Archive for February, 2006

-

Expensing Stock Options

Eddy Elfenbein, February 14th, 2006 at 12:44 pmYou may to check out Barron’s Online this week. The site is free-for-all for a limited time. Andrew Bary has a good article on the impact of expensing stock options, especially in the tech sector:

Tech outfits tend to be generous dispersers of stock options. At Intel and Cisco, the value of these are expected to equal about 13% of profits this year, versus 3% at Pfizer (PFE) and less than 1% at General Electric (GE).

Cisco reported “pro-forma” profits, excluding option expense, of 26 cents a share for its quarter ended Jan. 28, and of 22 cents, with option expense. Some investors and analysts, hoping for earnings that would justify a high stock price, still focus on Cisco’s pro-forma results.

Nonetheless, says David Bianco, the chief equity strategist at UBS. “There are not too many investors out there who think stock options aren’t an expense.” Option grants have been falling in recent years — Cisco, however, issued more in its latest fiscal year than in the prior one — and Bianco wonders how much further they’ll slip now that expensing is mandatory. He estimates that options will cut profits for the S&P 500 by about $2 this year, off an earnings base of around $80. That’s a hit of roughly 2.5%. The hit in tech will be an estimated 15%. -

Random Market Stat of the Day

Eddy Elfenbein, February 14th, 2006 at 11:36 amIt’s hard to overstate the impact of long-term interest rates on equity prices. As long as long-term yields head lower, the stock market does well. But when rates rise, it’s like running into the wind.

Since 1962, there have been over 2,300 weeks of trading. The yield on the 10-year Treasury bond has fallen for 1,060 of those weeks. During those weeks, the S&P 500 is up a combined 6,187%, which is about 22.5% on an annualized basis.

The 10-year yield was unchanged over 129 weeks. During that time, the S&P 500 was up just 4%, or 1.6% annualized.

And for the 1,112 weeks of rising yields, the S&P 500 was down 72.3%, or 5.8% a year. When you separate out the data like this, you can really see the impact that bond yields have on the market.

Perhaps the most important fundamental aspect of this market is that long-term interest rates have been remarkably flat for so long. For the last two-and-a-half years, long-term yields have traded in a band between 3.68% and 4.87%. Over 75% of the time, the yield has been between 4.0% and 4.5%.

In other words, stocks aren’t getting any help from bonds. -

Expeditors Earnings

Eddy Elfenbein, February 14th, 2006 at 9:50 amThis morning, Expeditors (EXPD) reported fourth-quarter earnings of 72 cents a share. However, that included a tax benefit of 19 cents a share. Discounting that, Expeditors earned 51 cents a share, two cents more than Wall Street’s estimates. Net sales increased 23%.

“This quarter has to be viewed as a fitting end to what was an outstanding year,” said Peter J. Rose, Chairman and Chief Executive Officer. “Our operating income was 27.6% of net revenue during the fourth quarter of 2004, but this expanded to an amazing 31.3% in 2005 as we were able to handle a significant increase in freight without having to add a commensurate amount of expense. This positive leverage was a result of our ongoing process and productivity initiatives. By every measure, our people did a superb job executing in what was really a very difficult environment: simply put, there was just a bunch of freight out there,” continued Rose.

“Air freight volumes were strong during the fourth quarter and ocean freight, which was a little subdued in November 2005 compared with October, came through very strong in December,” Rose said. “We think that a 39% operating income increase off of our already sizeable base is extremely indicative of just how well we executed during the busiest time of the year. We just finished recording our second straight one billion dollar quarter and this put us over the top to enjoy our first year with over one billion dollars in net revenue. More than empty talk, these are real measures of progress,” Rose concluded. -

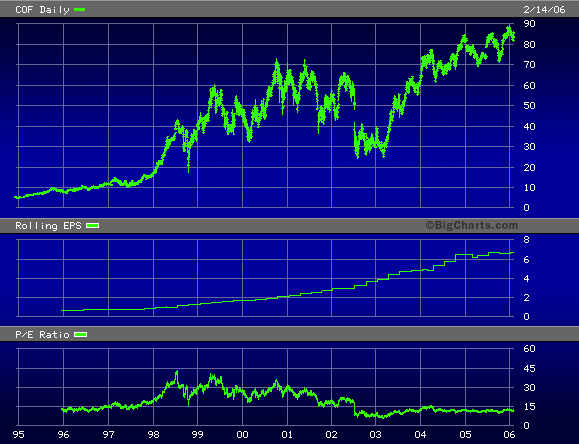

Obscenely Profitable Stock

Eddy Elfenbein, February 14th, 2006 at 1:00 amIn my continuing series, “here’s an obscenely profitable stock that I don’t own,” I bring you Capital One Financial (COF).

