Archive for March, 2007

-

Kvetchin’ Gretchen

Eddy Elfenbein, March 15th, 2007 at 9:26 amDid anyone see Lost last night? Wouldn’t there be tons of dead animals around that sonic wall thing? Also, am I the only person who thinks about these things?

ANYWAY

Larry Ribstein rips into Gretchen Morgenson:All of this highlights what I’ve been saying about Morgenson for many months. It’s not about her views, or about whether her targets are behaving well or badly. It’s about the journalism: shoddy, hysterical, unsophisticated, misleading, and often just simply poor. More importantly, it’s about the standards of her employer, which persists not only in highlighting her opinions, but in putting them on the front page as “news.”

Dealbreaker has more.

-

Harley and the Subprime Market

Eddy Elfenbein, March 15th, 2007 at 8:26 amFrom Forbes:

Americans not only bought homes they couldn’t afford, they also spent money they didn’t have on Harleys.

In a note on Wednesday, Edward Aaron, an analyst for RBC Capital Market, said that Harley-Davidson’s financial unit has seen increased delinquencies and losses on loans given out over the past few years.

One reason for that phenomenon, he said, is the same reason that the subprime lenders are in financial turmoil — that is — they lent money to risky borrowers.

“While we don’t know which borrowers are accounting for the acceleration of loss rates in Harley’s loan securitizations, it’s stands to reason that the lower credit quality customer’s would be accounting for most of that change,” he said.

That doesn’t mean Harley is on the verge of implosion, Aaron said in an interview. But it may cause the motorcycle company’s earnings to sputter over the next few years.This is old news. Herb Greenberg wrote about Harley’s finance unit years ago.

-

Finally….

Eddy Elfenbein, March 14th, 2007 at 9:11 pm -

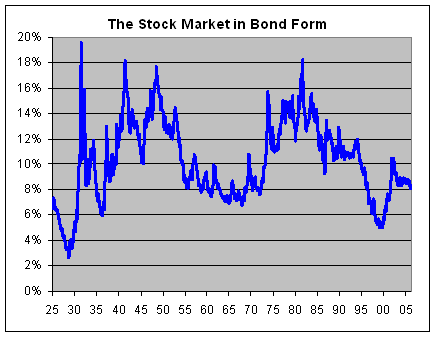

What If the Stock Market Was a Bond?

Eddy Elfenbein, March 14th, 2007 at 2:55 pmHere’s an unusual post. But it’s my blog, so deal.

I was curious what the historical stock market performance would look like if the stock market was a bond.

Strange? Let me take a step back and explain.

I have the monthly total return figures (including dividends) for the stock market going back to the 1920s. I wanted to take those same monthly changes, apply them to an imaginary bond and see what the yield would have been through the years.

I assumed that it’s a bond of infinite maturity and pays a fixed coupon each month. Actually, the amount of the coupon doesn’t matter, as long as it’s the same each month.

I have to think that many investors would be better served if there were such an investment vehicle. If they knew that the market’s current yield was something like 7% or 8%, they might treat their investments very differently.

What’s interesting is that investing in the 19th century wasn’t too far from this. Many stocks traded at or near “par” which was often $100 a share. Every year, the company would pay out an annual dividend, say $5 or $8 a share, sometimes none, sometimes $10 or $15. They dividend was the game, and there wasn’t nearly as much emphasis on long-term capital gains.

There’s one hitch though. I have to choose a starting yield-to-maturity for December 1925. So this isn’t a completely kosher experiment because the starting point is based on my guess. If I choose a number that’s too high, then the historical performance won’t be able to keep up, and the yield-to-maturity would grow higher and higher and soon leave orbit. Conversely, if my starting YTM is too low, the yield would gradually get pushed down to microscopic levels.

Fortunately, the data makes my job easy. If I start with 6.6%, the market’s yield gets

out of control by the 1970s. If I start with 6.5%, the yield goes to rock bottom levels by today. By my judgment, the best looking line starts with 6.538%.

Here’s what it looks like:

I have to stress that even though this “bond” is complete make believe, this reflects what the actual stock market really did for the past eighty-two years.

Over the last eight decades, the yield has averaged about 10.2%, which is right in line with the market’s long-term total return. Through February 2007, it stood at 8.3%. Seven years ago, it got down to 5% (by comparison, long-term Treasuries were going for 6.5%). -

Reader Quiz

Eddy Elfenbein, March 14th, 2007 at 1:37 pmOK class, here’s a short quiz. Let’s say the stock market sells off. We’re told it’s because investors have grown complacent about risk and bid up prices to irrational levels.

If that’s true, which stocks should do better—growth or value?

Despite the selling, growth is outperforming value. -

It’s Not Over Over There

Eddy Elfenbein, March 14th, 2007 at 10:07 amMore selling in Asia. Once again, the Indian market bore the brunt of the selling:

Here’s a roundup of the Asian markets. -

Cranky Octogenarian Opens Mouth

Eddy Elfenbein, March 14th, 2007 at 8:33 am

From the AP:Two weeks ago, Greenspan’s comments about the possibility of a recession occurring at the end of this year contributed to a 416-point fall in the Dow Jones industrial average.

