Archive for June, 2007

-

Sorry Ladies

Eddy Elfenbein, June 11th, 2007 at 9:17 amDealBook‘s Andrew Ross Sorkin is off the market. My congratulations to the happy couple.

(Hat Tip: DealBreaker) -

Dick Parsons on Wal-Mart

Eddy Elfenbein, June 8th, 2007 at 1:45 pm“It will be a cold day in hell that I would actually get up from my apartment to go to the video store,” Mr. Parsons added. “I’ve never actually been in a Wal-Mart.”

-

Defending Bed Bath & Beyond

Eddy Elfenbein, June 8th, 2007 at 10:58 amI’m not the only one who still likes Bed Bath & Beyond (BBBY). Here are some other views:

SunTrust Robinson Humphrey analyst David Magee stood by his “Buy” rating and said the company will be one of the first to gain when the housing market shows signs of a bottom.

Magee also said the lowered expectations, while disappointing, are not that bad and its balance sheet remains strong. Magee also expects the company will use its $1 billion share repurchase program to enhance shareholder value.

“We had actually expected the market reaction to the news might be worse, and while we do believe there could be some additional near-term volatility, (we) don’t anticipate significant further declines in the multiple,” Magee wrote in a client note.

Meanwhile, CIBC World Markets Corp. Vivian Ma said a decline in the share price presents a buying opportunity. She remained bullish on the company’s long-term value.

“We think the sales environment could remain very competitive in the second quarter, but Bed Bath & Beyond may see some rebound sequentially,” Ma wrote in a client note. “Bed Bath & Beyond has been a consistent outperformer in other periods of consumer pullback.” -

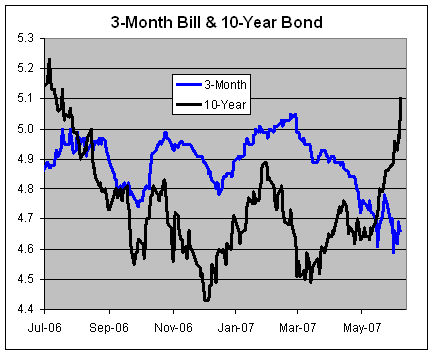

The Yield Curve Widens

Eddy Elfenbein, June 8th, 2007 at 10:54 amYesterday’s real action was in the bond market. The 10-year Treasury had its worst day in over three years. Here’s a chart of the 10-year T-bond along with the three-month Treasury bill to show you how much things have changed in the past month.

-

Breaking: Bill Gross Is Now a Bond Bear

Eddy Elfenbein, June 7th, 2007 at 3:40 pmAfter 25 years of being a bond bull, Bill Gross has turned bearish:

Long-time bond bull Bill Gross, just one year after declaring the end of the bear market for U.S. Treasuries, on Thursday conceded the snappy pace of global economic growth will likely keep bonds on their heels.

Furthermore, Gross forecast that benchmark Treasury yields will range higher than previously thought, prompting him to acknowledge he is now a “bear market manager” after a quarter century as the global bond market’s most powerful bull.

Gross, chief investment officer for Pacific Investment Management Co. and manager of the world’s largest bond fund, said solid global growth and a mild acceleration of inflation in the United States and abroad will drive 10-year U.S. Treasury note yields to top out at 6.5 percent over the next three to five years as opposed to the 5.5 percent ceiling previously forecast and 5.1 percent seen on Thursday.

Gross’s comments were included in a note summarizing an annual gathering of Pimco investment managers, a copy of which was obtained by Reuters. -

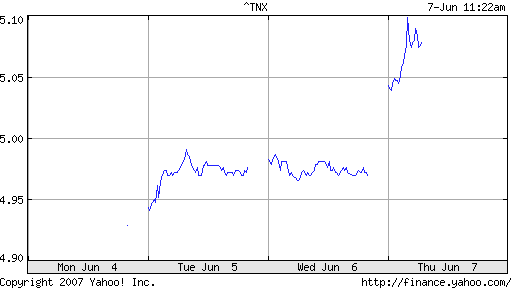

The 10-Year T-Bond Breaks 5%

Eddy Elfenbein, June 7th, 2007 at 11:44 am

This is the first time this has happened since last August. -

Victory!

Eddy Elfenbein, June 7th, 2007 at 9:57 amOr something not as close to defeat.

The private equity consortium looking to buy Biomet (BMET) has increased its bid to $46 a share. The vote scheduled for this Friday has been canceled. -

Citi’s Top Secret Plan

Eddy Elfenbein, June 6th, 2007 at 1:28 pmDealBreaker’s Bess Levin looks at Citigroup’s (C) newest strategy, breaking into the Boston banking market.

Pardon me while I go bang my head against the wall. First off, the Boston banking market is what? Four hundred years old. I’m sorry but this is just plain silliness.

Citigroup’s strategy is that it’s a “financial supermarket.” They figure “hey, we have credit card customers with Boston addresses, so they’ll certainly buy Smith Barney mutual funds!” You can just feel the synergy!

Let’s take a step back and look at this. We’re waiting to see if a company with $2 trillion in assets can make impact its business by impressing Bostonians with having one statement for their credit cards and investments.

Please, this is secret so whatever you do, don’t tell Fidelity (or State Street or Bank of America or Merrill Lynch or anybody else with $30 in deposits).

The financial supermarket idea doesn’t work. Repeat after me, Mr. Prince, it doesn’t work. I know, it sounds good on paper, but people don’t do their finances that way. They never have and they’re not about to now. This was just a nice idea to justify some lousy acquisitions many, many years ago.

Eddy’s rule of business #15,783: No matter who is put in charge to execute a dumb idea, when it starts to fail, people will blame the execution, not the dumb idea. Lots of people are ready to toss Chuck Prince overboard. Fine, but he’s not the problem.

Twenty-five years ago, Sears bought Dean Witter. They had this great idea. Stick brokerage offices in the stores! Well, it didn’t work and Sears eventually sold Dean Witter. Later Dean Witter bought Discover and turned it into a hugely profitable credit card business. Then Morgan merged with Dean Witter, and made a whole lotta money.

Guess what Morgan is spinning off now? Discover!

Think about it, Chuck. Split Citi up. -

The Coolest Water Buffaloes Versus Lions Versus Crocs Video You’ll See All Day

Eddy Elfenbein, June 6th, 2007 at 11:19 am

Funny, this is oddly familiar to the J&J/Guidant/Boston Scientific fight last year. -

Trophy Stocks

Eddy Elfenbein, June 6th, 2007 at 9:13 amTom Wolfe coined the phrase “trophy wife.” Now, Michael Lewis says the reason the rich want to own newspapers isn’t for the money, but for the status.

This logic explains what appears to be happening right now inside the two great national newspapers, the New York Times and the Wall Street Journal.

The cachet of the New York Times is worth more to the Sulzberger family than to anyone else. The Sulzbergers’ relationship to the Times is the chief source of their status; without it they are mere mortals with a bit of cash; and so the Sulzbergers cling to their control of the Times as tightly as ever.

Instead of getting out while the getting is good, they flop around looking for new ways to raise money without ceding control, and to make money without leaving the news business. Which is to say, they are working as hard as they possibly can to throw good money after bad — with the predictable result that they have alienated their outside investors.When you have nothing else to offer except a gazillion Class A shares, you’ll naturally overvalue your role, which the Bancrofts see as protecting the Journal’s independence. They’re confusing vanity for high-mindedness.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His