They’re one of the major credit card companies (David Spade, “what’s in your wallet?”). The company is massively profitable.

Capital One uses a combination of heavy mass marketing and pinpoint datamining. They know exactly who to lend to and how much. Despite their aggressive marketing, the loan portfolio has actually been fairly conservative.

I often hear people complain about junk mail from credit card companies. The companies do it for a highly sophisticated and complex reason. It works.

Capital One grew so quickly that the market assumed something had to be wrong. Four years ago, banking regulators demanded tighter controls and the stock cracked. But the company stood by its loan portfolio, and the results speak for themselves.

Here’s their earnings-per-share for the past few years: $0.77, $0.93, $1.32, $1.72, $2.24, $2.91, $3.93, $4.92, $6.21 and $6.73. Constant growth.

The company forecast earnings this year of $7.40 to $7.80 a share, which translates to growth of 10% to 16%. It also means that at today’s price, Capital One is going for 11.0 to 11.6 times this year’s earnings. That’s very cheap, and if that isn’t enough, you also get a teeny dividend.

One of my worries, however, is that the company recently completed a major merger with Hibernia bank. I always get nervous about growth-through-acquisition strategies.

-

The Market Now Expects At Least One More Rate Hike

Eddy Elfenbein, February 13th, 2006 at 4:08 pmHere’s a major change in sentiment: One month ago, the futures market indicated that there was a 56% chance that the Fed would raise rates on its March 28 meeting, and a 0% chance of a rate hike in May. Today, the futures indicate a 94% chance of a rate hike in March, and a 62% chance of another rate hike in May.

-

This Week’s Earnings

Eddy Elfenbein, February 13th, 2006 at 2:47 pmExpeditors International (EXPD) will release its fourth-quarter earnings tomorrow morning. The current consensus estimate is for 51 cents a share. Last year, Expeditors earned 39 cents a share. This is a great stock, although it’s getting a bit rich for me.

Dell (DELL) will release its fourth-quarter earnings on Thursday.

For the record, Dell originally said that its third-quarter earnings would come in at 39 to 41 cents a share, on sales of $14.1 to $14.5 billion. However, the results were 39 cents a share on sales of $13.9 billion. That was the “miss” that freaked everyone out.

For this quarter, Dell expects earnings of 40 to 42 cents a share on sales of $14.6 to $15 billion. Wall Street’s original forecast was for 42 cents on $15 billion.

If Dell earns 43 cents a share, I will never listen to another Wall Street analyst for the rest of my life. -

Is the Oil Crises Over?

Eddy Elfenbein, February 13th, 2006 at 1:52 pmYes, according to Matthew Lynn at Bloomberg:

Forget that order for a funny- looking electric car. Take the solar panels off the roof. Don’t worry about hoarding tinned food for the long economic slump that is about to engulf the world.

Why? Because the oil crisis we were all concerned about less than a year ago is quietly going away.

The laws of supply and demand are starting to restore market calm. They suggest that although oil isn’t about to get really cheap, talk of $100 a barrel can now be put to rest.

That will give an extra leg to economic growth and stop central bankers from fretting about inflation.

“The fundamentals are starting to quietly reassert themselves,” Simon Hayley, senior international economist at Capital Economics Ltd. in London, said in a telephone interview.Oil is down to $61.15 a barrel today.

-

Venture Capitalist Turns Romance Novelist

Eddy Elfenbein, February 13th, 2006 at 1:33 pmTom Perkins, one of the legendary venture capitalists of Silicon Valley, has a new book out. But it’s not what you think.

