CWS Market Review – April 22, 2025

(This is the free version of CWS Market Review. If you like what you see, then please sign up for the premium newsletter for $20 per month or $200 for the whole year. If you sign up today, you can see our two reports, “Your Handy Guide to Stock Orders” and “How Not to Get Screwed on Your Mortgage.”)

Before this week, the battle on Wall Street was over tariffs. Now it’s over tariffs and interest-rate policy. President Trump took to social media to call Federal Reserve Chairman Jerome Powell, “a major loser.”

In the history of White House/Central Bank relations, that’s probably one of the more polite salvos (Google “Andrew Jackson” and the “Bank War” if you want to see what I mean.)

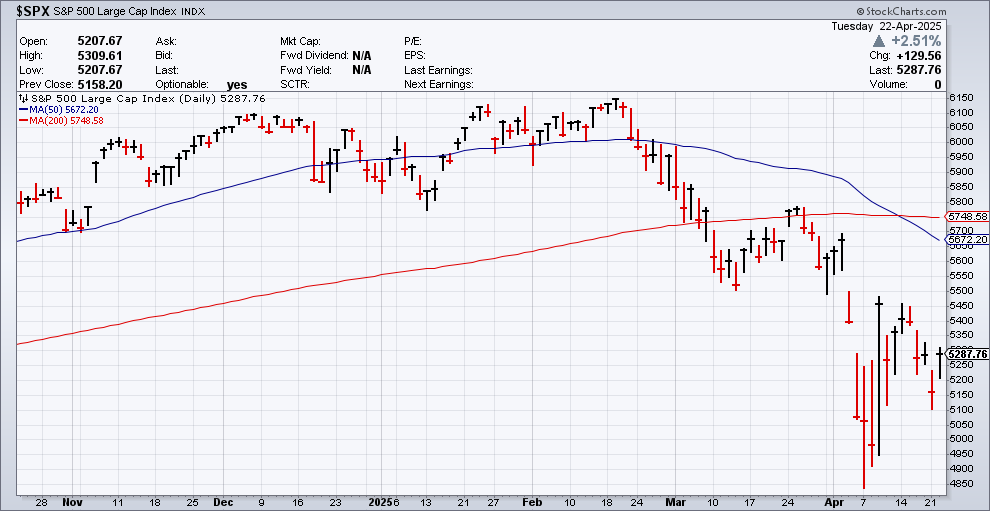

Wall Street was not particularly pleased with the president’s remarks. The U.S. stock market is now off to its worst start for a presidential term since at least 1928. The Dow is on pace for its worst April since the Great Depression.

Somebody call T.S. Eliot!

At one point in yesterday’s trading session, the S&P 500 was off by 3.4%. To put that in context, that day was worse than every single trading day in 2023 and 2024. Yet for this April, it would only be the fourth worst. Fortunately, we were spared somewhat as the market did rally off yesterday’s low.

One interesting side note to yesterday’s sell-off was how broad it was. It’s as if every stock lost around 2.5% plus or minus 1%. Of course, that’s not literally true, but in no sense did we see the massive rotation action that we saw earlier this month. By this, I’m referring to days when growth stocks were through the floor but value stocks shot up. Or the opposite. Yesterday, most everything was down.

Today’s recovery was perhaps even broader than yesterday’s. For example, the S&P 500 Growth ETF was up 2.71% today while the Value ETF was up 2.34%. That’s very narrow, especially for a big day.

The narrowness of this market suggests that the market is most concerned with valuations on a broad level, not with any specific sector or industry. In plain English, yesterday Wall Street thought stock prices were too high. It walked some of that back today.

Another optimistic item came today when Bloomberg reported that Treasury Secretary Scott Bessent believes that the “tariff standoff with China is unsustainable and that he expects the situation to de-escalate.”

“Bessent also said the world’s top two countries essentially have a trade embargo in place, with both slapping tariffs of more than 125% on each other’s goods.”

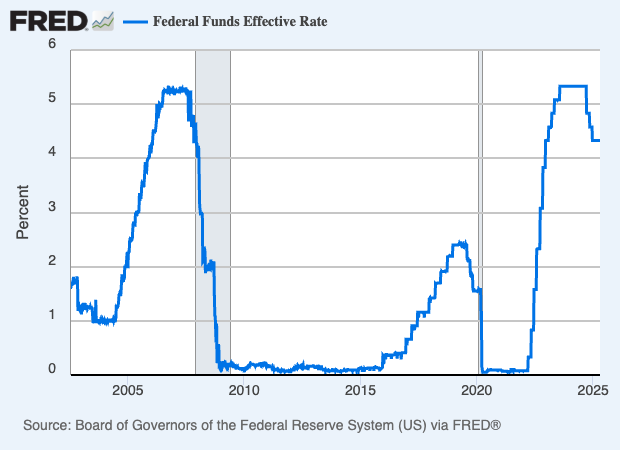

As for the Trump-Fed squabbles, the president may soon get his way. The FOMC meets again in two weeks, and I doubt anything will happen. After that, however, the Fed meets in June and I think there’s a very good chance that the central bank will cut rates by 0.25%.

