’t between growth and value, as we’ve seen with the big rotation. Instead, the gap was between cyclical stocks and defensive stocks. In other words, traders were arguing about the health of the economy, and the bears were getting their way.

Wall Street bounced back some today. The old Wall Street rule is that you walk back one-third of a big move, and that proved fairly accurate today. Both the S&P 500 and Nasdaq rose a little more than 1% today.

Interestingly, the stock market peaked on July 16 which seems to be a popular time for market peaks. In 2022, the S&P 500 peaked at 4,130.29 on July 29 and then sank 13.4% to 3,577.03 on October 12th.

In 2023, the S&P 500 peaked at 4,607.07 on July 27th and then sank 10.6% to 4,117.37 on October 27.

In 1990, the S&P peaked at 368.95 on July 16th and then fell 20% to 295.46 on October 12th, mostly in response to Saddam Hussein’s invasion of Kuwait on August 2.

Then, in 1998, in a carbon copy of 1990, the S&P peaked at 1,186.75 on July 17th and then fell 19.2% by October 8th.

Broadridge Rallies on Earnings and Guidance

I wanted to touch on Tuesday’s earnings report from one of our Buy List stocks, Broadridge Financial Solutions (BR). I’ll have more details on it in our premium issue later this week, but the company is doing so well that I wanted to share it with you.

The company runs a great business. This is how Barron’s described Broadridge two years ago:

The company has a near monopoly in the business of managing and distributing investor communications for practically every public company in the U.S., plus mutual funds, exchange-traded funds, and more. That includes proxies, regulatory disclosures, and other reports and filings required of all U.S. securities issuers. Those are non-discretionary communications that companies and funds need to distribute no matter what the world is doing. That segment tends to grow at the pace of overall stockholdings in the U.S., with Broadridge able to eke out higher profit margins thanks to a continuing shift from printed documents delivered by mail to digital investor communications.

Broadridge’s fiscal Q4 earnings rose 9% to $3.50 per share. That matched Wall Street’s consensus. The company also raised its dividend by 10% to $3.52 per share. This is BR’s 18th annual dividend hike in a row. It’s also the 12th double-digit increase in the last 13 years.

For the coming year, Broadridge sees recurring revenue growth of 5% to 7%, and adjusted EPS growth of 8% to 12%.

Broadridge has been a great stock for us. The shares got a nice 4.8% jump in today’s trade. Since the start of 2023, Broadridge has gained 67% for us.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on August 6th, 2024 at 6:20 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His