CWS Market Review – September 24, 2024

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

The Federal Reserve Cuts By 0.5%

Last week, the Federal Reserve voted to lower interest rates by 0.5%, although I think it’s more accurate to say that the Fed undid some of the historically aggressive rate hikes it deployed in 2022 and 2023.

Over a 16-month period, the Fed hiked short-term interest rates a total of 525 basis points. The aggressive rate hikes were intended to combat a nasty bout of inflation. At one point, inflation was running at more than 9%.

Now, more than a year after the last Fed hike, and with inflation trending below 3%, the central bank decided to slash rates by 0.5%.

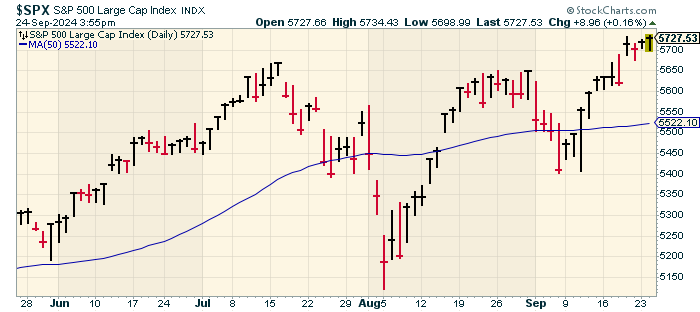

I admit I didn’t think the Fed would go through with a rate cut that large. So far, Wall Street seems quite pleased with the move. Today the S&P 500 closed at another all-time high, its 41st of the year. The Nasdaq was up as well but it’s still below its high from more than two months ago.

Overall, this has been a good year for the stock market. The S&P 500 Total Return Index, which includes dividends, is up 21% this year. We’re about to close out Q3, and the S&P 500 is on track for its fourth quarterly gain in a row.

It looks like this will only be the first in a long series of rate cuts. For the November meeting, traders are evenly split on whether the Fed will cut by 0.25% or by 0.50%. That meeting will be shortly after the election.

While the exact plans are in doubt, the overall strategy is clear: the Fed is leaning towards cutting rates. Over the next four meetings, traders expect the Fed to cut interest rates by a total of 1.5%. That makes sense if you believe that inflation has been whipped.

Still, this is an unusual rate cut because it’s happening while unemployment is still low (but rising) and the stock market is strong. I have my doubts that we can easily settle back into the economic environment we had before the last bout of inflation.

It’s also unusual that the financial markets are seemingly unbothered even though there’s more evidence that Americans are apprehensive about the future. A good example is that earlier today, shares of Lowe’s (LOW) and Home Depot (HD) both reached new all-time highs. I highlight the home improvement duo because they’re a good indicator of what the economy is doing at the ground level.

Other industrial stocks like 3M (MMM), Caterpillar (CAT), Sherwin-Williams (SHW) and Carrier Global (CARR) also hit new highs.

What’s Next for the Fed?

In last week’s Fed decision, the only dissenting vote came from Michelle Bowman. What makes her dissent noteworthy is that Bowman is a Fed Governor, not a regional bank president. Typically, Fed Governors vote in line with the Fed chair. Bowman’s dissent is the first for a Fed governor in nearly 20 years. She believes that the Fed should be cutting by only 0.25%.

Earlier today, Bowman spoke before a group of bankers in Kentucky where she had a chance to explain her decision. She said that the Fed’s big cut “could be interpreted as a premature declaration of victory on our price-stability mandate.”

There’s also a basic thought that inflation, however you want to measure it, is still not at the Fed’s target rate of 2%. The rate cut assumed that inflation will safely glide itself into port. Bowman also believes that a cut of 0.5% would signal to the market that the economy is in greater peril than it truly is.

The two-year Treasury yield has a decent track record of running just ahead of the Fed on interest rates. Right now, there’s a big divergence between the two. Even after the rate cut, the Fed funds rate is still 1.2% above the 2-year yield. That’s a good sign that more cuts are coming.

Indeed, there are still worrying signs about the economy. Earlier today, the Conference Board said that its measure of consumer confidence dropped from 105.6 in August to 98.7 for September.

That was the biggest drop since August 2021, and it was below Wall Street’s expectations for 104. For context, before Covid, consumer confidence reached 132.6 in February 2020. Of the economic subgroups, the largest drop in confidence came among those making less than $50,000. Stocks are happy while consumers are tapped out.

Another good example of this was today’s Case-Shiller report which showed that home values hit another new high, but housing affordability, which adjusts for mortgages costs, is near the lowest on record.

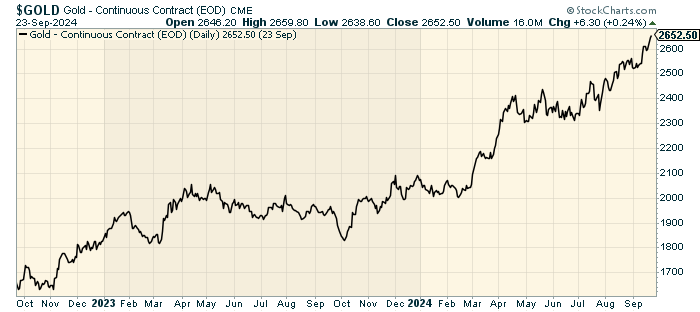

Another troubling sign is that the price of gold has been rallying strongly. Typically, this is a crisis asset that investors flock to during turbulent times. Reuters reports that most banks expect gold’s run to last into next year. On Tuesday, the Midas metal got as high as $2,639.95 per ounce. Gold is having a great year.

On Thursday, the government will offer its second revision to the Q2 GDP report. The last report said the economy grew at a real, annualized rate of 3% during the second three months of the year. I’m curious how well the economy did during Q3. For now, Wall Street is sounding optimistic. The Atlanta Fed’s GDPNow model estimates the economy grew at a 2.9% rate for Q3. Goldman Sachs said it expects growth of 3.0%.

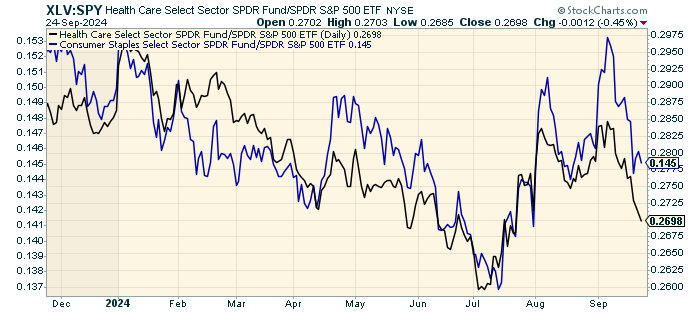

Typically, as the economy gets weaker and the Fed lowers rates, we can expect that defensive stocks will do well. Over the summer, many defensive stocks started to perk up and outgained the rest of the stock market.

Here’s a chart of the S&P 500 Consumer Staples ETF (XLP) and the S&P 500 Healthcare ETF (XLV) divided by the S&P 500 ETF (SPY).

You can see how the market changed its mind. At one point, no one wanted anything to do with defensive stocks, but this summer, they got hot again (although they’ve been slipping back down lately).

I think this trend has more room to run. Defensive stocks offer more stability and often higher dividends than the rest of the market. Also, many defensive areas of the market have fallen to favorable valuation metrics.

On our Buy List, this means stocks like Hershey (HSY) or Stryker (SYK). For income investors, that means utilities like American Water Works (AWK).

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on September 24th, 2024 at 5:52 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His