Archive for 2005

-

Europe’s Economy

Eddy Elfenbein, September 28th, 2005 at 1:17 pmDaimler Chrysler just announced that it will cut 8,500 jobs in Germany over the next year.

The world’s fifth-biggest carmaker said the move would cost 950 million euros, to be offset by extraordinary income and efficiency gains.

It reiterated its forecast for a slight rise in 2005 operating profit excluding charges to restructure its Smart minicar business.

The Mercedes division employed around 105,000 staff at the end of last year, of which some 94,000 were in Germany.

“These headcount reductions are indispensable. They will contribute to significant improvements in the competitiveness of Mercedes-Benz through an increase in productivity,” it said in a statement. “The measures will also contribute to the sustained safeguarding of production (in) Germany.”So if all lost for Europe’s economy? Matthew Lynn says, “Don’t Blame Oil for Europe’s Economic Slowdown.”

If oil is so deadly to Europe’s economic prospects, then why is it that Japan appears to be emerging from a recession, when Europe is still stuck with miserable growth? Japan isn’t exactly famous for its oil wells.

Likewise, the U.S. Because taxes on pump prices are so much lower there than they are in Europe, the impact that an increase in oil prices has on consumers is proportionately much greater. And yet, U.S. growth rates remain significantly higher than Europe’s. The U.S. economy expanded an annual 3.3 percent in the second quarter, compared with 1.1 percent for the euro area.Lynn concludes:

The reasons why Europe’s economy is growing so slowly are familiar: high taxes, dysfunctional labor markets, and restrictive monetary policy. The first step toward fixing those is honesty. Right now, that appears to be a commodity in shorter supply than oil.

-

Fair Isaac Hits New All-Time High

Eddy Elfenbein, September 28th, 2005 at 12:55 pmFair Isaac finally hit a new all-time high today. It took nearly two years for the company to break into record territory.

J.P. Morgan upgraded Fair Isaac today to overweight from neutral. I’m not a big fan of following analyst upgrades or downgrades, but this one is nice to see. Fair Isaac has a very strong business. I especially like the fact that its gross margins come to about 70% of sales. That’s the sign of a well-run business.

The company will report its fiscal fourth-quarter earnings in late-October. The current estimate is for 49 cents a share. This means that although FIC’s stock is roughly where it was two years ago, its profits are nearly 30% higher. This is a solid stock to own.

You can see my complete Buy List here.

-

Warren Buffett’s Shareholder Letters

Eddy Elfenbein, September 27th, 2005 at 8:35 pmIf you’re new to the world of investing, I recommend reading some of Warren Buffett’s annual shareholder letters. You can find a complete collection here.

The letters have a folksy style and Buffett always makes a good point. This is the best way to get a nice summary of Buffett’s investing philosophy, and you can see how little it has changed over the years. -

Google Watch

Eddy Elfenbein, September 27th, 2005 at 11:38 amIf you go to Google today, you’ll see that today is the search engine’s 7th birthday. Happy Birthday!!

Wait a minute! Didn’t they just celebrate their 7th birthday three weeks ago? It turns out, Google has a few birthdays. Search Engine Watch is on the case. -

Frontier Airlines

Eddy Elfenbein, September 27th, 2005 at 10:01 amOne of the best ways to look for a good stock to buy is to find the most-unloved industry, and pick out that sector’s best stock. It’s no secret that airlines stocks have performed horribly. Make no mistake, the industry is in rough shape, but there are good stocks out there. For example, I think the industry’s woes have given us a good opportunity in Frontier Airlines. The stock is now below $10.

Frontier has a lot going for it. For one, it’s an airline that’s not in bankruptcy. That right there is a big advantage over it competitors. Frontier is small regional airline based in Denver with a solid balance sheet. The company has switched to using all Airbuses. Frontier has slowly expanded its market share.

The airline is popular with its passengers. The company is ranked near the top in customer satisfaction surveys. The downside is rising fuel costs. Frontier is one of the least efficient airlines in handling higher fuel prices. The company should post third-quarter profits in late October. Frontier has posted better-than-expected earnings for the last two quarters.

Frontier was originally based in Denver, one of United’s hubs, to piggyback on their business. Now that United is doing so poorly, Frontier can actually take some of United’s core business.

