Archive for July, 2008

-

The Eight Lean Years

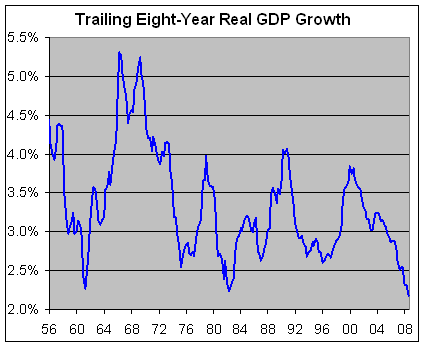

Eddy Elfenbein, July 31st, 2008 at 2:31 pmFor the last 32 quarters, real GDP has grown at annualized rate of 2.18%.

That’s the slowest eight-year growth rate since…well, my quarterly data only goes back to 1947. -

Nicholas Financial’s Earnings

Eddy Elfenbein, July 31st, 2008 at 11:35 amFor the second quarter, Nicholas Financial (NICK) earned 15 cents a share. Since the stock is basically priced for Armageddon, I think this is good news.

Revenue increased by 8% and EPS dropped from 27 cents to 15 cents. The major culprit isn’t hard to spot. The provision for credit losses nearly tripled from last year. Without that, pre-tax profit actually grew by about 4% over last year. The stock is now trading at less than 35 times this quarter’s earnings. -

Second-Quarter GDP Growth

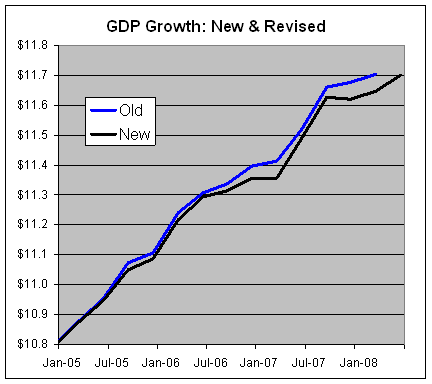

Eddy Elfenbein, July 31st, 2008 at 9:38 amThe government reported today that GDP grew by 1.89% for the second quarter. This is the sixth time in the last eight quarters that GDP growth has come in less than 2.7%. The government also revised its numbers for each quarter going back to the start of 2005.

The revisions aren’t terribly dramatic but they mostly say that growth has been weaker than we thought. From the fourth quarter of 2004 to the first quarter of 2008, the original forecast had been that real GDP grew by 8.4%. Turns out it was just 7.9%. That may not sound like much but it’s over $50 billion that’s vanished with a keystroke. I know I miss it already.

We also learned that the fourth quarter of 2007 was in fact, a negative quarter, and the first quarter of 2007 was just barely positive. The newspaper definition of a recession is back-to-back quarters of negative growth. In reality, the official timers of recession use a much more sophisticated method for pinpointing the beginning and end of a recession. What we’re experiencing may be an extended period of low growth, but where the economy doesn’t experience much actual contraction.

Here’s real GDP growth, old and new (in trillions):

-

Least Coherent Sentence of the Day

Eddy Elfenbein, July 30th, 2008 at 2:20 pmFrom an unnamed media company whose stock is 75% off its high:

Some experts have said that the law was wrong-headed in its effort to retain the hybrid nature of the mortgage finance giants, which are private companies with publicly traded stock, but which have an explicit guarantee of help from the government — an arrangement that critics say privatizes the profits but socializes the risk and any losses.

Let me take a deep breath to get my head around this, but the definition of the public company is one with publicly traded stock, therefore a private company can’t have publicly traded stock. Now if they meant private in the sense that it’s not nationalized, well that’s a different can of incoherence. If it were nationalized, then it wouldn’t be publicly traded. Is this really that hard?

