Archive for 2005

-

Broker Ad

Eddy Elfenbein, November 10th, 2005 at 11:39 amClick here to see the worst broker ad ever (via Michael Covel).

-

Patterson Companies

Eddy Elfenbein, November 10th, 2005 at 11:20 amOne of the things I like about this blog is that it let’s me think out loud. For example, there’s one stock I’ve been following that I’m truly undecided about. The company is Patterson Companies (PDCO). It’s exactly the kind of stock I like. Steady earnings growth, high returns-on-equity and consistent operating history.

The company makes supplies for the dental industry, and it’s a major supplier for the veterinary industry (don’t laugh, it’s very profitable). For several years now the company has grown its earnings by 20% a year like clockwork. To come up with an estimate for next quarter, all you had to do was add 20% to last year’s quarter, plus or minus a penny, then sit back and watch. The stock acted like a bond with a 20% coupon. Here’s the company’s earnings-per-share for the last 10 fiscal years:

1996 $0.22

1997 $0.25

1998 $0.31

1999 $0.38

2000 $0.48

2001 $0.57

2002 $0.70

2003 $0.85

2004 $1.09

2005 $1.32

Not too shabby. There aren’t many companies like that. But then the bombshell came. In May the company totally and completely missed earnings. Wall Street was expecting 39 cents a share, Patterson made only 36 cents. That’s like Tiger Woods missing a three-foot putt. What the hell happened? The year before, Patterson had earned 33 cents a share. This was so…unexpected. The market freaked out and Patterson’s stock fell 14% in one day.

Wall Street started to bring down its earnings estimates, and in August Patterson missed again! This time, the Street was expecting 32 cents a share compared with 30 cents the year before, but Patterson reported 31 cents. This couldn’t be happening!

How could this happen for two straight quarters? I was baffled—plus, I could never understand the company’s explanation. It seemed that business was quite simply slower. Was this just a blip, or was there something bigger at work?

I’m very suspicious of “blips.” I just don’t like them. I don’t consider myself a bottom-fisher, and I stay away from turnaround plays. Some companies do turn around, it’s just very, very, very hard. For every one Harley Davidson (HDI), there are ten Rite Aids (RAD). Patterson’s stock has continued to drift lower, and it’s now over 22% off its pre-bombshell high. But I’m still too afraid to go in. Yes, I know. Bock. Bock. But I just can’t pull the trigger.

Earnings are due again on November 23 and I’m already sweating. Should I be this emotional about a stock I don’t even own? Last year, Patterson made 31 cents a share and said it’s expecting earnings of 35 cent to 37 cents a share for this quarter. I’m almost as afraid of a good quarter as I am of a bad one. If Patterson delivers great results, should I go back in? I just can’t ignore two lousy quarters. If the results are rotten, then the story is easy. The company just ain’t no good no more.

But what if it’s a screaming buy and I’m not listening? -

General Motors to Restate Earnings

Eddy Elfenbein, November 10th, 2005 at 10:05 amYesterday, it was AIG (AIG). Now General Motors (GM) is restating earnings from 2001. When it rains, it pours:

General Motors said it would restate its financial results for 2001 by up to $400m because of accounting errors while losses for the second quarter of 2005 quadrupled after a revision of its holding in Fuji Heavy Industries.

The world largest carmaker, which is already suffering from four consecutive quarters of losses and the collapse of its main parts supplier Delphi, said in a filing with the Securities and Exchange Commission that its 2001 earnings were overstated by $300 million to $400 million, but the final amount hasn’t been determined.It once was a giant. Here’s a chart showing the decline of GM’s credit rating over the past 25 years.

-

Expect Three More Fed Rate Hikes

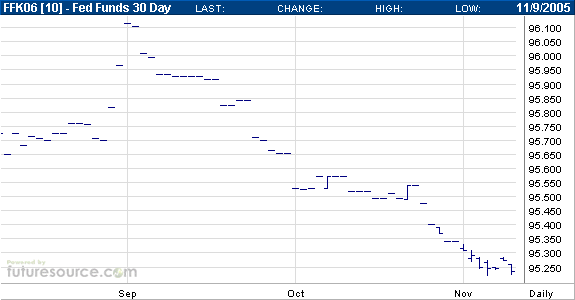

Eddy Elfenbein, November 10th, 2005 at 9:59 amWilliam Poole, the President of the St. Louis Federal Reserve Bank, said yesterday that the Fed’s interest-rate policy ought to be “risk-averse.” That may not seem like a big deal, but in the carefully-worded world of central bankers, that’s considered to be going ape shit. I’m surprised Poole wasn’t taken down with a Taser.

In English it means, or the market is taking it to mean, that the Fed is going to raise rates three more times. Until now, the market was expecting two more rate hikes—one on December 13, and another on January 31, which is also Greenspan’s last day. Now the market is also expecting another rate increase at the Fed’s March 28th meeting. That will bring the Fed funds rate up to 4.75%.

Here’s a graph of the futures contract for the Fed funds rate for next May. You can see the spike around the time of Katrina when the market thought the Fed might put off its rate hikes. Even though that was just over two months ago, the market’s perception has since changed quite dramatically.

