Archive for 2005

-

Are We at Bottom Yet?

Eddy Elfenbein, October 13th, 2005 at 10:34 amThe S&P 500 closed yesterday at its lowest level in five months, and today doesn’t look much better. There are only a few earnings reports today. Winnebago (WGO) reported that its profits dropped 19%, but that doesn’t seem to be impacting Thor Industries (THO). Melissa Davis at TheStreet.com has an interesting article on the clash between Biomet (BMET) and Zimmer (ZMH). Both stocks are on our Buy List.

Progressive, the auto-insurer, was upgraded this morning at AG Edwards. The stock hit a new 52-week high today.

Perhaps the most important story, and in many respects, the most expected, China has rejected Treasury Secretary Snow’s pressure for more currency reform. Their finance minister said, “We will not listen to someone else’s conductor when doing what we need to do.”

And finally, here’s a list of most and least fuel efficient cars. -

Krispy Kreme Plunges on No News

Eddy Elfenbein, October 12th, 2005 at 11:23 pmShares in Krispy Kreme (KKD) plunged nearly 13% today on no news. Over 6 million shares were traded. At one point, the stock was down close to 28%. Amidst the carnage, the company issued a press release.

Although as a matter of policy the Company does not comment on unusual market activity or rumors, the Company stated that it is unaware of what has triggered the unusually high trading volume and decline in its stock price today.

Well, I can think of a few reasons for the sell-off. It might have something to do with the earnings warning. Or possibly, the federal investigation. Or perhaps, the SEC investigation.

After all, the company did have to restate earnings for the past four years. It turns out that they overstated their earnings by $22 million. On the other hand, it could the multiple franchisee lawsuits.

Maybe Wall Street was just overreacting. -

Today’s Market

Eddy Elfenbein, October 12th, 2005 at 10:04 pmThe market fell yet again. The fourth quarter has gotten off to an awful start. The S&P 500 fell -0.61% today and our Buy List dropped -0.35%. Thanks to Medtronic (MDT), we were able to beat the market again. I think the company will be able to capitalize off changes in the industry. Glenn Reicin of Morgan Stanley noted that Medtronic is taking advantage of Guidant’s (GDT) problems.

There was some bad news for a certain Attorney General in New York. Mr. Spitzer suffered two defeats today.A U.S. District Court judge ruled that Spitzer had stepped outside his turf with a probe into home-lending practices at major banks, declaring that enforcing bank laws was a matter of federal, not state jurisdiction.

In a separate matter, Spitzer’s office dropped four remaining criminal charges against former Bank of America Corp. broker Theodore Sihpol, whom he had accused of helping a hedge fund trade mutual funds illegally.

In a separate civil case brought by the Securities and Exchange Commission, Sihpol on Wednesday agreed to pay a $200,000 fine and submit to a five-year ban from the securities industry, without admitting or denying any wrongdoing.

A jury in June acquitted Sihpol of 29 counts, including grand larceny. It deadlocked on the four counts, leading Justice James Yates of the New York State Supreme Court to declare a mistrial.

On Wednesday, Spitzer dropped the four remaining counts.

His political opponents said the simultaneous slip-ups could prove a drag as Spitzer, a Democratic, sets his sites on his next political goal — winning the governor’s office in November 2006.After 16 months of raising interest rates, the Federal Reserve is finally impacting long-term rates. The 10-year Treasury bond closed at its highest yield in six months.

-

The Video iPod

Eddy Elfenbein, October 12th, 2005 at 2:22 pmWell, I was wrong. Apple just unveiled its new video iPod.

-

Do We Need Analysts’ Estimates?

Eddy Elfenbein, October 12th, 2005 at 12:22 pmOn days like this, I wonder why we even bother to listen to analysts’ estimates. Advanced Micro Devices (AMD) earned 18 cents a share, creaming the Street’s estimate of eight cents a share, yet the stock falls. Earlier, Alcoa (AA) slashed its earnings forecast, then beat it, and rallied. Apple Computer (AAPL) beat by a penny, and was creamed in after-hours yesterday, but is now trading modestly lower. The big secret announcement is still to come.

On our Buy List, Thor Industries (THO) reported earnings of 58 cents a share, which was one or two cents below estimates, depending on whom you ask. The stock is trading 19 cents lower. Progressive (PGR) said that its third-quarter earnings fell 22% to $1.54 a share, which is a nickel below estimates. And the stock is…higher.

Progressive also had to deal with losses from Katrina and Rita. The company said that its Katrina losses will be about $173.6 million, which is $54.1 million higher than it previously estimated. Progressive also said that Rita will cost $11.9 million.