-

S&P 500 and Earnings

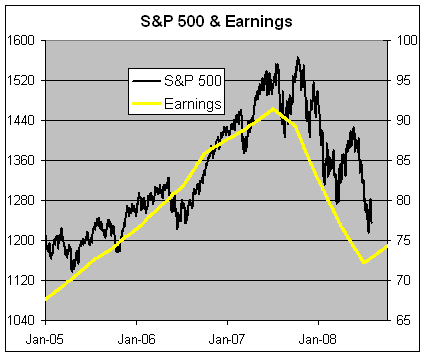

Eddy Elfenbein, July 30th, 2008 at 10:47 amHere’s a look at the S&P 500 (black line, left scale) and its earnings (gold line, right scale). The graph is scaled at 16-to-1.

I think it’s clear that the market isn’t undervalued, given its current condition. What will matter is if the downturn is earnings will really by over this quarter. Given the rate that earnings have been cut, that’s far from certain. -

Fiserv’s Earnings

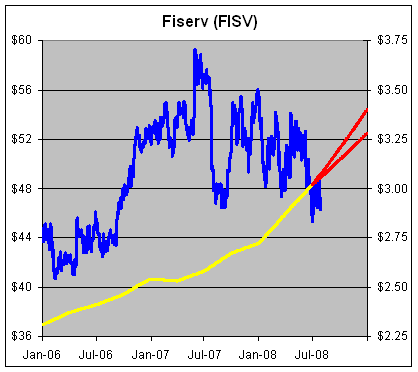

Eddy Elfenbein, July 29th, 2008 at 5:48 pmFiserv (FISV) just came out with a solid earnings report. For Q2, the company earned 83 cents a share from continuing ops. That beat the Street’s consensus by four cents a share. Revenue rose 38% to $1.30 billion. The company projects full-year EPS at $3.28 to $3.40.

Here’s a look at Fiserv’s stock (blue line, left scale) and earnings-per-share (gold line, right scale).

The red indicates the company’s EPS projection. I’ve scaled the graph at a ratio of 16-to-1, which is pretty conservative. That means that when the lines cross, the P/E ratio is 16.

You can see how far the company’s valuation has fallen even though earnings growth seems to be holding up well. That’s as good a definition as any for a good buying opportunity. -

Obama Gives Bernanke Vote of Confidence

Eddy Elfenbein, July 28th, 2008 at 12:26 pmWell, the election is over now. Bernanke wins 1-0.

“I think that Chairman Bernanke was handed a pretty tough hand and I think some of the decisions he’s made have been the right ones,” the presumptive Democratic nominee told Reuters in an interview on Saturday evening.

-

What Did Experts Have to Say at the Beginning of the Year?

Eddy Elfenbein, July 28th, 2008 at 11:29 amIf you can look into the seeds of time, and say which grain will grow and which will not, speak then unto me.

Generally, I’m not a big fan of the story, “so-and-so said to buy stock X, and it’s down therefore so-and-so is a moron.” Being wrong about the market doesn’t make you a moron. Claiming you didn’t say something you clearly did, however, does. Still, it’s worth taking a look at what the experts said that 2008 would have in store.

I dug up BusinessWeek’s article from last December, “Where to Put Your Cash in 2008.” Ah, those were innocent days!

William Greiner said that his favorite stock is Starbucks (SBUX). Youch! The stock is off by about 30% YTD. It gets worse. Tobias Levkovich said to buy financials. No comment needed. Jason Trennert had a year-end target for the S&P 500 of 1680. Leo Grohowski’s favorite stock was FCStone Group (FCSX) which is now down by about 60%. David Bianco had an S&P 500 target of 1700, and his favorite stock pick, Oracle (ORCL), is about flat for the year.

So what’s the lesson here? Is it that all these people are morons and we should never listen to them? Not at all. The great thing about investing is that you don’t need to predict the future. You don’t have to predict elections. You don’t even have to predict Fed policy. Successful investing isn’t about predicting what the market will do, it’s really a game of risk management. In fact, knowing that you can’t predict the future is the best starting point. Each investor should ask themselves, “given that I can’t predict what will happen 12 months from now, what’s the best way to position my portfolio to profit?”