The Dow had another big losing day on Tuesday, falling by 242.66 points, the second biggest drop of the year. But this decline was not driven by anything Greenspan said but rather investors worries about the subprime mortgage market.

During his appearance Tuesday, Greenspan talked about past market crises but not the most recent turmoil and he made no forecasts about the possibility of a recession.

Greenspan did put forward a proposal on how to reduce the growing inequality of incomes in the United States – admit more skilled immigrants into the country. -

From the Goldman Sachs Conference Call

Eddy Elfenbein, March 13th, 2007 at 10:09 pmI thought this was an interesting answer from CFO David Viniar:

Michael Hecht – Banc of America

I just wanted to follow up on FICC. You guys noted the record results in credit and mortgages. I was just wondering if you could talk a little bit more about the traction there in terms of it being more environmental versus share gains? Particularly in mortgages, are you seeing the best traction in sub-prime versus prime versus commercial or non-U.S.?

David A. Viniar

I think we have handled the turmoil in the market pretty well. Again, in mortgages, you have to remember to size it, and I’ve talked about this, so with sub-prime first. Sub-prime is part of mortgages, which is part of FICC, which is part of trading, which is part of Goldman Sachs. So the size of mortgages in all of Goldman Sachs is modest, while the business is important, like all of our businesses. Credit businesses are a little bit bigger than the mortgage business, but we really haven’t seen any contagion to the credit markets. The credit markets continue to be quite robust. Credit spreads continue to be tight. There continues to be a lot of liquidity in those markets.Courtesy of Seeking Alpha.

-

100 Years Ago Today

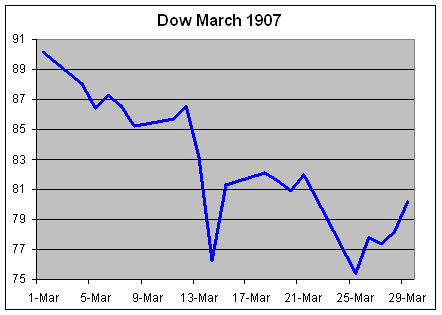

Eddy Elfenbein, March 13th, 2007 at 11:34 amThink your portfolio is having a tough time. Well, buck up. Today marks the 100th anniversary of the beginning of the Panic of 1907.

On March 13, 1907, the Dow CRASHED from 86.53 to 83.12. That may not sound like a lot, but it was a fall of 3.94%, which beats our wimpy 3.29% drop from two weeks ago. The next day, March 14, saw the really big action. The Dow plunged to 76.23, a drop of 8.29%. That’s a two-day drop of 11.9%. Today, that would be like the Dow losing 1,500 points in 48 hours. The drop of March 14 still ranks as the seventh-worst day in the Dow’s history.

The index shot up 6.69% on March 15, but all was not safe. The Dow fell 6.23% on March 25. Here’s a look at Dow during March 1907:

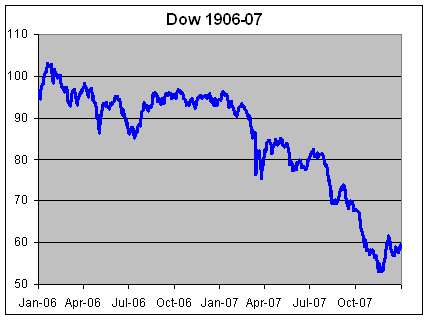

That was only part of it. In 22 months, the Dow fell by half. Here’s how the market did in 1906 and 1907:

J.P. Morgan helped end the panic by providing a loan to the U.S. government. This led people to think that it really might not be a good idea to have the government dependent on one guy’s terms. Soooo, in 1913 Congress passed the Federal Reserve Act.

And we haven’t had any trouble since. -

Goldman’s Earnings

Eddy Elfenbein, March 13th, 2007 at 10:00 amGoldman Sachs (GS) was supposed to report lower earnings today. This was supposed to be the quarter when the party ended for the big Wall Street houses. Well, it didn’t happen. Or at least, it hasn’t happened yet.

Goldman’s earnings blew away the Street’s estimates. The company earned $6.67 a share compared with $5.08 a share last year. That’s just amazing. Let me put that into context for you. Wall Street was looking for a decline to $4.89 a share. In fact, the highest estimate of any analyst was for $5.60 a share. Goldman still beat that by more than a dollar. This is the seventh straight quarter that Goldman has beaten earnings.

After the company reported earnings two quarters ago, the stock rose for 12 straight days. On the 13th day, it fell by a penny a share. Then it continued to rise for 12 of the next fourteen days.

Here’s a look at how the Big Five firms on Wall Street have done over the past four years:

Notice how all the stocks started to take a hit recently. Investors were clearly bracing themselves for bad news. Also, Guy Moszkowski, a high-profile analyst at Merrill Lynch, recently downgraded several stocks in the sector.

(You can also see why investors were so unhappy with Phil Purcell at Morgan.)

Goldman is now going for about 10 times next year’s earnings. Lehman (LEH) reports tomorrow.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His