Steel’s Revival

In 1941, Art Rooney decided to change his football team’s name from the Pittsburgh Pirates to the Pittsburgh Steelers to reflect the city’s blue-collar image. Like the football team, the steel industry has had a difficult past 25 years. But also like the football team, the industry has gone through a remarkable turnaround.

In today’s IBD, Amy Reeves notes:

In the 1980s and ’90s, steel was a symbol of the dying Old Economy. Mines closed, companies went bankrupt, and workers were laid off despite their union muscle.

But even as the new tech workers declared themselves to be the future, they were still driving steel cars, eating out of steel containers and living and working in buildings framed with steel girders. So after enough cutbacks, demand was bound to outstrip supply.

That finally happened in recent years, bringing better days to steel producers.

This time, companies aren’t content to simply ride the swings of the commodity cycle.

The industry’s leaders are taking steps to prepare for the next downturn — by cutting costs, improving technology and, above all, consolidating. That’s especially important right now, since some signs are showing that the current upturn may have peaked.

Makers of specialty alloys, meanwhile, are still rising untrammeled. The booming aerospace, technology and medical markets are constantly looking for high-tech metals with special properties.

With the emergence of Mittal (MT), the industry is going through a rapid consolidation:

The number of steel firms in North America and Europe has been shrinking for some time.

Since the end of 1997, according to Considine, no fewer than 32 U.S. steel companies have filed for bankruptcy. The last was Stelco in January 2004.

More recent headlines have shown the industry’s urge to merge. In the last few months, a bidding war erupted between European giants Arcelor and ThyssenKrupp for Canada’s Dofasco. No sooner did Arcelor emerge the victor than Mittal Steel moved in with a hostile bid for Arcelor.

Europe started the consolidation trend before North America did, Sharkey notes. That explains why the Continent holds some of the largest and richest steel makers. But as the Dofasco battle shows, they’d still like a piece of the North American auto market.

Analyst Chris Olin of Longbow Research expects to see more of this, since the industry is still “way too fragmented.”

If Mittal succeeds in buying Arcelor, that will noticeably de-fragment the industry right there, since the new firm would be bigger than its next three rivals combined.

“Mittal’s attempt to buy Arcelor is a game changer,” Olin said. “Everybody’s in play now.”

At this point, those in the U.S. steel industry sound less worried about Europe than about China. China supplies 30% of world steel production, Sharkey says, and is growing at warp speed.

Sharkey and Considine feel the U.S. steel industry has suffered from unfair trade practices and foreign government subsidies. “We have a very competitive industry globally,” Sharkey said. “But we can’t compete with governments.”

Considine believes that President Bush’s hotly debated decision to impose steel tariffs from March 2002 to December 2003 gave the domestic industry crucial cover while it restructured.

Olin disagrees, saying a change in the dollar and skyrocketing shipping costs were what really curbed imports.

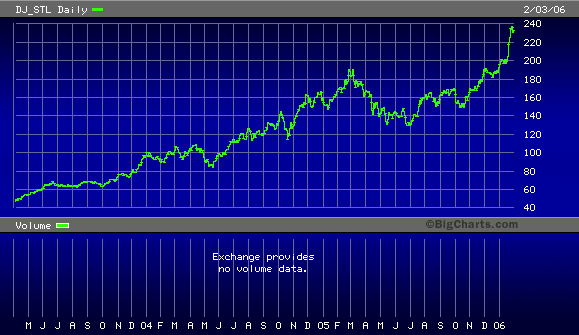

The other big part of the steel story is China. Here’s a chart of the Dow Jones Steel Index since April 2003.

Posted by Eddy Elfenbein on February 6th, 2006 at 10:58 am

The information in this blog post represents my own opinions and does not contain a recommendation for any particular security or investment. I or my affiliates may hold positions or other interests in securities mentioned in the Blog, please see my Disclaimer page for my full disclaimer.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His