The 10-year Treasury bond is currently yielding 4.64%, so the yield curve could be slightly inverted in just a few months. The 30-year Treasury is yielding 4.82%. Actually, it’s a 26-year bond; the U.S. Treasury hasn’t issued a 30-year in four years. But thanks to budget deficits, they’ll be returning in February.

The interest rate gap between the U.S. and Europe has been getting steadily wider, which has helped the dollar rally this year. Two straight weeks of rioting has also helped the greenback. On the other hand, the trade deficit surged to a new record in September. The trade deficit jumped 11.2% to $66.1 billion. The deficit with China was over $20 billion. -

The Market Today

Eddy Elfenbein, November 9th, 2005 at 5:45 pmThe market closed its fifth straight boring-as-hell day. Not that I’m looking for excitement, but this is getting ridiculous. Let at these numbers: the Dow, +6.49 points, the Naz +3.74 and the S&P 500 +2.06. Of the 100 stocks in the S&P 100, 74 moved less than 1% today. This is like watching the WNBA. The VIX (^VIX) is now back below 13.

Here’s something a little bit interesting. After an accounting scandal earlier this year, American International Group (AIG) restated its profits for the last five years. It turns out that the company had overstated its profits by $3.9 billion. Hey, those pesky decimals can be kinda confusing. Millions, billions, kilometers, it’s all one big blur. Well, now the company is correcting the correction. AIG says that it understated the previous correction by $500 million. That’s nice to know but something tells me this story isn’t quite over.

Here’s a little tidbit from the Wall Street Journal on Hank Greenberg, AIG’s former Grand Poobah.When AIG executives traveled with him on business, they were required to use the small pilots’ bathroom in the front of a corporate plane. A large, fancy bathroom in the back of the plane could be used only by Mr. Greenberg, his wife and their Maltese dog, Snowball, according to a former AIG executive.

A dog named Snowball? Wasn’t that Trotsky in Animal Farm? Or wait, that was a pig. But still, Snowball? The bathroom??

Moving on, the Buy List had a decent day. We beat the market again. The S&P 500 was up 0.17%, and the Buy List was up 0.44%. Both Fair Isaac (FIC) and Expeditors (EXPD) hit new 52-week highs. Danaher (DHR), the tool company, reiterated its fourth-quarter forecast. I like to see companies do that around the middle of a quarter.

Outside our Buy List, Cisco (CSCO) reported earnings after the close. I’m enjoying this because this is the first time Cisco is required to expense its stock options. Several tech stocks fought this regulation hard. Cisco regularly had its earnings inflated by about 20%.

Just two months ago, Cisco was trying to get the SEC’s approval on a shady option-expensing scheme. Fortunately, the SEC shot them down. I always enjoyed hearing people on CNBC say that Cisco has a P/E ratio of around 16. Yes, by their accounting.

For the quarter, Cisco earned 25 cents a share, 20 cents without options. Including options, the Street was looking for 24 cents a share. Starbucks (SBUX) just said that options-expensing will cost them about 9%.

And finally, General Motors (GM) fell to another 52-week low as Delphi reported that its loss widened by seven-fold. -

Investing Tips

Eddy Elfenbein, November 9th, 2005 at 2:40 pmThe worst investor in the world is the investor who’s down a little, and thinks he or she can make it back by doing something dramatic. This usually involves “doubling-down,” or using a lot of margin, but it usually winds up turning a small loss into a major problem. They delude themselves into thinking that a quick fix—just this one time—can correct the shortfall.

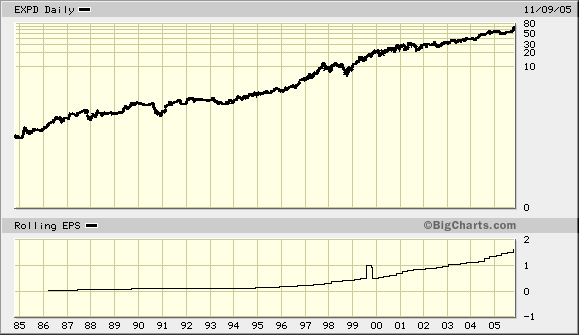

When you’re down in an investment, you can’t let your emotions get the best of you. The first lesson is that the stock doesn’t know you own it or what price you paid. I often hear from investors who own horrible stocks but they refuse to sell because they “don’t want to book a loss.” The stock isn’t aware of your entry point. If it’s a good stock, then keep owning it. If it’s bad, then sell. It really is that simple.

Here’s a chart of Expeditors (EXPD) going back 20 years. You can see that there’s never been a time that was “too late to buy.” And with many lousy stocks, it’s never too early to sell.

Value is a relative. If Google‘s (GOOG) stock were to fall by $100 over the next few months, you’d hear people say that it’s cheap. No, it would be cheaper than it was, but it’d still be wildly overpriced. We all have different yardsticks, but good investors don’t toss theirs aside when it tells them something they don’t want to hear.

