Archive for February, 2009

-

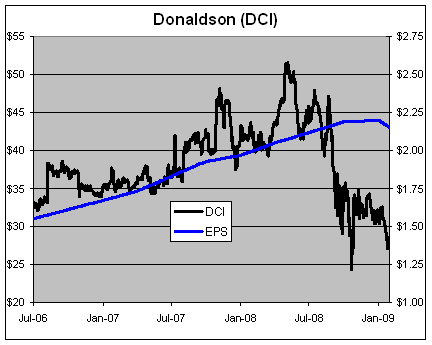

Donaldson’s Earnings Streak Set to End

Eddy Elfenbein, February 26th, 2009 at 1:26 pmToday is a sad day for lovers of high-quality stocks. Donaldson (DCI) lowered its 2009 EPS forecast to a range of $1.70 to $1.90, which means that the company will almost certainly end its 19-year streak of delivering record earnings.

Donaldson isn’t very well known, but it’s a remarkable company. Their market cap is about $2 billion and they’re in the S&P 400 Mid-Cap Index (^MID). Donaldson is the filtration business which is about as dull as they come.

Last year, the company earned $2.12 a share and the outlook for this year (the fiscal year ends in July) was a range of $2.16 to $2.36. So even before today, the streak looked to be in jeopardy.

For the second quarter, Donaldson earned 43 cents a share which was a mere penny a share more than last year’s Q2. Net income was actually down, but the company has fewer shares outstanding.

I’m not particularly worried about Donaldson. I don’t think they’re in any more trouble than anyone else. I was also happy to see this nugget from their press release:In addition, since a significant portion of our pay is ‘at risk’ and paid based on our actual financial performance, executive officer compensation is expected to be reduced by 30 to 50 percent this year due to lower incentive payouts. In addition, officer base salaries have been frozen at January 2008 levels.

Here’s a look at Donaldson’s stock along with its EPS line in blue. The two axes are scaled at 20 to 1.

Here’s the earnings streak:Year………….Sales……………..EPS

1990…………$422.9……………$0.19

1991…………$457.7……………$0.21

1992…………$482.1……………$0.23

1993…………$533.3……………$0.26

1994…………$593.5……………$0.30

1995…………$704.0……………$0.37

1996…………$758.6……………$0.42

1997…………$833.3……………$0.50

1998…………$940.4……………$0.57

1999…………$944.1……………$0.66

2000…………$1,092.3…………$0.76

2001…………$1,137.0…………$0.83

2002…………$1,126.0…………$0.95

2003…………$1,218.3…………$1.05

2004…………$1,415.0…………$1.18

2005…………$1,595.7…………$1.27

2006…………$1,694.3…………$1.55

2007…………$1,918.8…………$1.83

2008…………$2,232.5…………$2.12 -

WSJ: Stocks Drop to 50% of Peak

Eddy Elfenbein, February 25th, 2009 at 4:34 pmThe Wall Street Journal notes that the S&P 500 is now half of its peak. This is the only the second time in history that has happen. The first time was the grandaddy — 1929.

Bespoke writes:Ultimately in the bear that started in 1929, the S&P 500 dropped a whopping 86.19% from its all-time high. This low occurred 679 trading days after the all-time high was reached, or about two years and nine months. The current decline has lasted one year and four months.

But by far the most depressing aspect of the 50%+ decline back in the 1930s was how long it took for the index to make a new all-time high. Following the peak in 1929, the S&P 500 went 6,251 trading days before hitting a new all-time high 25 years later.I’m a glass-is-half-full kind of guy so can’t we turn that around? If the market does fall by 86%, think of the buying opportunity!

-

P/E Ratios Don’t Need to Be Cyclically Adjusted

Eddy Elfenbein, February 25th, 2009 at 1:40 pmThe Cyclically Adjusted Price/Earnings Ratio (or CAPE) has been getting a lot of attention lately. It was originally developed by Benjamin Graham, and Robert Shiller has been the latest proponent.

In today’s Financial Times, John Authers writes:Long-term measures of value are also finely poised. Take the cyclical price/earnings ratio, which compares share prices with average earnings during the past decade, rather than to the most recent year’s earnings. This evens out bumps in earnings multiples caused by the profit cycle, and has proved to be a great market timing vehicle – highs and lows for this metric have overlapped almost perfectly with highs and lows for the market.