Our Buy List is mostly down today, although Medtronic (MDT) is rallying thanks to its long-term earnings forecast. Another Minnesota stock, although not on our Buy List, is Fastenal (FAST). The home-improvement store reported very good earnings, beating the Street by four cents a share. The stock is currently up over 7%. -

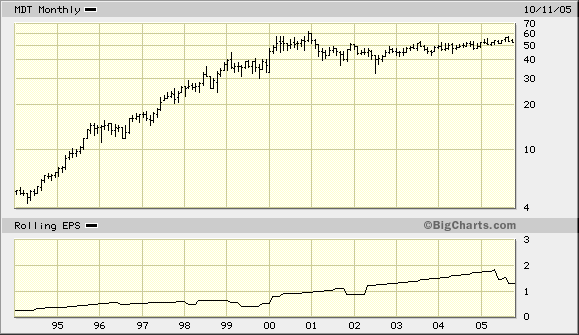

Medtronic Can See for Miles and Miles

Eddy Elfenbein, October 12th, 2005 at 9:01 amMedtronic (MDT), one of the quietest stocks on our Buy List, finally spoke out, and did so loudly. The company raised its earnings forecast for next year, the year after that, and the year after that. In short, Medtronic sees strong earnings through the rest of the Bush administration.

Medical device maker Medtronic Inc. on Tuesday raised its earnings guidance through 2008, citing confidence in its performance and growth prospects, as well as a lower tax rate.

Excluding one-time items and expensing for stock options, the company said it expects fiscal 2006 earnings per share between $2.18 and $2.23, up from its previous outlook of $2.10 to $2.15, and analysts’ consensus profit estimate of $2.16, according to a Thomson Financial poll.

For fiscal 2007, Medtronic raised its earnings per share forecast to a range of $2.45 to $2.55, compared with prior guidance of $2.37 to $2.47. Analysts expect the company to earn $2.46 per share.

Medtronic also boosted its profit outlook for fiscal 2008 to between $2.78 and $2.98 per share, up from its previous estimate of $2.70 to $2.90 per share. Analysts expect a profit of $2.88 per share.

The company said it still expects revenue growth of 14 percent to 16 percent for the fiscal second quarter, as well as sales of $11.1 billion to $11.6 billion for the full year 2006. Analysts forecast revenue of $2.76 billion for the quarter and $11.49 billion for the year.

Medtronic also backed its outlook for revenue of $12.2 billion to $13.3 billion for fiscal 2007, and $14 billion to $16 billion for fiscal 2008. Analysts expect revenue of about $13 billion and $14.92 billion for 2007 and 2008, respectively.First Albany reiterated its strong buy and raised its price target to $66. Deutsche Bank also maintained its buy rating. Despite steadily higher profits, the stock hasn’t done much over the past few years (see chart below). Medtronic is an excellent buy.

-

What to Make of Apple’s Earnings

Eddy Elfenbein, October 11th, 2005 at 11:17 pmFrom the archives of TheStreet.com, here’s the beginning of Troy Wolverton’s story on Apple’s (AAPL) earnings report from six months ago:

Apple sweet earnings report left a bad taste in the mouths of some analysts and investors, sending the company’s shares lower on Thursday.

Apple’s shares were recently off $3.39, or 8.3%, to $37.65.

On Wednesday afternoon, the computer and electronics maker topped Wall Street’s earnings estimates by 10 cents a share and offered better-than-expected guidance for its current quarter.

Despite the blowout numbers, some analysts still found room to quibble.And this is Wolverton’s story from today:

While the company topped bottom-line expectations, its sales fell short of Wall Street’s estimates. More importantly, iPod sales were nowhere near the heady numbers bandied about on Wall Street.

And following the company’s earnings announcement, its stock dropped like a rock. In recent after-hours trading, it was off $5.44, or 10.5%, to $46.15 on Instinet.Reads a bit similar, don’t it? One stock, two earnings reports and the same results. Well, if a stock rallies from the upper-$30’s to the mid-$50’s in the last three months, you can be sure that it’ll be pretty hard to deliver on expectations. That’s why the smart money knew this and starting dumping Apple last week. Except for today, the stock dropped for five straight sessions. To me, the only surprise is that some people were still surprised.

Let’s make one thing perfectly clear: Wall Street is not upset that Apple missed its revenue target. Please. Wall Street couldn’t care less about sales figures unless it’s looking for other excuses. Apple missed its sales forecast by roughly one day’s worth of sales. That’s nothing. What upset the Street is the earnings miss. By miss, I mean that Apple only beat by one penny a share.

