Archive for December, 2007

-

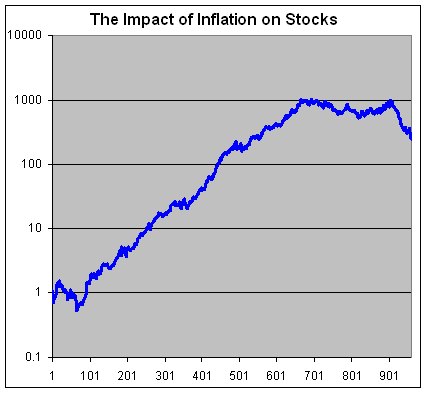

Inflation’s Impact on the Stock Market

Eddy Elfenbein, December 14th, 2007 at 10:26 amSo how does inflation affect the market? Well, it’s not good. Inflation is a tax on capital. It’s a way for the government to get your money without asking. In fact, the only thing worse than inflation is deflation.

I took 80 years of monthly stock market return and ranked them by inflation (lowest to highest). Then I wanted to see the cumulative return as the rate of inflation increased. Here are the results.

At the far left are the most deflationary months, and the far right are the most inflationary. The blue line shows the after-inflation cumulative return of the market.

As you can see, deflation has a negative impact on equity prices. The market falls until about the 70th data point which corresponds with an annualized deflation rate of 5.5%. The vast majority of those months were in the 1930s.

Stocks rise very steadily until it hits a brick wall around data point 660. That corresponds with an inflation rate of 5.1%. -

CPI Surge

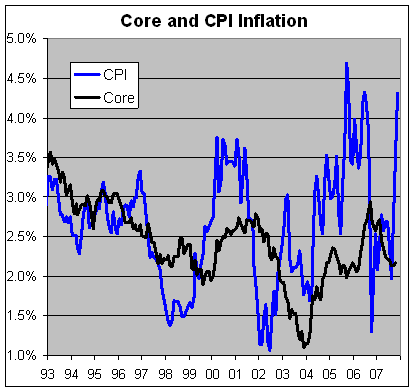

Eddy Elfenbein, December 14th, 2007 at 9:25 amThe government just reported that consumer inflation surged 0.8% last month. That’s the fastest rate in more than two years. The year-over-year rate is now 4.31%, which is slightly more than where the Fed is. Still, I’m an inflation skeptic. The government’s numbers most certainly understate the rate of inflation, but I’m only concerned if inflation seems to be getting out of hand.

The core rate was just 0.3% last month. Yes, yes, I know the core rate comes in for a lot of criticism, but I think it’s important to watch. For nearly twelve straight years, the year-over-year core rate has never been greater than 3% or less than 1%. Also, long-term interest rates are still quite low.

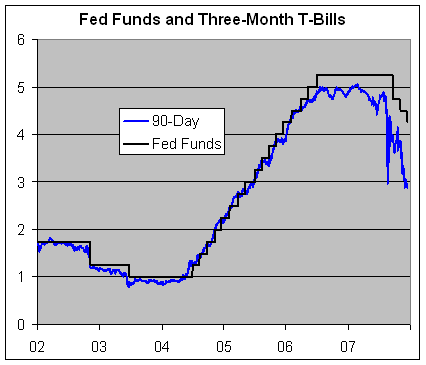

In fact, more Fed rate cuts could be on the way. The rate on short-term Treasury bills are still far below the Fed Funds rate. Yesterday, the T-bill rate closed at 2.78%, the lowest since the August panic. The Fed is about 140 basis points above the market.

-

Bill Miller on Risk

Eddy Elfenbein, December 13th, 2007 at 3:03 pmVia B-Ritz:

You also know that rising stock prices mean lower future rates of return and falling stock prices mean higher rates of return. So I was much happier in the summer of ’02 when you buy everything on sale than I was in the Spring of 2000 when a lot of things were super-expensive.

My view is that the evidence is overwhelming that most people are too risk averse. And that therefore they should be taking a lot more risk than they feel like is right.

The problem is that real risk and perceived risk are two different things. And that’s where people get into trouble, because they perceive risk to be high when prices are low, and they perceive risk to be low when prices are high. That’s the psychological problem that most people have. -

Buy List Update

Eddy Elfenbein, December 13th, 2007 at 12:34 pmGood news from Jos. A Bank Clothiers (JOSB). The company just reported earnings of 38 cents a share, which is a big jump from the 30 cents it made in the same quarter a year ago. The Street was looking for earnings of 33 cents a share. Sales rose 10% to $131.3 million.

This stock has had a bizarre year. For the first half of the year, it charged out of the gate and gave us a quick 57% profit. It then took it all back and we’re now in the red. But I still like JOSB and the numbers look good.

