Archive for January, 2009

-

Stryker Delivers

Eddy Elfenbein, January 9th, 2009 at 10:28 amThe company reaffirmed that it expects a 2008 profit, excluding special items, of $2.82 to $2.84 per share, an increase of 18 percent from 2007.

For 2009, the Kalamazoo, Michigan-based company forecast earnings of $3.12 to $3.22 per share, up 10 percent to 14 percent from expected 2008 results. Analysts’ average forecast is $3.15.Check out this trend in EPS growth:

2002: $0.88

2003: $1.12

2004: $1.43

2005: $1.75

2006: $2.02

2007: $2.40

2008: $2.82 to $2.84 (est)

2009: $3.12 to $3.22 (est) -

The Politics of Fear?

Eddy Elfenbein, January 9th, 2009 at 8:30 amRemember how George Bush used the “politics of fear” during a national crisis to “scare voters” into approving his pre-existing agenda? Maybe it’s just me. Anyway, here are some choice quotes from Obama’s speech yesterday:

We start 2009 in the midst of a crisis unlike any we have seen in our lifetime.

I don’t believe it’s too late to change course, but it will be if we don’t take dramatic action as soon as possible.

If nothing is done, this recession could linger for years.

We could lose a generation of potential and promise.

a bad situation could become dramatically worse.

we won’t get out of it by simply waiting for a better day to come, or relying on the worn-out dogmas of the past.

Only government can break the vicious cycles that are crippling our economy.

If we act with the urgency and seriousness that this moment requires.

we need to act boldly and act now to reverse these cycles

This must be a time when leaders in both parties put the urgent needs of our nation above our own narrow interests.

For every day we wait or point fingers or drag our feet, more Americans will lose their jobs. More families will lose their savings. More dreams will be deferred and denied. And our nation will sink deeper into a crisis that, at some point, we may not be able to reverse.

I know the scale of this plan is unprecedented, but so is the severity of our situation.

God Bless AmericaWow, I’m sold.

-

Anti-TARP Day

Eddy Elfenbein, January 9th, 2009 at 8:11 amToday seems to be Anti-TARP day. The first salvo comes from a congressional oversight committee:

The U.S. Treasury has failed to reveal its strategy for stabilizing the financial system, not answered questions asked by a government watchdog, and has done nothing to help struggling homeowners, a report being released Friday charges.

In the most scathing criticism yet of Treasury’s implementation of the $700 billion financial-rescue package, a draft report being issued by the five-member congressional oversight panel said there appear to be “significant gaps” in Treasury’s ability to track hundreds of billions of dollars of taxpayer money.

“The panel’s initial concerns about the [Troubled Asset Relief Program] have only grown, exacerbated by the shifting explanations of its purposes and the tools used by Treasury,” said the draft report, which found that the department has “not yet explained its strategy” for stabilizing the financial markets.

The report faults Treasury on a variety of fronts: having no ability to ensure banks lend the money they have received from the government; having no standards for measuring the success of the program; and for ignoring or offering incomplete answers to panel questions.Even harsher news comes from this Bloomberg article:

Henry Paulson may be the most powerful manager of money in the world and he still couldn’t do for taxpayers with the $700 billion bailout of American banks what Warren Buffett did for his shareholders in investing in Goldman Sachs Group Inc.

The Treasury secretary has made 174 purchases of banks’ preferred shares that include certificates to buy stock at a later date. He invested $10 billion in Goldman Sachs in October, twice as much as Buffett did the month before, yet gained warrants worth one-fourth as much as the billionaire, according to data compiled by Bloomberg. The Goldman Sachs terms were repeated in most of the other bank bailouts.

Paulson’s warrant deals may give U.S. taxpayers, who are funding the bailouts, less profit from any recovery in financial stocks than shareholders such as Goldman Sachs Chief Executive Officer Lloyd Blankfein and Saudi Arabian Prince Alwaleed bin Talal, owner of 4 percent of Citigroup Inc., said Simon Johnson, former chief economist for the International Monetary Fund.

The transactions are “just egregious,” said Johnson, a fellow at the Peterson Institute for International Economics in Washington. “You want to do it the way Warren does it.” -

Bank of England Cuts Rates to Lowest Level Since ’94

Eddy Elfenbein, January 8th, 2009 at 9:39 amThat would be 1694 when the bank was started:

The Bank of England cut the benchmark interest rate to the lowest since the central bank was founded in 1694 as policy makers tried to prevent the credit squeeze from deepening Britain’s recession.