After beating by six cents last quarter, and ten cents in the previous two quarters, Wall Street was expecting a massive earnings surprise. (Bear in mind Wolverton’s story above is about a sell-off following a 10-cent surprise). For this quarter, the Street high was 43 cents a share. That’s what Wall Street wanted and it didn’t get it. By any reasonable valuation, Apple is at least 20% overpriced. Should Apple really be going for twice the earnings multiple of Dell (DELL)? I doubt it and the only reason investors paid for it was they wanted a positive news cycle. That’s why you now hear talk of Apple’s revenues shortfall.

My advice is to stay away for now. The good news is that the company gave a positive forecast for this quarter. If the shares pull back enough, we might have a good buying opportunity, but not now.

Addendum: I’m guessing tomorrow’s secret announcement won’t be a video iPod, but expanded storage. -

Today’s Market

Eddy Elfenbein, October 11th, 2005 at 4:57 pmThe market bumped up and down all day long, before closing lower -0.21%. The S&P 500 has closed lower in six of the last seven sessions. This is shaping up to be one of the worst Octobers in years.

Our Buy List dropped -0.88% today. The big loser wasRespironics (RESP) which lost about 5% on no news. Just six of our stocks went up, and nineteen went down. I was surprised to see Froniter Airlines (FRNT) drop below $10 today. I suspect that the shares are continuing to move in the opposite direction of oil. This stock is very cheap now. I can’t imagine it going much lower, but stranger things have happened. -

Women are Better Investors than Men

Eddy Elfenbein, October 11th, 2005 at 1:39 pmOne of my readers asked me about this topic. A few years ago, there was an academic report that showed that women are better investors than men. The key difference wasn’t stock-picking, but risk and trading. Men traded their accounts 45% more than women, and single men traded 67% more than single women. Investing is one of the key activities where doing nothing is often the best move to make.

A study of more than 35,000 discount-brokerage customers by economists at the University of California at Davis found that between 1991 and 1997, women’s portfolios earned, on average, 1.4 percentage points more a year than men’s.

Among single people, the difference was even more pronounced, with single women earning 2.3 percentage points more per year than single men.

Records of investment clubs reveal an even wider performance gap: Through the end of 1998, all-female clubs had an average compounded lifetime return of 23.8 percent a year, compared with just 19.2 percent for all-male clubs, according to the National Association of Investors Corp., which represents about 37,000 clubs nationwide. -

Danaher’s Well-Oiled Machine

Eddy Elfenbein, October 11th, 2005 at 9:33 amDanaher (DHR), one of our Buy List stocks gets the highest rating from Standard & Poor’s.

Danaher, a maker of hand tools and process and environmental controls, is benefiting from steady economic growth, in Standard & Poor’s opinion. We believe that Danaher will continue to expand through a combination of organic growth and acquisitions.

In our view, Danaher has done an excellent job integrating its purchases, expanding acquired-companies’ margins, and generating free cash flow in excess of net income. These funds, in turn, have helped Danaher make additional acquisitions and, in our view, maintain a healthy balance sheet, with a large cash position that offsets most of its long-term debt.

On both a relative and intrinsic basis, we find the shares attractively valued. Given our view of Danaher’s strong operating fundamentals and its compelling valuation metrics, our recommendation is 5 STARS (strong buy).

CORE BUSINESSES. Danaher manufactures and markets industrial and consumer products. It has three reporting segments: professional instrumentation (42% of 2004 sales), industrial technologies (39%), and tools and components (19%).

Businesses in the professional-instrumentation segment offer various products and services to professional and technical customers that are used in connection with the performance of their work. At year-end 2004, professional instrumentation served three lines of business: environmental, electronic test, and medical technology.

The industrial-technologies segment manufactures products and sub-systems that are typically incorporated by original equipment manufacturers (OEMs) into various end products and systems, as well as by customers and systems integrators into production and packaging lines. Many of the businesses also provide services to support these products, including helping customers with integration and installation and ensuring product uptime.

U.S.-EUROPE FOCUS. As of Dec. 31, 2004, the industrial-technologies segment encompassed two strategic lines of business: motion and product identification. It also included three focused niche businesses: power quality, aerospace and defense, and sensors and controls.

The tools-and-components segment is made up of one strategic line of business — mechanics’ hand tools. It also includes four focused niche businesses: Delta Consolidated Industries, Hennessy Industries, Jacobs Chuck Manufacturing, and Jacobs Vehicle Systems.

Sales in 2004 by geographic destination were: United States, 55%; Europe, 29%; Asia, 10%; and other regions, 6%.