That’s why I favor a diverse portfolio of financially sound companies trading at reasonable prices. I shouldn’t be making fun of anyone’s predictions since I have UnitedHealth Group (UNH) on my Buy List. The stock has gotten clobbered all year. Still, I’m a bit ahead of the market because I’ve diversified my Buy List. I love Nicholas Financial (NICK) and I bought some more last week. I have no idea why the stock is so low. All I know is that it is. I don’t know when it will go closer to its true value. It could be one day or one year. Or it could fall off a cliff. I don’t know, but I’ve loaded up my Buy List with enough stocks like NICK to bend the odds in my favor.

Today, Sohu.com (SOHU) made news because it reported amazing earnings results. Yet the stock is down today. That may not make a lot of sense, but that’s how the market can act in the near-term. This is a good time to revisit my investing philosophy from the FAQ page:What’s your investing philosophy?

My investing philosophy is very simple: Investors ought to buy and hold great companies. It doesn’t get more complicated than that. Avoid trading in and out of stocks, and be well-diversified. Investors should own at least 12 stocks, and have a goal of owning 20.

Be prepared for bear markets. A lousy market can strike at any time without warning. All stocks go down. It doesn’t mean the stock is broken. Stocks are volatile by nature. That’s the price you pay for superior returns. If you can ride out the bad times, you’ll be rewarded. If you can’t bear to see your portfolio drop by 50%, do not invest in the stock market. -

The Right Stuff

Eddy Elfenbein, July 28th, 2008 at 10:19 amAh, the joys of a well-executed roll-up strategy in a growing but fragmented market.

That has been the winning formula for Amphenol, (APH) a maker of connectors for electronic and fiber-optic systems that has combined internal growth with growth through acquisition to triple sales since 2002.

A skilled hand at boosting margins at acquired firms, Amphenol has grown earnings even more swiftly. The firm recently raised earnings estimates for this year to $2.34-$2.38 a share. That’s over five times the 46 cents it earned in 2002.

Amphenol’s connectors, which allow the mating of different elements within a broad range of electronic products, have been in demand. With strong sales to military, commercial aerospace and mobile device customers leading the way, Amphenol posted record sales and profits in the June quarter, exceeding analysts’ guidance.

Along with raising earnings guidance, the company also hiked revenue guidance for all of 2008, predicting sales of about $3 billion, a better than 15% gain vs. ’07. With robust cash flow and almost $200 million of cash and short-term investments on the balance sheet, Amphenol is well-positioned for further performance-boosting buyouts.

“They are the consolidators in an extremely fragmented marketplace,” said Amit Daryanani, equity analyst with RBC Capital Markets. The 10 largest connector firms — including Amphenol and its two biggest rivals, Tyco Electronics (TEL) and Molex (MOLX) — hold 55% of the global market. More than 2,000 smaller companies share the remaining 45%, Longbow Research analyst Shawn Harrison says.

Amphenol typically acquires firms with niche products and then broadens sales through its vast global distribution network, Harrison says.

Amphenol has a history of identifying good acquisition targets running 10% operating margins and then bringing those margins up to the stellar corporatewide standard, now approaching 20%, according to Daryanani.

In 2005, Amphenol purchased Teradyne’s connector business, then running at mid-single-digit margins. By mid-2007, the business was running at 19% operating margins. Among the efficiencies Amphenol brings to new buys: savings in volume procurement, efficient inventory management and “good management controls,” according to Daryanani.

Amphenol acquisitions contributed 4% to the company’s 2007 revenue growth. But other things also have been going well for the connector kingpin, whose products form the seams in items ranging from cell phones and computers to complex military electronics.

Organic growth in existing businesses contributed 8.5% to last year’s overall growth, with favorable currency movement kicking in an additional 2.7%, Daryanani said.