That may not be enough for the president’s liking, but traders expect three more rate cuts this year after the cut in June. It’s broadly understood that the president can’t fire the Fed chief unless it’s for cause, meaning something like misconduct. The Fed chairman can’t be dismissed because of a policy disagreement. Powell’s term isn’t up until May of next year, and things may be quite different then.

Earnings from Moody’s and Mueller

We had two Buy List earnings reports. I’ll cover these in greater depth in our premium newsletter (which you can sign up for here). I also want to stress how well our Buy List is doing against the broader market. In fact, in relative terms, the last several weeks have been some of our best in the 20-year history of our Buy List.

Let’s start with Mueller Industries (MLI). This is one of those well-run small-to-mid caps that’s not well known on Wall Street. The company has a market value of roughly $8 billion. Since early 1992, the stock is up by 40,000%. You’d think that would attract more interest, but that’s not the case.

I can’t say it’s completely ignored by Wall Street, but Mueller is currently followed by just one Wall Street analyst. Personally, I love finding little-covered stocks.

Here’s a chart of Mueller. The S&P 500 (in red) looks like a flat line in comparison. It’s actually a gain of 1,150%.

Mueller makes and sells copper, brass, and aluminum products. The company operates through three segments: Piping Systems, Industrial Metals, and Climate.

For Q1, Mueller had operating income of $206.3 million. That’s up 12.4% over last year. Net income increased 13.7% to $156.4 million. Quarterly sales increased 17.6% to $1 billion. Mueller’s EPS rose 14.9% to $1.39. The lone analyst had been expecting $1.31 per share.

During the quarter, the price for copper averaged $4.57 per pound. That’s up 18.4% over last year’s Q1.

Mueller said that the increase in sales was attributable to the inclusion of sales from two recently acquired businesses, and also to higher selling prices related to the rise in raw material costs and tariffs. At the end of the quarter, MLI had a cash balance of $830.1 million.

Regarding the quarter performance, Greg Christopher, Mueller’s CEO said, “We delivered very good results in the first quarter despite certain manufacturing disruptions, which have since been resolved, and the general economic landscape. We were particularly pleased with the positive contributions that our Nehring Electrical Works and Elkhart Products acquisitions made to our business, and we look forward to their continued improvement.”

Regarding the outlook, Mr. Christopher continued, “While markets and demand are in line with our year end comments and outlook, the tariff and trade policies have presented new challenges. Although we largely manufacture our products in the countries where they are consumed, we are not immune to the effects of tariffs. Where required, our teams are proactively and diligently taking appropriate price actions and will continue to do so as necessary. As we have consistently demonstrated resilience during past periods of disruption, we are confident in our ability to effectively navigate the current environment.”

Mueller is now going for just under 11 times next year’s earnings. The company pays a quarterly dividend of 25 cents per share, which yields about 1.4%. The stock got a nice 2.7% bounce in today’s trading.

Moody’s (MCO) has been a great stock for us. We added it in 2017, and it’s been a big winner for us. I’m glad to see MCO is outpacing the market this year as well, although that means it’s down by less.

For the quarter, Moody’s revenues increased by 8% to $1.9 billion. Moody’s business is really two businesses. There’s Moody’s Investor Service (MIS) and Moody’s Analytics (MA), which is the jewel in the crown.

Last quarter, revenues at MIS increased by 8% to $1.1 billion. Revenue at MA increased by 8% to $859 million. Earnings increased 14% to $3.83 per share. That’s a healthy beat. Wall Street had been expecting $3.54 per share.

Companywide, Moody’s had an operating margin of 51.7%. For MIS, it was 66% and for MA, it was 30%. Cash flow from operations was $757 million and free cash flow was $672 million.

During Q1, Moody’s bought back 800,000 shares at an average cost of $481.77 per share and issued net 400,000 shares as part of its employee stock-based compensation programs.

This was another very good quarter for Moody’s. The only downbeat is that it lowered its guidance for the coming year. Previously, Moody’s had been expecting full-year earnings to range between $14 and $14.50 per share. Now it sees 2025 earnings ranging between $13.25 and $14 per share. I think that’s a sign of the current environment instead of the health of Moody’s business.

Shares of Moody’s rallied 4% today.

Outside of earnings, we’ll have some important news items towards the end of next week. The ADP payrolls report will be out on Wednesday, April 30. The ISM Manufacturing report will be out the following day. After that, the April jobs report will be due out on Friday, May 2.

Also on Wednesday, we’ll get our first report on Q1 GDP growth. Wall Street is not looking forward to this report. The consensus seems to expect Q1 GDP growth between 0% and 1%. That’s not very good. We’re not in a recession yet, but one may not be too far away. As it turns out, the major loser could be the economy.

That’s all for now. I’ll have more for you in the next issue of CWS Market Review.

– Eddy

Posted by Eddy Elfenbein on April 22nd, 2025 at 5:24 pm

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His