LOOMING OVERCAPACITY? We believe that industrial machinery companies should generally fare well in 2005 and 2006, due to anticipated economic growth and a favorable interest rate environment. Longer term, we think that large gluts in global industrial production capacity could hamper earnings growth for certain companies.

We expect continued growth in sales and profits for companies in the S&P Industrial Machinery Index in 2005, albeit at a slower pace than last year. More specifically, as of Sept. 13, S&P estimates operating earnings growth of 18%, vs. 44% in 2004. In addition, so far this year, most manufacturers, with the exception of some of the more commoditized product producers, have demonstrated a modest amount of pricing power via surcharges and select price increases to help cope with rising raw material costs (particularly for steel and copper).

This industry takes in a wide range of industrial concerns that supply the equipment that other companies need to run their manufacturing operations. Longer term, we believe Asia-driven industrial overcapacity could trigger a deflationary cycle. With corporate-profit margins likely to get squeezed in that environment, this could also cause manufacturers to cut back on production, employment levels, and machinery and equipment spending.

TRIMMING COSTS. We think that Danaher, with its diverse product mix and geographic diversification, can continue to grow faster than the industrial machinery industry as a whole.

After a sales gain of 30% in 2004, we expect revenue growth to slow to 18% in 2005 and 14% in 2006. This will be driven by a combination of U.S. and foreign economic growth, acquisitions made in 2004 and 2005, and acquisitions that we anticipate for 2005 and 2006.

We see 2005 and 2006 margins benefiting from employment reductions and other streamlining activities, partly offset by narrower margins at some acquired businesses.

HEALTHY MARGINS. For the longer term, we look for sales increases to be spurred by internal growth (5% to 7% a year), supplemented by acquisitions. We anticipate a steady flow of new and enhanced products, as well as greater sales of traditional tool lines, to aid comparisons. We expect margins to widen over time, as Danaher consolidates acquisitions and benefits from higher capacity utilization, productivity gains, and cost-cutting efforts. Management has demonstrated its ability to acquire and integrate companies while enhancing EPS and cash-flow growth, in our view.

Based on S&P Core Earnings methodology, we believe the quality of Danaher’s earnings is high. After a series of adjustments made to its net income from continuing operations and before extraordinary items (based on generally accepted accounting principles) to conform to S&P Core Earnings methodology, Danaher’s 2004 net income per share of $2.30 would be reduced to $2.20, a 4% reduction. For 2005, we project S&P Core EPS of $2.75, only a 1.1% reduction from our operating EPS estimate of $2.78.

The reductions reflect option expense of 4 cents, offset by a one cent net pension credit. For 2006, we project S&P Core EPS of $3.14, equal to our operating EPS forecast, as our 2006 model includes option expenses and assumes no other adjustments.

STOCK AT A PREMIUM. The company has been able to consistently expand net income, EPS, and cash flow. Given what we see as Danaher’s sound balance sheet (long-term debt is under 30% of capitalization), as well as our expectation for strong cash flow growth in coming years, we think the company could raise its 8 cents per share annual cash dividend in 2006.

Based on several valuation measures, the stock is at a premium to that of some peers. We believe this reflects Danaher’s wider net margins and faster growth. The quality of earnings appears high to us, as we expect free cash flow in 2005 to exceed net income. Plus, as noted, S&P Core Earnings adjustments are likely to reduce expected 2005 operating EPS by only about 1%.

Based on peer and historical p-e multiple comparisons, we apply a p-e multiple of 21 times to our 2006 EPS estimate of $3.14 to arrive at a price of $66 for Danaher shares. Our discounted cash-flow model calculates intrinsic value of $67. Based on a combination of our p-e multiple and DCF analyses, our 12-month target price is $66.

HURT BY INFLEXIBILITY? We view the stock as attractively valued at a recent level of 17 times our 2006 EPS estimate, a p-e-to-growth (PEG) ratio of about 1.1, and at about a 20% discount to our target price of $66.

We’re concerned about some of Danaher’s corporate-governance practices, particularly its classified board of directors with its staggered terms, that may allow certain policies to be entrenched longer, despite shareholders’ desire to change them. On a positive note, the board is controlled by a majority of independent outsiders.

Potential risks to our investment recommendation and target price, in our view, include: slowing demand for Danaher’s products, and unfavorable changes in foreign-exchange rates. Also, Danaher is dependent upon acquisitions and successful integration of acquisitions for its growth in revenues and earnings. Failure to maintain its growth rate and track record of success could result in a lower equity valuation, in our view.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His