Today, the Wall Street Journal highlights Frontier’s growing service to Mexico. Two years ago, Frontier flew 33,000 passengers to Mexico. Last year, it flew nearly 100,000, and this year it will fly over 200,000 people to Mexico. -

GM’s Debt Downgraded Again

Eddy Elfenbein, September 27th, 2005 at 9:34 amGM’s outlook is actually getting worse. I didn’t think that could even happen. Its debt is already rated as “junk.” Today, Fitch lowered its rating to even junkier junk (double-B). The Delphi story is going to end soon and it’s not going to end well.

Here’s a short history of GM’s debt rating. It wasn’t that long ago that GM was one of the bluest blue chips on Wall Street. Last quarter, GM lost over $250 million, and over $1 billion in the quarter before that. -

SEC Investigating Taser

Eddy Elfenbein, September 27th, 2005 at 9:19 amThe SEC said it’s expanding its investigation into Taser.

The U.S. Securities and Exchange Commission has now upgraded its probe to a formal investigation, allowing it to subpoena documents. The SEC had opened an informal probe of the company over statements about the safety of its stun guns and a distribution deal struck in December 2004.

Taser also said it understands the SEC is looking into the possible unauthorized acquisition of material nonpublic information by individuals outside the company in an effort to manipulate Taser’s stock price.

Taser shares were down 8.6 percent to $6.68 Tuesday in premarket trading on the Inet electronic brokerage system.

Taser has stood by the safety of its weapons, saying the stun guns have never been named as the primary cause of death when suspects were in custody.

Taser Chief Executive Rick Smith said in a statement that he hoped the SEC probe would address “all pertinent issues,” including what he said was data indicating that “there may be a large, improper, naked short position” in the stock.The stock is down sharply in the pre-market. The stock is down over 75% since the beginning of the year. However, Rich Smith, at the Motley Fool is still bullish on Taser.

-

Citi Ungrouped

Eddy Elfenbein, September 26th, 2005 at 11:50 amTom Brown has a “modest proposal” to increase Citigroup’s value. Break it up.

I should say up front I was never a big fan of the supermarket strategy that was behind the 1998 creation of the Citi monolith in the first place. Huge scale doesn’t count for much in financial services, for one thing. And in financial services, smaller, focused players tend to outcompete large, diversified ones. That’s why, for instance, community banks reliably take deposit market share from the large national banks. And it’s why the monoline card industry was able to drive all but a handful of players out of the card business. The idea behind Citi was flawed from the beginning—which is one reason the stock’s P/E has eroded steadily for the past seven years.

By contrast, a breakup of the company would be a great strategic move and profound gesture to shareholders and competitors. In our view, a leaner, more focused group of legacy Citi businesses would emerge and be vastly preferable to the current bureaucratic Byzantium. The units would be much more effective competitors as smaller, focused players than they are now. So management can and should admit the obvious: the company is so big that, strictly by the law of large numbers, it can no longer generate meaningful company-wide organic growth. To put matters in perspective, if the company were to grow by 9% annually, net income would have to rise by $1.6 billion in 2006, which is roughly the equivalent of creating a brand-new BB&T. Incremental acquisitions, meanwhile, would have to be huge to make a meaningful difference, and would be tough to execute well (as management has publicly conceded). -

Reuters Vs. Bloomberg

Eddy Elfenbein, September 26th, 2005 at 8:52 amThe same speech on the same day is covered by different journalists.

Bloomberg:U.S.’s Bernanke Is ‘Pretty Optimistic’ About Economy

Energy prices risk to US economy—Bernanke

-

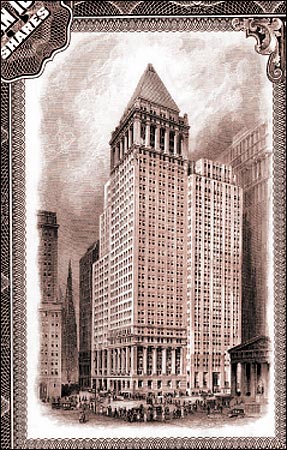

Wall Street Art

Eddy Elfenbein, September 25th, 2005 at 5:58 pmFour years ago, the stock exchange repealed its requirement for engravings on stock certificates. To some poeple, this is a lost art.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His