Archive for March, 2006

-

Another New High

Eddy Elfenbein, March 16th, 2006 at 1:34 pmToday is another good day for the market. New highs abound! The morning got off on the right foot when the government reported that inflation was tame last month. Inflation was up just 0.1% last month, and the “core rate,” which excludes volatile food and energy prices was also up just 0.1%. You wouldn’t know this by listening to some corners, but the core rate of inflation has been trending slightly lower over the past year.

The latest word is that Bernanke & Co. will raise rates two more time, and then cool it. Our Buy List is having a decent day. Danaher (DHR) is up for the sixth straight day. This is such a cool little company. The stock is at a new all-time high. I’m also happy to see Bed Beth & Beyond (BBBY) hold onto its gains.

Here’s what Jon Markman had to say about Brown & Brown (BRO) a few weeks ago:The company is scheduled to announce its 2006 first-quarter results in the third week of April, and I think they will show they’re on track to earn $1.28 in 2006, and $1.48 in 2007. At a much-deserved premium price/earnings multiple of 26, that would peg the stock for a move to around $38 over the next 12 months, which would be a 24% move.

The stock has a tendency to range trade for extended periods, and then move up briskly in the fourth quarter of each year. If you’re interested in starting a new position, you might consider deploying half of your allocation now between $28 and $30, and deploying another half toward the end of the summer, when it could very well be around the same price before its usual end-of-the-year bump up.

BRO is not totally without risk. It is highly exposed to the hurricane prone Gulf of Mexico region, with 40% of its revenues coming from Florida. Brown’s ability to continually acquire other insurance companies could be severely hindered if they have to write checks to settle customer claims from another brutal hurricane season instead. Yet as we all know by now, big short-term losses only mean one thing to insurance companies: They get to raise rates, keeping the cash machine flowing.

There’s one curiosity with BRO that I need to note, however. You have to wonder how a company with nearly $1 billion in revenues could have such a strange web site (www.bbinsurance.com). It’s very 1998, and marked by a penchant for zoo animals. Quotes at the top state gems like, “Lemurs eat an entirely vegetarian diet.” If anyone knows what this has to do with selling insurance, let me know.He’s right. It is a strange site.

Fair Isaac (FIC) is rebounding some. Yesterday, the stock got as low as $36.36. It’s currently just a tad above $40. I think the panic has passed. On Tuesday and Wednesday the stock generated volume of 10 million shares, equal to what it did over the previous month. Now I see why the brokers have been making so much dough.

Next Tuesday, we’ll get earnings reports from Biomet (BMET) and FactSet Research Systems (FDS).

Outside our Buy List, I’m still having a hard time believing Intel (INTC) is below $20 a share. I’m not wild about the stock. I’ve always thought it was a bit overrated, but the stock is where it was nine years ago. -

Big Profits On Wall Street

Eddy Elfenbein, March 16th, 2006 at 10:34 amHeavens to Murgatroyd! Wall Streetistan is swimming in profits. Thanks to heavy trading volume and a flurry of M&A activity, Wall Street firms are reporting ginormous earnings. The profits are so high, even Wall Street itself is surprised.

First up was Goldman Sachs (GS) which floored the market on Tuesday. Goldman’s net income soar 64% to $2.48 billion. No one saw that coming. Funny thing, one of the little ironies of Wall Street is that the investment houses are the hardest businesses to read. So whatever it is Goldman does behind those doors, they’re doing a heck of a lot of it.

Put it this way, Goldman made more coin last quarter than it did during all of 2002. The company’s asset management business (think, hedge funds) doubled. Goldman’s crushed Wall Street’s forecast by 54%. This was their third straight record quarter, and the company raised its dividend by 40%.

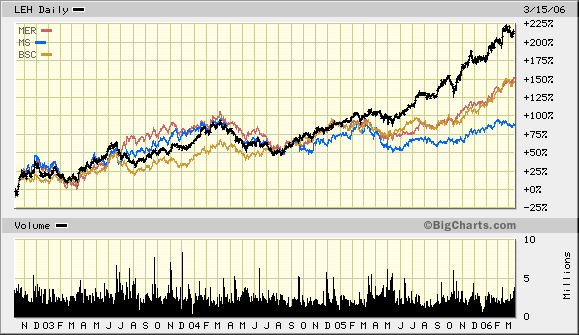

Yesterday, Lehman Brothers (LEH) followed up with another blowout report. Actually, I feel a little sorry for them since Goldman had set the bar so high. Lehman had record earnings of $1.09 billion. Excluding an accounting charge, earning-per-share came in at $3.50, a 26.8% increase over last year’s first quarter. That easily topped Wall Street’s expectation of $3.17 a share. Although, the stock sold off a little at first, so I’m not exactly sure what the real expectations were.