The Wall Street Journal reported that a judge has frozen the assets of a hedge fund. The manager “admitted that he had lost a large amount of money in the fund and had deviated from its original investment strategy in order to make up for losses, the SEC said.” Even pros make this mistake.

Just a few weeks ago, we saw Frontier Airlines (FRNT) plunge. I didn’t panic. I didn’t sell. I didn’t “double-down.” Instead, I waited. The storm passed, and we’re back where we were. This is why I love investing. As long as have a good strategy and high-quality stocks, sometimes the best thing to do is nothing at all. -

Oil Exes on Capitol Hill

Eddy Elfenbein, November 9th, 2005 at 12:06 pmCalling these hearings a circus would be an insult to America’s fine carnival-based economic sector.

James Mulla, chairman of ConocoPhillips, said “we are ready open our records” to dispute allegations of price gouging.

ConocoPhillips earned $3.8 billion in the third quarter, an 89% increase over a year earlier. But he said that represents only a 7.7% profit margin for every dollar of sales.

“We do not consider that a windfall,” said Mulva.The committee’s #1 target is Lee Raymond, the CEO of ExxonMobil (XOM).

Raymond said Exxon Mobil’s exploratory and capital spending plans are based on how long it takes to bring new wells, plants or other developments into production. The company’s planners pay no heed to daily or quarterly fluctuations in crude-oil or gasoline prices in deciding when to fund a project, he said.

In 1998, when the Asian economic collapse cut global oil demand and prices dropped to $10.35 a barrel, Exxon Mobil spent $15 billion on new projects, almost twice the company’s net income, he said. This year, the company plans to spend $18 billion, up from $14.9 billion in 2004.

Exxon has raised its spending budget for this year twice in response to soaring costs to rent drilling rigs and purchase steel pipes.

“Someone could argue that in 1998 we invested way too much money,” Raymond said. “My comment is the valley will be coming. And when the valley comes, we’re going to continue to invest.” -

A Dull Market

Eddy Elfenbein, November 9th, 2005 at 10:56 amDear Lord, this is a boring market. This is the S&P 500 for the last four days; up 0.43%, up 0.02%, up 0.22%, down 0.35%, and today we’re up 0.08%.

The Buy List is up 0.32% today. Wake me when something happens. -

Hedge Funds Lost Money in October

Eddy Elfenbein, November 9th, 2005 at 10:34 amOctober was a rotten month for hedge funds:

Hedge funds lost money overall in October, while strategies that trade equities fared the worst as stock prices fell, French business school Edhec said.

Long/short equity hedge funds which buy and short sell — sell a security on the expectation of buying it back cheaper at a later date — lost 2.41 percent on average in October, knocking their year-to-date returns down to 2.13 percent.

That compares with losses of 1.98 percent in October for the MSCI index of world stocks and gains of 7.10 percent in the 10 months since January.

“The month of October was characterised by the poor performance of global stock markets,” Edhec said in a statement.

“Value and small cap stocks performed even worse than the broad stock market. Stock market volatility rose.”

The Chicago Board Options Exchange’s Market Volatility Index, also known as the fear gauge and a benchmark measure of U.S. stock market volatility, hit a five-month peak of 17.19 on October 13, but has since slipped to around 13.

However that rise in volatility allowed one group of hedge funds, those that trade the different components — bond, equity, volatility — of convertible bonds, to make positive returns for the fifth month running.

Convertible bond hedge funds returned 0.24 percent in October although in the year to date they are still down 3.10 percent.

Managed futures funds, those that take directional bets in bond, stock, currency and commodity markets using computer models that give out buy or sell signals, lost 1.49 percent in October and year-to-date are up only 0.15 percent.

Event-driven strategies, which include those that aim to profit from potential takeover deals, were down 1.35 percent but up 1.28 percent for the first 10 months of this year.

“The returns for the month of October confirm the general trend over the last year, where hedge funds have performed below their historical average,” Edhec said. -

Two Stocks Go Private

Eddy Elfenbein, November 9th, 2005 at 9:59 amIn Peter Lynch’s “One Up On Wall Street,” he said that he first heard about La Quinta (LQI), when has asked someone at rival Holiday Inn who their best competitor was. Lynch, who was then the manager of Fidelity Magellan, later found out that La Quinta was covered by just three analysts. His point is that some of his best investment ideas didn’t come from highly paid research analysts. He wrote:

If IBM goes bad and you bought it, the clients and bosses will ask: “What’s wrong with that damn IBM lately?” But if La Quinta Motor Inns goes bad, they’ll ask: “What’s wrong with you?”

That’s very true. Later, Lynch spent a few nights at La Quinta; he liked what he saw and bought the stock. It became a huge winner for the fund. Today, La Quinta announced that it’s going private. The Blackstone Group is buying it out for $3.4 billion.

What’s strange is that this is the second private equity deal in the last two days. Yesterday, Linens N Things (LIN) said it’s being bought out for $1.3 billion. Doesn’t anybody like the stock market anymore? Yes, I know there have been some dubious IPOs in the past, but I’m curious if going private is a trend.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His