Archive for June, 2008

-

Lehman Drops Bomb

Eddy Elfenbein, June 9th, 2008 at 10:18 amWall Street had been expecting Lehman Brothers to post a loss of a couple million here and there. Turns out, a couple million was really 2800 million. This is their first-ever loss since going public. The company is also going to raise $6 billion in new capital.

Adding insult to injury, Jenny Anderson writes:Lehman Brothers, among the smallest players on Wall Street, announced on Monday that it will raise up to $6 billion in fresh capital from investors.

Jeez, it’s one thing to lose money, but there’s no need to get phallic. The shares are getting smacked today, but they’re still above the panic low from March.

Bess Levin is live-blogging the call. -

RIP: Bo Diddley

Eddy Elfenbein, June 6th, 2008 at 5:28 pm

He also appeared in Trading Places. -

Billionaire Drug Bust

Eddy Elfenbein, June 6th, 2008 at 12:03 pmThe Smoking Gun is on the scene:

The billionaire apparently did little to conceal his drug transactions. On one occasion, in the lobby of Broadcom’s southern California headquarters, he directed an employee to provide cash to a courier “in exchange for an envelope containing controlled substances,” the indictment charges. On a drug-fueled 2001 private plane flight–during which Nicholas allegedly used and distributed narcotics–the pilot was forced to don an oxygen mask due to the “marijuana smoke and fumes.” According to a March 2008 Forbes story, Nicholas, with an estimated net worth of $1.8 billion, is ranked 677 on the list of the world’s wealthiest individuals.

-

Huge Jump in Unemployment

Eddy Elfenbein, June 6th, 2008 at 9:56 amThe government reported today that the unemployment rate jumped from 5.0% to 5.5%. Many news outlets are saying that this was the largest increase in 22 years. I broke down the data into a few more decimal places, and it’s actually the largest increase in 28 years. Nonfarm payrolls declined by 49,000.

-

Bernanke Bombs at Harvard

Eddy Elfenbein, June 5th, 2008 at 9:07 am“These, obviously, are not the kind of topics chosen by many recent Class Day speakers,” Bernanke said. “But, then, the class marshals presumably knew what they were getting when they invited an economist.”

While the class marshals may have known what they were getting, it seemed many of the seniors present did not.

“I’m annoyed, I’m irritated. I just think that a person who speaks for the class should be able to impart words from experience, especially someone who has risen so much and has come so far, from right where we are,” said Jennifer C. Arcila ’08, who was among the steady trickle heading out before the speech finished.Here’s the speech.

(Via: Mankiw.) -

The Buy List Is Still Rolling

Eddy Elfenbein, June 4th, 2008 at 6:21 pmThanks to Jos. A Bank Clothiers‘ (JOSB) big earnings report, that stock soared over 11% today. Net income jumped 18% in their fiscal first quarter. The company earned 53 cents a share, which topped the 46-cent estimate.

This helped the 20 stocks on my Buy List gain an average of 1.17% today compared with a decline of -0.03% for the S&P 500. This is the 10th time in the past eleven days that we’ve beaten the market. Since May 20, we’re up 1.35% compared with a -3.46% decline for the S&P 500. -

More on Momentum Losing Momentum

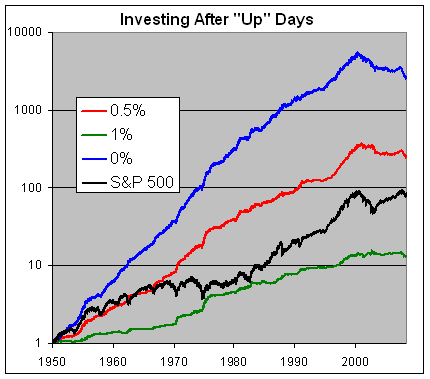

Eddy Elfenbein, June 4th, 2008 at 1:28 pmThe world’s easiest timing strategy, only invest after up days, was a huge winner for many decades, but not anymore.

Check out the chart below:

The blue line is what you would have earned if you had only invested on days following stock market advances (dividends aren’t included). The red line is for days following 0.5% advances. The green line is days following 1% advances, and the black is the S&P 500.

By early 2000, the blue line had returned over 5,000-fold which lapped the S&P 500 by 60 times. Unfortunately, it’s not a very practical trading strategy, considering how often you have to go in and out of the market. Still, that’s one of the more astonishing figures I’ve ever calculated, especially considering how simple the rule is.