The Monetary Policy Committee, led by Governor Mervyn King, trimmed the bank rate by a half point to 1.5 percent. The result matched the median forecast of 60 economists in a Bloomberg News survey. The pound rose against the euro and the dollar. -

Wallstrip Unstripped

Eddy Elfenbein, January 7th, 2009 at 10:04 pmWallstrip has come to the end of the road:

Like much of Wall Street, Wallstrip is pulling in its horns.

The finance-focused, comedy video Web site, which CBS’s interactive unit acquired in May 2007, won’t be producing any more episodes, PEhub.com said Wednesday, citing an undisclosed source. CBS plans to “take the DNA from WallStrip and apply it” to Bnet, another CBS property, the source told PEhub.

WallStrip, cheerily hosted by Julie Alexandria, produced three Web episodes a week, usually focusing on a company whose stock was trading at or near an all-time high. These days, few stocks fit that description, thanks to the sharp downturn in the market.

A source confirmed to DealBook on Wednesday that Wallstrip is scrapping its regular schedule, but details of the overhaul haven’t been announced yet. The Web site and the community will remain, the source said.

Howard Lindzon, the manager of a small hedge fund who helped create Wallstrip, told The New York Times in early 2007 that the Web site targets a space “between Jim Cramer and the bottom of the market.”

When it was acquired by CBS, one of Wallstrip’s producers said the Web site had yet to produce any self-sustaining ad revenue. It is unclear if it was ever profitable.This is sad; I’m a huge WallStrip fan.

-

The Strange Death of Risk Management

Eddy Elfenbein, January 7th, 2009 at 4:43 pmI just got around to reading Joe Nocera’s recent article on the life and death of risk management, and the titanically overrated blowhard Nassim Nicholas Taleb. The media tends to like these “Big Think” articles as it feeds into the Malcolm Gladwell-style of bring Big Ideas to the masses. Gladwell, in fact, was one of the first to highlight Taleb a few years ago in the New Yorker.

If you’re not familiar with Taleb, he has one idea and one idea alone. Actually, it’s not even his idea. The man who really impresses me Benoit Mandelbrot. Anyway, the idea is that stock returns don’t follow the normal distribution (the bell curve). That’s it—that’s the Big Think idea.

Here’s the deal: If stocks don’t follow a bell curve, then a lot of the ways we measure risk are flawed. For Taleb, of course, it’s much more than that. His idea (meaning Mandelbrot’s) is really an impossible to comprehend discourse on the human soul. In short, everyone else is a moron and only Taleb gets it.

He highlighted his idea in his two awful books, Fooled by Randomness and the Black Swan. I’ve actually read both books and I’m curious how many people who bought the books have actually read them. My hunch is that these could be part of the great unread books of the world. The reason is that the books are so bad that they’re barely literate. Taleb goes on and on about how he’s such an aesthete living in a world of philistines, yet he can’t write a single coherent page. Now expand that 400 pages. If people knew just how tedious these books are, I doubt they would receive so much praise.

Taleb and others now claim that Value at Risk, or VaR, played a large role in the credit mess. Sorry, that simply isn’t the case. Risk models are perfectly fine to use as long as you’re aware of the limitations. Every financial ratio or metric is like that. Just because it has some flaw is no reason to blame the movement of the economy on the misuse of math. Nocera points out that once Goldman Sachs saw problems with their VaR numbers, they adjusted. No big deal and Goldman is still in business today. Nocera quote one risk manager, “VaR is a peacetime statistic.” Exactly.

Here’s an excerpt from the article:“VaR was inevitable,” Gregg Berman of RiskMetrics said when I went to see him a few days later. He didn’t sound like an intellectual charlatan. His explanation of the utility of VaR — and its limitations — made a certain undeniable sense. He did, however, sound like somebody who was completely taken aback by the amount of blame placed on risk modeling since the financial crisis began.

“Obviously, we are big proponents of risk models,” he said. “But a computer does not do risk modeling. People do it. And people got overzealous and they stopped being careful. They took on too much leverage. And whether they had models that missed that, or they weren’t paying enough attention, I don’t know. But I do think that this was much more a failure of management than of risk management. I think blaming models for this would be very unfortunate because you are placing blame on a mathematical equation. You can’t blame math,” he added with some exasperation.Here’s another good snippet:

And yet, instead of dismissing VaR as worthless, most of the experts I talked to defended it. The issue, it seemed to me, was less what VaR did and did not do, but how you thought about it. Taleb says that because VaR didn’t measure the 1 percent, it was worse than useless — it was downright harmful. But most of the risk experts said there was a great deal to be said for being able to manage risk 99 percent of the time, however imperfectly, even though it meant you couldn’t account for the last 1 percent.