Late yesterday, Danaher (DHR) reaffirmed its Q4 outlook for EPS of $1.09 to $1.14. Sometimes investors ignore these “reaffirm” stories. I don’t. It’s one thing to say earnings will be good, but it’s nice to see a company follow-up on their forecast, even if it’s just reaffirming. DHR expects 2008 EPS to range between $4.30 to $4.40. -

Advice from Harry Schultz

Eddy Elfenbein, December 13th, 2007 at 11:52 amPeter Brimelow finds some interesting advice from legendary newsletter publisher, Harry Schultz, outside the usual that the world is going to hell:

Amid the apocalyptic advice, Schultz finds time to dispense some other helpful hints. Avoid fluoride. Cell phones may cause cancer. Sauerkraut makes for a healthier prostate. Use faxes for all financial transactions. Give money to Republican presidential candidate Ron Paul on his Dec. 16 Boston Tea Party anniversary fundathon.

-

Team Spirit

Eddy Elfenbein, December 13th, 2007 at 11:38 amA-Rod Signs Record $275 Million Deal With Yankees

“The real question was, did he really care about being a Yankee or is he just about the money,” Steinbrenner said in a Nov. 14 interview. “It’s apparent he wants to be a Yankee and it’s not about the money.”

In other news: Goldman chief’s pay set to hit $70m.

-

The Back-Dating Bubble Bursts

Eddy Elfenbein, December 12th, 2007 at 1:12 pmLarry Ribstein of Ideoblog deserves some sort of blog award. Early on, he correctly called the back-dating brouhaha of 2006 what is was, a media-driven pseudo scandal. Now here we are in 2007 and the scandal bubble has burst.

The one big fish the authorities got was Greg Reyes, the former head of Brocade. In August he was convicted of conspiracy and fraud. Ribstein said that Reyes was “trying to maximize shareholder value by recruiting the best people, not line his pockets, and where it’s unlikely any misstatements hurt investors.”

Now it looks like they’re going to lose this case as well. Andrew Ross Sorkin reports in today’s NYT:A principal witness in the stock-options backdating trial that ended in a conviction of Gregory L. Reyes, the chief executive of Brocade Communications Systems Inc., has told associates her testimony may have been untrue, according to court documents.

In affidavits, friends and associates of the witness, Elizabeth Moore, a Brocade employee who testified that Mr. Reyes deceived the company, said she had privately retracted her testimony.For uncovering the back-dating scandal, The Wall Street Journal won a Pulitzer Prize.

-

If the Market Is So Darn Efficient, Then Why Is this Blog Free? Wait, Don’t Answer That!

Eddy Elfenbein, December 12th, 2007 at 11:57 amMegan McArdle, my favorite libertarian blogstress, has some thoughts about Michael Lewis’ Portfolio article and Efficient Market Hypothesis (see also here and here). Megan is a great blogger and I read her every day.

I don’t want to get too deep in the weeds on this topic but I’m an EMH skeptic and I want to explain why. My main beef with it is that EMH suffers from theoretical overreach.

OK class, let’s remember our scientific method. A theory is a logical explanation for natural phenomena. Well, EMH explains a whole lot, but there are still some holes. The wholes aren’t big, mind you, but they’re definitely there and can’t be ignored.

Maybe some day, someone will come along with a better explanation for the market and those holes. I hope that day comes soon, but until then, EMH is the best we got.

To me, the most significant hole is that value stocks have consistently outperformed the market and they’ve done it with less volatility. The data here is unambiguous. It goes back 80 years and it’s clear as a bell. Again, we’re not talking about a huge difference, but it’s there. There are others (Yahoo at $25?), but that’s the cleanest.

Let me be clear: I think the market is very efficient, but the market can be consistently beaten. It’s not luck. It’s just very, very, very, very hard.

As a practical matter, there’s a lot to be said for index funds. From my experience of investor behavior, more people ought to own them.

It’s interesting that EMH defenders always say that the market can’t be beaten. They rarely defend the other half—the market can’t beat you. What can I say? I know people who have done a great amount of empirical research on this front and their results are, sadly, quite compelling.

One final note: Please feel free to ignore the fact that this is a discussion of efficient markets taking place on free blog sites.

Update: Megan has more today:I am being assailed by people pointing out that Berkshire Hathaway has done spectacularly, and therefore this EMH stuff is a bunch of hooey. I could point out that if you’d had a million guys flipping coins repeatedly for a year, at least one of them would have come up with a massive streak of heads. Even if you paid him $1mm for each heads flip, this would not actually be attributable to his awesome coin-flipping skill. Indeed, you’d have at least one cluster of guys who’d done well…perhaps fellows who’d gone to Harvard together, or people who’d all studied “Value Coin Flipping” under a master. There would be other outliers, and other groups of people who’d studied “Fundamentalist Coin Flipping” or “The Vincenzi Flipping Technique” who would not have done well. But no one would be looking to them for advice, so you would never have heard of them, and it would seem like a minor miracle that this guy, this technique had just produced such amazingly outsized returns.