For the past several years, Lehman has been the shining star of the big houses. The company is traditionally known as a bond house, but Richard Fuld, the CEO, has worked to diversify their business. Plus, he’s probably noticed that the yield curve doesn’t exactly curve anymore.

Then Bear Stearns (BSC) said this morning that it’s also making some serious cash. Wall Street was looking for $2.95 a share. BA! Bear Stearns made a cool $3.54. Profits jumped 36% to $514.2 million.

But not everything is great for Bear this morning. There’s also the little issue of the $250 million fine for fraudulent market timing and late trading of mutual funds.According to NYSE Regulation, the exchange’s regulatory arm, Bear Stearns engaged in a pattern of deceptive market timing and late trading of fund shares from 1999 through 2003. The trades were designed to take advantage of the time between the markets’ closing and the new share values posted by mutual fund companies.

Bear Stearns settled the case without admitting or denying the charges. The company will pay $90 million in fines and relinquish $160 million in profits and interest.Morgan Stanley (MS) will report is earnings next week, and Merrill Lynch (MER) will follow in April.

-

Buy List Update

Eddy Elfenbein, March 16th, 2006 at 5:58 amNow that we’re winding up the first quarter, I thought this would be a good time to look at how well our Buy List has done.

If you’re not familiar with our Buy List, this is a list of 20 stocks that I select each year and start tracking on January 1. The hitch is that the list does not change all year. So I’m stuck with the good, the bad and the ugly. I do this to show investors that you don’t need to do a lot of trading to be a successful investor.

So how well are we doing? The good news is that we’re up slightly for the year. The bad news is that we’re trailing the market by nearly 2%.

Through yesterday’s close, our 20 stocks are up an average of 2.46% (not including dividends). The S&P 500 is up 4.38%. Our daily volatility is 8.7% greater than the market.

We were slightly ahead of the market through mid-February, but this latest surge caught our stocks a bit flat-footed.

Here’s how our stocks have done:Ticker Stock Profit EXPD Expeditors International 23.55% DHR Danaher 12.59% VAR Varian Medical Systems 12.59% SEIC SEI Investments 9.38% GDW Golden West Financial 8.56% BRO Brown & Brown 5.86% DCI Donaldson 4.78% HD Home Depot 4.40% BBBY Bed Bath & Beyond 2.63% SYY Sysco 0.00% BMET Biomet -0.08% RESP Respironics -0.27% AFL AFLAC -0.37% FDS FactSet Research Systems -1.21% DELL Dell -1.30% FISV Fiserv -1.92% HDI Harley-Davidson -2.91% MDT Medtronic -7.68% UNH UnitedHealth Group -7.72% FIC Fair Isaac -11.66% Fair Isaac’s (FIC) troubles started just two days ago, but Medtronic (MDT) and UnitedHealth (UNH) come in at #18 and #19. In fact, there’s a good deal of space between them and #17. So much for safety with size! MDT and UNH are two of the largest stocks on the Buy List.

While I’m a very competitive person, I’m not ready to panic just yet over trailing the S&P 500. Given the short time period, our performance to date is completely normal.

I still see lots of great bargains on the list. Dell (DELL) below $30 is a good buy. I’m in shock that Bed Bath and Beyond (BBBY) cracked $37 yesterday. Fiserv (FISV) and Harley-Davidson (HDI) are both good buys. The only stock I’m leery of is our best-performing one. Expeditors (EXPD) is a great company, but it looks a wee bit rich at this price.

As always, my advice is to buy and hold great companies. Don’t worry about oil or moving averages or the Federal Reserve or whatever else we’re being told to worry about.

Worry about your friends and family. Our Buy List stocks are terrific companies. The great Benjamin Graham said that the market acts like a voting machine in the short term, but a weighing machine in the long term. The voice of reason is quiet, yet persistent. -

See What $1 Million Looks Like

Eddy Elfenbein, March 15th, 2006 at 4:54 pmAll 899 square feet. One bedroom and one-and-a-half baths.

On a related note, Google (GOOG) closed at $344.50 today. -

Sherron Watkins Is No Whistleblower

Eddy Elfenbein, March 15th, 2006 at 2:24 pmSharron Watkins is ready to take the stand at today’s Enron trial. She’s become a mini-celebrity due to her role as the brave whistleblower inside Enron. Watkins was even named one of Time’s “Persons of the Year,” along with two other female whistleblowers. We even had to endure articles asking us if women are really more honest than men.

Unlike the other two women (Cynthia Cooper and Coleen Rowley), Sherron Watkins is no whistleblower. All she did was write an anonymous letter to Ken Lay. She didn’t go to the media or regulators, and she never followed up.