Howard has more. As usual, he’s bang on.

-

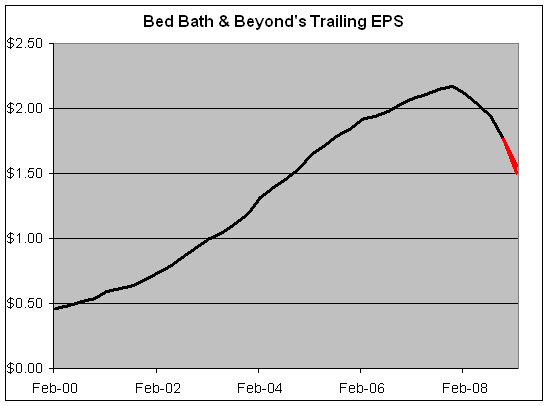

Bed, Bath & Beyond’s Q3 Earnings

Eddy Elfenbein, January 7th, 2009 at 4:20 pmFor their third-quarter (ending November 29), Bed Bath & Beyond (BBBY) just reported earnings of 34 cents a share. That’s pretty ugly, but honestly, it’s not bad considering the crappy environment they’re in. The earnings were a penny below the Street’s consensus, and the company earned 52 cents a share for last year’s Q3. Sales came in at $1.783 billion which was slightly below last year’s Q3. Same-store sales were just ugly, down 5.6%.

The company sees Q4 EPS coming in at 40 to 46 cents which is less than the 49 cents the Street was expecting.

Here are the earnings results going back a few years:Quarter Sales Gross Profit Operating Profit Net Profit EPS $356,633 $146,214 $28,015 $17,883 $0.06 $451,715 $185,570 $53,580 $33,247 $0.12 $480,145 $196,784 $50,607 $31,707 $0.11 $569,012 $238,233 $77,138 $48,392 $0.17 $459,163 $187,293 $36,339 $23,364 $0.08 $589,381 $241,284 $70,009 $43,578 $0.15 $602,004 $246,080 $64,592 $40,665 $0.14 $746,107 $311,802 $101,898 $64,315 $0.22 $575,833 $234,959 $45,602 $30,007 $0.10 $713,636 $291,342 $84,672 $53,954 $0.18 $759,438 $311,030 $83,749 $52,964 $0.18 $879,055 $370,235 $132,077 $82,674 $0.28 $776,798 $318,362 $72,701 $46,299 $0.15 $903,044 $370,335 $119,687 $75,459 $0.25 $936,030 $386,224 $119,228 $75,112 $0.25 $1,049,292 $443,626 $168,441 $105,309 $0.35 $893,868 $367,180 $90,450 $57,508 $0.19 $1,111,445 $459,145 $155,867 $97,208 $0.32 $1,174,740 $486,987 $161,459 $100,506 $0.33 $1,297,928 $563,352 $231,567 $144,248 $0.47 $1,100,917 $456,774 $128,707 $82,049 $0.27 $1,273,960 $530,829 $189,108 $120,008 $0.39 $1,305,155 $548,152 $190,978 $121,927 $0.40 $1,467,646 $650,546 $283,621 $180,980 $0.59 $1,244,421 $520,781 $150,884 $98,903 $0.33 $1,431,182 $601,784 $217,877 $141,402 $0.47 $1,448,680 $615,363 $205,493 $134,620 $0.45 $1,685,279 $747,820 $304,917 $197,922 $0.67 $1,395,963 $590,098 $148,750 $100,431 $0.35 $1,607,239 $678,249 $219,622 $145,535 $0.51 $1,619,240 $704,073 $211,134 $142,436 $0.50 $1,994,987 $862,982 $309,895 $205,842 $0.72 $1,553,293 $646,109 $154,391 $104,647 $0.38 $1,767,716 $732,158 $211,037 $147,008 $0.55 $1,794,747 $747,866 $203,152 $138,232 $0.52 $1,933,186 $799,098 $259,442 $172,921 $0.66 $1,648,491 $656,000 $118,819 $76,777 $0.30 $1,853,892 $739,321 $187,421 $119,268 $0.46 $1,782,683 $692,857 $136,374 $87,700 $0.34 Here’s their trailing four-quarter earnings-per-share. The two red lines show the upper and lower band of the company’s projection.

