CWS Market Review – October 22, 2024

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Q2 Earnings Are Looking Good (Mostly)

Q2 earnings season is in full swing. This week, 112 members of the S&P 500 and seven of the 30 stocks in the Dow are due to report earnings. The early numbers look mostly good. The good news is that more companies are beating earnings, but they’re doing it by smaller amounts.

This looks to be the fifth quarter in a row of earnings growth, but it will be the slowest growth in the last year.

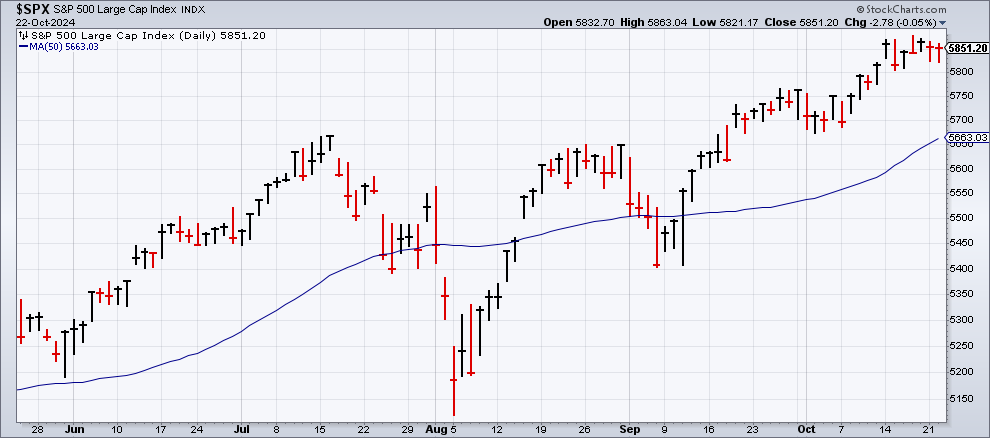

The stock market doesn’t seem terribly concerned. The S&P 500 is down a bit since its last all-time high close reached on Friday.

The stock market has had a very impressive run since the last low reached in early August. The index is currently more than 3% above its 50-day moving average.

So far, 14% of the companies in the S&P 500 have reported earnings results. Of those, 79% have beaten expectations. That’s a little above the usual rate. (Yes, on Wall Street, you’re expected to beat expectations.)

Companies are reporting results that are 6.1% above expectations. That’s lower than normal. Over the last five years, companies have topped results by 8.5%.

Digging into the details, we’ve seen decent results from many large banks, but the weak spot is that we’ve seen lower guidance from industrials.

Some of these numbers for expectations have been helped by analysts cutting back on their forecasts. Earnings growth is now tracking at 3.4%, but that’s down from 4.3% at the end of Q3.

Of the companies that have reported so far, 64% have beaten on revenue which is a little below the five-year average of 69%. On average, companies are beating on revenue by 1.1%. That’s below the five-year average of 2%.

If 4.7% is the actual revenue growth rate for the quarter, it will mark the 16th quarter in a row of positive revenue growth.

The “Magnificent 7” stocks are expected to report earnings growth of 18.1% for Q3. If you took those seven out of the S&P 500, then the other 493 stocks are expected to report earnings growth of 0.1%.

For this calendar year, analysts expect earnings growth of 9.4%. They see that ramping up to 15.1% for next year. I expect to see both numbers gradually lowered. The forward price/earnings ratio is currently 21.9 which is elevated but not extreme.

Moody’s Posts a Big Earnings Beat

Seven of our Buy List stocks are due to report this week. We already had three reports out earlier today. I’ll go over all of them in our premium issue, but I wanted to highlight one of them for today’s issue.

For Q3, Moody’s (MCO) said that its adjusted earnings rose 32% to $3.21 per share. Wall Street had been expecting $2.86 per share. The CFO said this was a “fantastic” quarter for Moody’s and I agree.

Moody’s also raised its full year guidance to a range of $11.90 to $12.10 per share. The previous range was $11 to $11.40 per share. Since Moody’s has already made $9.85 per share so far this year, the new guidance implies Q4 earnings of $2.05 to $2.25 per share. Wall Street had been expecting $2.18 per share.

CEO Rob Fauber said:

“Moody’s record-breaking revenue performance in the third quarter is a testament to our unwavering status as the Agency of Choice for our customers and our actions to prime the business for durable future growth. In parallel, we delivered strong recurring revenue growth in our analytics business, driven by investments and innovation that enhance our offerings and empower our customers with the insights necessary to navigate the complexities of an increasingly dynamic risk environment.”

The stock fell after the earnings report, but I’m not at all concerned. It’s not unusual for our stocks to drop after their earnings reports. The company continues to do very well. Over the last two years, shares of Moody’s have doubled for us, and that includes some big drops.

This week will be dominated by earnings news. There’s not much going on as far as economic reports. Several Fed officials will be speaking but that’s usually not so important for economic news.

Next week, however, will see some important news. The October jobs report will be out next Friday, November 1. If you recall, the jobs numbers for September were quite good. The U.S. economy created 254,000 net new jobs last month.

The other report to look out for is the first report on Q3 GDP. Of course, this report will be revised many times, but next Wednesday we’ll see the government’s first stab at it. Growth for Q2 was 3.0%. The Atlanta FED’s GDPNow model sees Q3 growth of 3.4%. That would be very impressive.

If the economy is doing better than expected, then we can see possible evidence in other places. For example, the yield on the 10-year Treasury has slowly crept higher. On October 1, the 10-year yield was 3.74%. By Monday’s close, it had risen by 45 basis points.

Tied to the higher bond yields is that growth stocks have been outperforming value stocks over the last few weeks. It’s not by a huge amount but the value/growth divide often mimics what Treasury bonds are doing.

Stock Focus: MarketAxess

Lately, I’ve been watching shares of MarketAxess (MKTX). This is a good example of a company that’s fairly large but not well known outside the world of financial data.

The company runs an electronic trading platform for the institutional credit markets. In other words, this is how the big boys trade bonds, and MarketAxess dominates the field. In electronic trading, 85% of bonds are traded on MKTX’s platform, as are 84% of junk bonds. That works out to 20% of all corporate bond trading in the U.S.

The company was started by Richard McVey in 2000, and he served as CEO until last year. The stock IPO’d in 2004 at $11 per share and it was a huge success. By 2020, MKTX got to $600 per share. Then it started to struggle. Earlier this year, the stock dropped below $200 per share.

Is there a potential bargain here? Possibly. MKTX dominates its business, and the company continues to be profitable, although it’s not seeing much growth in recent years. The business was impacted last year by lower corporate bond issuance.

The stock is suddenly popular again. In August, MKTX reported Q2 earnings of $1.72 per share. That was a four-cent beat. Last week, the stock briefly broke above $300 per share. That’s a huge turnaround for a short period of time.

MarketAxess is due to report earnings again on November 6. Wall Street is looking for earnings of $1.85 per share. The stock is hardly cheap. It’s currently going for about 35 times next year’s earnings. At a lower price, it could be worth buying.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on October 22nd, 2024 at 2:19 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His