If superior performance were solely due to luck, wouldn’t we see more “successful” coin-flippers attribute their returns to arbitrary sounding strategies? You know, investing by astrology, the weather or charts patterns. Hey, if it’s all luck so the strategy shouldn’t matter.

But that’s not what we see. If you go down the list of people who have amassed great long-term track records, each one credits Graham and Dodd style value investing. There’s Peter Lynch. There was Bill Ruane who met Buffett decades ago at a Graham conference. There are the guys who Leucadia National who have done even better than Berkshire. They espouse the exact same philosophy. The guys at Danaher. The Tisch brothers. Eddie Lampert. The list goes on and on.

As far as I know, no technical analyst is on the Forbes 400 but there are lots of value investors. -

Greenspan in Today’s WSJ

Eddy Elfenbein, December 12th, 2007 at 7:53 am

The Roots of the Mortgage Crisis

By Alan GreenspanAfter more than a half-century observing numerous price bubbles evolve and deflate, I have reluctantly concluded that bubbles cannot be safely defused by monetary policy or other policy initiatives before the speculative fever breaks on its own. There was clearly little the world’s central banks could do to temper this most recent surge in human euphoria, in some ways reminiscent of the Dutch Tulip craze of the 17th century and South Sea Bubble of the 18th century.

I do not doubt that a low U.S. federal-funds rate in response to the dot-com crash, and especially the 1% rate set in mid-2003 to counter potential deflation, lowered interest rates on adjustable-rate mortgages (ARMs) and may have contributed to the rise in U.S. home prices. In my judgment, however, the impact on demand for homes financed with ARMs was not major.

Demand in those days was driven by the expectation of rising prices — the dynamic that fuels most asset-price bubbles. If low adjustable-rate financing had not been available, most of the demand would have been financed with fixed rate, long-term mortgages. In fact, home prices continued to rise for two years subsequent to the peak of ARM originations (seasonally adjusted).

I and my colleagues at the Fed believed that the potential threat of corrosive deflation in 2003 was real, even though deflation was not thought to be the most likely projection. We will never know whether the temporary 1% federal-funds rate fended off a deflationary crisis, potentially much more daunting than the current one. But I did fret that maintaining rates too low for too long was problematic. The failure of either the growth of the monetary base, or of M2, to exceed 5% while the fed-funds rate was 1% assuaged my concern that we had added inflationary tinder to the economy.Notice how we’ll never know if we avoided corrosive deflation, yet Greenspan is confident that low rates weren’t a major factor in the housing bubble. Conveniently, he saved us from the event that never came and couldn’t protect us from the one that did.

-

Electability Update

Eddy Elfenbein, December 12th, 2007 at 7:12 amI written about this topic before but one of the things I find fascinating about finance is how you can use markets for two items to create an “implied market” for a third. This idea is at the root of all the complex financial instruments that caused problems for so many hedge funds recently.

I’ll give you a good example. At InTrade.com, the site where you can trade futures on real world events, you can buy contracts on which candidate will win his or her party’s nomination next year. There’s a separate contract for which candidate will win the presidency.

Let’s break out some math, shall we?

If you divide the latter by the former, you get an “electability” contract. For example, according to recent prices, Rudy Giuliani has a 41.5% chance (I’m using the last price) of getting the GOP nomination and an 18.4% of winning the presidency. Soooo…the market believes that if he gets the nomination, he has a 44.34% chance of winning (18.4% divided by 41.5%).

(The only minor flaw is that could include a candidate winning but not getting the nomination, however, I’m content with dismissing that possibility as beyond remote.)

What’s interesting is electability in the general election can have little impact on how well a candidate does in the primaries. Some people, myself included, think that Ronald Reagan would have had a better chance of beating Jimmy Carter in 1976 instead of Gerald Ford, even though Ford beat Reagan for the nomination.

I should add that I don’t place a great deal of faith in these real world futures markets. I simply see them as fun games to enjoy, but not to take too seriously. Also, the markets aren’t very liquid. A minor change could have a big impact on the smaller-priced contracts.

Having said that, here’s a look at some candidates and the market’s take on their electability (sorry Paulites and Edwards fan, your candidates were too low to get a useful meaure).

Candidate………To Get Nomination….To Win…………Electability

Hillary……………………..59.5……………….39.0………………65.55

Obama……………………33.0……………….17.2………………52.12

Giuliani……………………41.5……………….18.4………………44.34

Huckabee………………..18.6…………………7.2………………38.71

Romney…………………..18.8…………………5.9………………31.38

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His