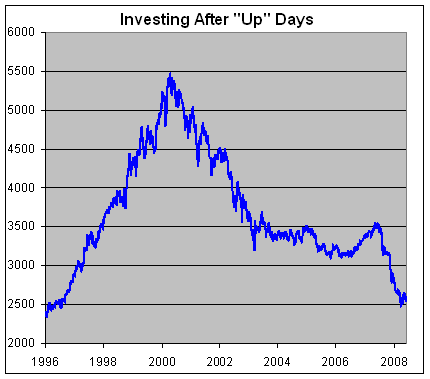

Since 2000, however, the strategy has been a bust. The blue line is still below half its peak from eight years ago. It’s not just the burst of the tech bubble, the blue has done especially poorly in the past year. Here’s the blue line again, but only over the past few years (and no log scale):

So what’s going on here? One answer is that an efficient market has simply caught up with a good idea and it no longer works.

But I think another explanation could be, it’s the result of a subtle shift in the nature of the market. Instead of being trend-enforcing, the market has become trend-negating. Each up move is no longer confirmed, but is now fought. If so, I think that’s a healthy development for the market.

But that’s just speculation on my part. What do you think? -

What If the Stock Market Were a Bond?

Eddy Elfenbein, June 3rd, 2008 at 1:35 pmHere’s an update of a post I did last year. I thought it would be interesting to see what the stock market’s historical performance would look like if the stock market were a bond.

Let me explain what I mean.

I took all of the monthly return data for the stock market going back to the 1920s. I then wanted to see what a bond would look like if we applied those exact same monthly changes to it.

I assumed that it’s a bond of infinite maturity and pays a fixed coupon each month.

There’s one hitch though. I have to choose a starting yield-to-maturity for December 1925. So this isn’t a completely kosher experiment because the starting point is based on my guess. If I choose a number that’s too high, then the historical performance won’t be able to keep up, and the yield-to-maturity would grow higher and higher and soon leave orbit. Conversely, if my starting YTM is too low, the yield would gradually get pushed down to microscopic levels.

Fortunately, the data makes my job easy. After eight decades, the window I have to work with is pretty narrow. If I start with 6.6%, that’s too high, and 6.5% is too low. After playing with the numbers, I settled on 6.538%.

Even though this “bond” is complete make-believe, it reflects what the actual stock market really did for the past 83 years.

Over the last eight decades, the yield has averaged about 10.2%, which is right in line with the market’s long-term total return. Through the end of May, it stood at 8.75%. Eight years ago, it got down to 4.9% (by comparison, long-term Treasuries were going for 6.5%).

Last year, I wrote:I have to think that many investors would be better served if there were such an investment vehicle. If they knew that the market’s current yield was something like 7% or 8%, they might treat their investments very differently.

What’s interesting is that investing in the 19th century wasn’t too far from this. Many stocks traded at or near “par” which was often $100 a share. Every year, the company would pay out an annual dividend, say $5 or $8 a share, sometimes none, sometimes $10 or $15. They dividend was the game, and there wasn’t nearly as much emphasis on long-term capital gains. -

Soros Now Celebreating Ten Years of Gloom

Eddy Elfenbein, June 3rd, 2008 at 11:30 amGeorge Soros is currently testifying on Capitol Hill about the high cost of oil.

The BBC reported: He warned that a “global credit crunch” was in the making and would probably lead the world into recession. Actually, that last part is from nearly ten years ago, but with Soros, he always sees disaster, the particulars may change. In 2000, he was warning us about the disintegration of the euro. -

Wachovia’s CEO Ousted

Eddy Elfenbein, June 3rd, 2008 at 10:56 amI’m glad we had Golden West Financial on our 2006 Buy List, and I was glad that Wachovia (WB) bought the company. For the tracking purposes of the Buy List, shares of Wachovia replaced the shares of Golden West. However, there was no way I was going to keep Wachovia on the 2007 Buy List. Fortunately, that decision proved correct.

What was our good fortune was bad news for Wachovia’s CEO Ken Thompson. He was let go yesterday by the board of Wachovia. BusinessWeek reports:According to one Wachovia insider, Crutchfield’s downfall came when “he stopped listening” to his other executives. Likewise, it’s hard to believe Thompson didn’t get resistance from his own management team about buying Golden West—and ignored it.

Because no one outside of Thompson and Golden West CEO Herb Sandler seemed to like the deal from the moment it was announced. Indeed, in the initial conference calls with analysts and investors after the deal, Thompson was on the defensive from the outset.

For Thompson, the Golden West purchase gave him the beachhead in California he had long desired. It also gave him an array of creative mortgage products to pump through his broker channel. But the ink was barely dry on the Golden West deal in late 2006 when the housing bubble in markets including California and Florida began to deflate. And by early this year, the mounting losses from Golden West, coupled with deteriorating credit quality in the rest of the bank’s portfolio, began to hit Wachovia hard: The bank reported a $393 million loss in the first quarter and then amended the report in mid-May to say it really lost $708 million after a review of its portfolio of bank-owned life insurance. That forced the bank to cut its dividend by more than 40% and to sell $8 billion in new shares—a move that served to bolster Wachovia’s equity but diluted the value of existing shareholders’ stock.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His