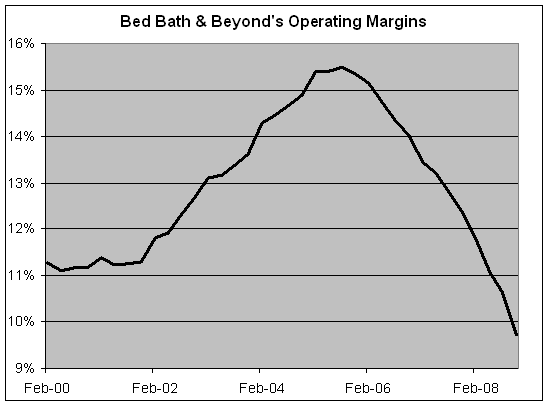

It’s not hard to find the squeaky wheel. Take at look at their operating margins:

That’s based on trailing four quarter numbers. This means the company is doing a lot of price-cutting. -

The End of Times

Eddy Elfenbein, January 7th, 2009 at 11:45 amMichael Hirschorn says the New York Times could go bankrupt, by May.

It’s certainly plausible. Earnings reports released by the New York Times Company in October indicate that drastic measures will have to be taken over the next five months or the paper will default on some $400million in debt. With more than $1billion in debt already on the books, only $46million in cash reserves as of October, and no clear way to tap into the capital markets (the company’s debt was recently reduced to junk status), the paper’s future doesn’t look good.

“As part of our analysis of our uses of cash, we are evaluating future financing arrangements,” the Times Company announced blandly in October, referring to the crunch it will face in May. “Based on the conversations we have had with lenders, we expect that we will be able to manage our debt and credit obligations as they mature.” This prompted Henry Blodget, whose Web site, Silicon Alley Insider, has offered the smartest ongoing analysis of the company’s travails, to write: “‘We expect that we will be able to manage’? Translation: There’s a possibility that we won’t be able to manage.” -

Mean Automakers Dash Nation’s Hope For Flying Cars

Eddy Elfenbein, January 6th, 2009 at 4:56 pm -

Earnings Preview: Bed Bath & Beyond

Eddy Elfenbein, January 6th, 2009 at 1:20 pmBed Bath & Beyond Inc. reports results for its fiscal third quarter on Wednesday. The following is a summary of key developments and analyst opinion related to the period.

OVERVIEW: In early December, Bed Bath & Beyond pre-released results for the third quarter, saying same-store sales slipped amid a tough economic climate and liquidation sales by a major competitor.

The Union, N.J.-based housewares retailer it expects earnings to range between 31 cents and 35 cents per share for the quarter ended Nov. 29. That’s down from previous guidance of 41 cents to 47 cents a share the company gave in September. It also represents a drop from 2007, when the company earned 52 cents a share in the same period.

The company said its net sales for the quarter fell 0.7 percent from the same period the previous year, when it reported sales of $1.79 billion.

Same-store sales for the quarter declined about 5.6 percent. Same-store sales, or sales at stores open at least a year, are a key indicator of a retailer’s health because they measure revenue at existing locations rather than newly opened ones.

During the quarter, the retail chain saw shares sink to an eight-year intraday low as government figures show home furnishing sales fell.

BY THE NUMBERS: Analysts polled by Thomson Reuters estimate a profit of 33 cents per share on revenue of $1.79 billion for the quarter.

ANALYST TAKE: After the retailer pre-released lower-than-expected third quarter figures in early December, analysts said the company was facing increasing pressure from a difficult sales environment and the ongoing bankruptcy liquidation sales of items by competitor Linens ‘N Things.

“While we expect consumer spending will likely remain weak, Bed Bath & Beyond may well be one of the few retailers to show earnings growth next year,” SunTrust Robinson Humphrey analyst David Magee told investors in early December. “Moreover, once the macro environment improves, Bed Bath & Beyond should emerge stronger than most and could benefit from some ongoing consolidation in the space along the way.”

WHAT’S AHEAD: Investors will be looking for an update on how the company’s holiday sales fared and more details about what executives expects business trends to be in the coming year.

STOCK PERFORMANCE: During the quarter, which ended Nov. 29, shares fell about 34 percent to end the period at $20.29.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His