The new book, Sex and the Single Zillionaire, is actually a romance novel and it sounds like the kind of thing Danielle Steel would write. Of course, that’s hardly a coincidence considering that Ms. Steel is not only his editor, but his ex-wife.

Yah Zhao at the Harvard Crimson outlines the plot:The protagonist, Steven Hudson, is a powerful N.Y. investment banker. Like Perkins, Steven receives a letter asking him to be the star in a reality television show called “Trophy Bride” where young, female 20-somethings compete to marry a “zillionaire.” After repeated assertions about the absurdity of the offer, Steven ends up agreeing to do the show—partially because he is lonely after his wife’s passing and partially because he falls in love with the producer of the show, Jessie Jones.

After 280 pages of trials and tribulations—including Steven being conned by a girl pretending to be on the U.S. Olympic ski team, being pursued by a nymphomaniac, and pacifying his extremely conservative colleagues who were outraged by his “sex frolic”—the obligatory happy ending is duly set down. -

Gurgle

Eddy Elfenbein, February 13th, 2006 at 11:31 amMusn’t gloat.

Ther media is turning around Google (GOOG) is a big way. Barron’s featured Google on its front page this weekend.To get a sense of what might happen to the stock, we gave one über-bull’s 2006 revenue estimate for Google a 20% haircut, trimmed his projected expenses by 5% (but no further, because bulls greatly underestimate Google’s costs), deducted stock-based compensation and, generously, gave the company credit for the considerable interest income on its cash. The result: Earnings would be 30% lower than the bull’s projection, at $6.28 a share. If the stock were to maintain its current multiple of 41 on those lowered earnings, it would be worth $257. It’s more likely the multiple would shrink to as low as 30, in line with the slower growth. That would make the stock worth $188, versus its recent $360.

Though this exercise is less than scientific, it clearly demonstrates two things. First, Google’s business has tremendous leverage — changes in revenue, in either direction, have outsized impacts on the bottom line. That’s the result of high profit margins: 88% of net revenue and 58% of gross revenue. Second, the exercise provides a glimpse of the risk posed by a lofty stock multiple.

“Google reminds me very much of what went on in 1999 and 2000,” says Fred Hickey, editor of the well-regarded High-Tech Strategist newsletter and a member of the Barron’s Roundtable. “The valuation is insane, relative to what they do.”The stock opened at $344 today. The AP is reporting that analysts are standing behind Google:

“Google remains our No. 1 buy recommendation in the Internet sector, and our price target remains $490,” said Citigroup analyst Mark Mahaney, who added the March 2 analyst day might be another catalyst for the lofty stock.

Sasa Zorovic, an analyst with Oppenheimer, said the recent stock weakness since Google reported disappointing fourth-quarter earnings might even provide a buying opportunity. The stock has fallen 20 percent since reported quarterly numbers on Jan. 31.

“We continue to believe the online advertising industry remains a powerful growth story and that Google enjoys a market-leading position, gaining share from the competition in recent months,” Zorovic said in a report. “We believe the recent pullback provides a buying opportunity, and we reiterate our ‘Buy’ rating and $540 price target.” -

BlackRock shares jump amid talk of Merrill deal

Eddy Elfenbein, February 13th, 2006 at 11:28 amMerrill launches a pre-emptive strike:

Shares of BlackRock Inc. shot higher on Monday in thin, pre-market trading amid speculation the money management firm was involved in a deal with Merrill Lynch & Co.

BlackRock shares rose almost 14 percent to $149.80 on the Inet electronic brokerage.

Both The New York Times and The Wall Street Journal, citing people familiar with the discussions, reported in Monday editions that Merrill Lynch would acquire a large stake in BlackRock, known for managing fixed income. The Journal valued the transaction at about $8 billion.

Megan Frank, a spokeswoman for Merrill Lynch, said the company can’t confirm or deny market rumors. A call to BlackRock seeking comment was not immediately returned.

A deal would create a company with $1 trillion in assets under management, the most of any publicly traded company.

A BlackRock deal would be more strategically compelling than the alleged Merrill deal with Morgan Stanley, Buckingham Research said in a note to investors.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His