You can read the memo here. In it, you can see that she’s not only not a whistleblower, she was actually concerned that others might blow the whistle. I’ll politely skip over the issue of Time, owned by what was once known as AOL Time Warner, pointing out the problems of creative accounting.

Dan Ackman sums up what Watkins really did:A whistle-blower, literally speaking, is someone who spots a criminal robbing a bank and blows a whistle, alerting the police. That’s not Sherron Watkins.

What the Enron vice president did was write a memo to the bank robber, suggesting he stop robbing the bank and offering ways to avoid getting caught. Then she met with the robber, who said he didn’t believe he was robbing the bank, but said he’d investigate to find out for sure. Then, for all we know, Watkins did nothing, and her memo was not made public until congressional investigators released it six weeks after Enron filed for bankruptcy.Don’t feel too bad for her. She already had her $500,000 book deal.

-

Cyclical Index Follow-up

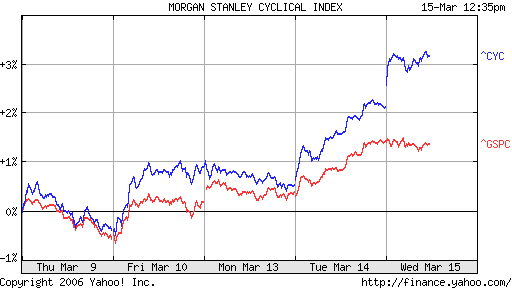

Eddy Elfenbein, March 15th, 2006 at 12:33 pmI wrote too soon about the Morgan Stanley Cyclical Index (^CYC) (see here). The cyclicals are having a huge day compared with the rest of the market. The CYC is up 1.04% while the S&P 500 is down 0.05%.

-

Harley Grows Up

Eddy Elfenbein, March 15th, 2006 at 11:22 am

Legendary hogmaker, Harley-Davidson (HDI), is facing a mid-life crisis. How do you market a plaything for older white guys to a mass audience?As the Baby Boomers who transformed Harley’s rumbling, lumbering bikes from countercultural totems into American icons enter their senior years — the leading edge of the generation is turning 60 this year — they’re increasingly in the market for knee and hip replacements (Biomet!), not Harley’s notoriously bone-shaking bikes.

That’s forcing the Milwaukee, Wisconsin-based company to scramble to find new customers among women, blacks and Hispanics — groups that have not been traditional Harley-Davidson riders.

The quest has involved the development and rollout of new products, like the 883 Sportster Low, built for smaller, lighter riders, and new marketing efforts, like Harley’s TV ad campaign during the NCAA tournament this spring.

And the effort is showing some signs of success. Female ridership has quintupled in recent years. Today, women like Janeen Wingo, a 33-year-old resident of Calumet City, Illinois, who bought a Harley-Davidson 1200 Sportster last summer, account for 1 in 10 of the company’s sales — up from 1 in 50 just 15 years ago.Here are Harley’s sales and earnings for the past ten years:

Year………..Sales (mil)………EPS

1996……….$1531.2…………$0.47

1997……….$1762.5…………$0.57

1998……….$2064.0…………$0.69

1999……….$2452.9…………$0.87

2000……….$2906.4…………$1.13

2001……….$3363.4…………$1.43

2002……….$4091.0…………$1.90

2003……….$4624.3…………$2.50

2004……….$5015.2…………$3.00

2005……….$5342.2…………$3.41

Not a bad trend. Wall Street is expecting 2006 EPS of $3.72 on sales of $5.6 billion. The stock is currently going for about 13 times this year’s estimate. -

Fair Isaac Roundup

Eddy Elfenbein, March 15th, 2006 at 10:25 amYesterday, shares of Fair Isaac (FIC) were knocked down on the news that three credit-reporting companies are creating a rival credit scoring system to Fair Isaac’s FICO. So far, I’m far from convinced that this new system is a serious threat to Fair Isaac.

The Wall Street Journal quotes Fair Isaac’s CEO, Thomas Grudnowski, who summed up the situation nicely:The new VantageScore system developed by the three bureaus competes with the FICO score system developed by market leader Fair Isaac Corp. of Minneapolis, whose proprietary credit-scoring system is used by 80% of the 50 largest banks in the U.S., according to Thomas Grudnowski, chief executive officer of Fair Isaac. About 75% of mortgage-loan originators use Fair Isaac’s FICO scores in their underwriting process, according to Doug Duncan, chief economist of the Mortgage Bankers Association.

“Because of our low price and high quality, there has got to be a burning platform for customers who want to switch, because there is going to be financial risk,” Mr. Grudnowski said.