In the second quarter, sales to military, commercial aviation and mobile-device customers all grew smartly. With wars in Afghanistan and Iraq and strength in commercial aviation sales, combined military and commercial aerospace sales grew by 24% year over year. That represents one-fifth of Amphenol’s revenue, Chief Executive Officer Martin Loeffler said during a July 17 earnings call.

The company did not respond to requests for interviews with top executives.

Growing still faster, but from a smaller base, were products used in mobile devices, up 50% year over year and now representing 11% of total revenue. Interconnect offerings for wireless infrastructure including cellular base stations also did well, tacking on 36% growth and now representing 13% of total sales, Loeffler reported.

Amphenol benefited from the buildout of a cellular infrastructure in India, Citigroup analyst Jim Suva says. (Citi has provided investment banking services for Amphenol.)

“They’re in the right end markets,” Harrison said.

Amphenol also has won share in those markets. Harrison cites mobile handsets, cellular infrastructure, defense and automotive as connector customer sectors where Amphenol has amassed share.

But there is risk in some of these sectors. Mobile handset sales, for example, are expected to be down significantly in 2008, Harrison says. A Barack Obama presidential victory that brings expedited withdrawal from Iraq could pinch the military business. Sales to commercial aviation customers like Boeing and Airbus could suffer, too, if the airlines, hit with altitudinous fuel costs, delay delivery of ordered planes.

Amphenol President and Chief Operating Officer Adam Norwitt told analysts that even in the event of a change in war strategy, Amphenol’s military business would continue to flourish. He said engagement in two wars has slowed several other defense programs, including the Joint Strike fighter, and these programs could pick up, providing new sources of revenue if war operations are cut back.

“We do see strength and the potential for demand into these larger programs that have been delayed,” said Norwitt, who will become chief executive officer in early 2009.

Citi’s Suva believes Amphenol actually could see some benefit from an early withdrawal, as much military equipment there, in use longer than expected, will need to be refurbished.

One potential kicker to earnings could be commercial deployment of the Boeing 787 Dreamliner, now expected to begin in the second half of next year.

Analysts have not yet included revenue from Amphenol’s contribution to these planes, Citi’s Suva says. He believes Amphenol could realize an additional $12.5 million in 2009 revenue, translating into 2 cents a share and $30 million in 2010, adding a nickel to EPS.

Suva says Amphenol, along with Research In Motion, (RIMM) is his top pick among the 20 electronics companies he follows.

At RBC Capital, analyst Daryanani thinks Amphenol could surprise to the upside on future earnings, but that its market multiple — already dear — is unlikely to expand. Amphenol stock, around 49, is selling at more than 18 times Daryanani’s 2009 estimate of 2.70. “You are paying a premium for Amphenol,” Daryanani said. -

A Small Baseball Interlude

Eddy Elfenbein, July 28th, 2008 at 10:11 amI hate to break this to East Coast sportswriters, but neither the Yankees nor Red Sox are in first place. You’d never know it but the no-name Tampa Bay Rays are in first, and the Angels are probably better than the Rays.

Yesterday was Alex Rodriguez’s 33rd birthday. He now has 539 home runs, which is 12th on the all-time list (for the record, I count Hank Aaron’s 755 as the record). When Hank Aaron turned 33 after the 1966 season he had a total of 442 home runs, so A-Rod is 97 ahead of Hammerin Hank. Of course, Aaron still pounded out 313 home runs over the next 10 years so A-Rod has his work cut out for him—he’s still only about 71% of the way there.

Here’s the list:

1. Aaron 755

2. Ruth 714

3. Mays 660

4. Sosa 609

5. Griffey 607

6. Robinson 586

7. McGwire 583

8. Killebrew 573

9. Palmeiro 569

10. Reggie 563

11. Schmidt 548

12. A-Rod 539

Finally, my poor Nats were shut out for the third time in the last four games, and the fifteenth time this season. Ugh!

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His