Financial institutions and mortgage companies use credit scores, which are derived from information reported to local and national credit-reporting agencies, to determine which loan applicants are good risks. Your payment history, amount of debt owed, and how long you’ve used credit are some of the factors included in a credit score. Each of the three national reporting agencies currently markets its own credit score to lenders and consumers, as does Fair Isaac, which sells them directly to consumers at myfico.com. The credit bureaus also sell the FICO scores to consumers.

Fair Isaac’s system uses a scale from 300 to 850, with 850 being the highest score representing a stellar borrowing record. The VantageScore system uses a scale from 500 to 990, which corresponds to an academic letter-grading system from F to A. Therefore, scores higher than 900 earn an A, scores from 800 to 900 a B and so on.I like the way the company is responding. MarketWatch quotes Ron Totaro, a Fair Isaac veep:

But Fair Isaac’s Totaro says lenders face significant hurdles in switching to new score models.

Some credit-granting firms “have been using a FICO score for 20 years in many cases. It’s embedded in lenders’ computer systems, lending processes…you can constantly go back and compare apples to apples on how a portfolio is performing or how you need to adjust your lending criteria,” he said.

While the credit-reporting agencies’ announcement today was a surprise, he doesn’t see the new product as a significant threat.

“We’ve been dealing with folks trying to come up with another type of credit score and it really hasn’t impacted us. We don’t see this particular item impacting our business in any way,” Totaro said.Yes, it’s not so easy to kill the king. Here’s Grudnowski again, this time in Business Week:

Fair Isaac Chief Executive Tom Grudnowski said in an interview that FICO scores are deeply embedded in the way lenders evaluate loan applications. The biggest challenge for the credit bureaus, he says, will be to prove that their score is so much better that it justifies ripping up the way they do things now. Says Grudnowski: “There’s got to be a really compelling reason to convince an institution to change.”

There are also anti-trust concerns. I’m not so sure three companies can get together so easily to take on a market leader.

The stock is below $37 this morning. I’ll gladly buy more if it goes any lower. -

The Middle East Markets Get Pummeled

Eddy Elfenbein, March 15th, 2006 at 7:32 amSome people think the Middle East is living in another century. Well, the region apparently just arrived at 1929.

The stock markets across the Arab world dropped dramatically yesterday. The Dubai Financial Market dropped 11.71%, which is eerily similar to the 11.73% that the Dow lost on October 29, 1929. Since its January high, the Dubai index is now off over 44%. But the good news is, they don’t run our ports!

I don’t mean to say “I told you so,” but I did, in fact, tell you so four months ago. (Dubai: Do Sell).This is a good time to remember that there’s an interesting correlation between market crashes and the largest buildings in the world. The Empire State Building went up just as our market crashed. The Petronas Towers were built as the Asian Tigers fell apart. The World Trade Center and Sears Tower accompanied the crash of the early 1970s. Even the Nasdaq’s shiny new office was opened just before its bubble burst.

The price of oil is already well below its high price. What’s good for consumers here isn’t good news for Dubai. I think Dubai is ready for a fall.And it’s not just Dubai. The pain is being felt all across the region. Since February 25, the Saudi Index is down 28%. According to Bloomberg: “Finance Minister Ibrahim al-Assaf said his government won’t intervene to stop the slide, the Saudi-owned television station Al-Arabiya reported.” So the state-owned media is telling us that the state won’t intervene in the markets. Somehow, I’m not relieved.

In Egypt, the government is working to prop up shares. The main index there, the CASE 30 Index, has doubled in each of the last three years. The index dropped 5.9% yesterday.

The Kuwaiti index is down 17% since February 7, and there have been protests for the government to do something.

For all the pain of a market crash, I’d like to believe that a financial crisis is an important step towards democracy. I even found a very sensible editorial against government intervention here. I hope the authorities behave reponsibly like a mature democratic country would, and not do anything dumb or silly to play upon public anger. -

Credit Derivatives Market Expands to $17.3 Trillion

Eddy Elfenbein, March 15th, 2006 at 6:13 amFrom Bloomberg:

Credit-default swaps, which pay compensation in the event of borrowers defaulting on their debt, expanded 105 percent in the full year, leading an increase in the $236-trillion market for derivatives, or contracts based on underlying assets. The market’s growth was slower than 123 percent increase in 2004, ISDA said in a report today at its annual meeting in Singapore.

Regulators are worried that credit derivatives are increasing too quickly for banks to control. The Federal Reserve Bank of New York has demanded action to tackle a backlog of contracts left unsigned for weeks or months, and for banks to address a shortage of bonds to settle contracts.Weeks or months?

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His