Robert Shiller, the Yale university economist, has done much to popularise the measure. According to his calculations, it makes US stocks look distinctly cheap. The cyclical p/e, at 13.38 entering this week, is below its average since 1870 of 16.34. It is also at its lowest since 1986.

However, this should not be treated as a short-term buying signal because cyclical p/es have dropped to as low as 6 at the bottom of previous bear markets. This would imply that stocks could fall 50 per cent more, before hitting bottom.I don’t think adjusting earnings multiples for the economic cycle is a sound idea. The obvious reason is that stock prices are themselves cyclical. I dispute Authors points that CAPE has been “a great market timing vehicle.” In fact, I think it’s been pretty bad.

According to data off Professor Shiller’s website, when the market’s CAPE was below 21, the market returned 1.35% annualized and adjusted for inflation. When it was above 21, the market did slightly better, growing by 1.82% annualized and adjusted for inflation.

For the unadjusted 12-month P/E Ratio, the market grew by 1.79% when it was below 21, and it contracted by -1.29% when it was above 21. In other words, the traditional P/E Ratio told you a lot more about how well the market was valued.

Neither metric, however, comes close to the easiest—momentum. If the market fell in the previous month, then it has continued to fall by an annualized and adjusted for inflation rate of -8.36%. If the market has been rising, then it continues to grow by a rate of 10.09%. -

Ditch the Home Mortgage Deduction?

Eddy Elfenbein, February 25th, 2009 at 12:10 pmEd Glaeser says it’s time to do away with the home mortgage interest deduction. His five reasons are:

Problem #1: Subsidizing interest payments encourages people to leverage themselves to the hilt to bet on housing markets.

Problem #2: The deduction pushes up prices in places where the supply of new homes is constrained, as it is in many coastal markets.

Problem #3: The deduction is wildly regressive.

Problem #4: The deduction encourages people to buy larger, single-family detached homes, and that increases carbon emissions and pushes people out of cities.

Problem #5: The home mortgage interest deduction is poorly designed to encourage homeownership, which is, after all, the alleged desideratum. -

The Wisdom of John Pilger

Eddy Elfenbein, February 25th, 2009 at 10:54 amTwo quotes from the vanguard of the proletariat:

The New Statesmen, November 15, 1999:

“No one can doubt [the Milosevic’s regime’s] cruelty and atrocities, but comparisons with the Third Reich are ridiculous.”

The Guardian, February 3, 2003:

“The current American elite is the Third Reich of our times.”

Oliver Kamm has more. -

Eaton Vance’s Earnings Plunge

Eddy Elfenbein, February 25th, 2009 at 9:51 amShares of Eaton Vance (EV) are up modestly this morning. The mutual fund company reported Q1 earnings of 21 cents a share, which is a big drop from the 46 cents it made during last year’s first quarter. The silver lining is that Wall Street was expecting 19 cents a share. Revenues dropped from 28%, from $289.8 million to $209.5 million. This is going to be a rough year for Eaton Vance, but few stocks have the long-term record they do. The stock is worth holding, and it also carries a nice 4% yield.

-

Dogbert Keeps It Real

Eddy Elfenbein, February 25th, 2009 at 9:22 am

-

“Well That Day of Reckoning Has Arrived”

Eddy Elfenbein, February 25th, 2009 at 12:46 amThe president lays out his plans:

First, we are creating a new lending fund that represents the largest effort ever to help provide auto loans, college loans, and small business loans to the consumers and entrepreneurs who keep this economy running.

Second, we have launched a housing plan that will help responsible families facing the threat of foreclosure lower their monthly payments and re-finance their mortgages. It’s a plan that won’t help speculators or that neighbor down the street who bought a house he could never hope to afford, but it will help millions of Americans who are struggling with declining home values – Americans who will now be able to take advantage of the lower interest rates that this plan has already helped bring about. In fact, the average family who re-finances today can save nearly $2000 per year on their mortgage.

Third, we will act with the full force of the federal government to ensure that the major banks that Americans depend on have enough confidence and enough money to lend even in more difficult times. And when we learn that a major bank has serious problems, we will hold accountable those responsible, force the necessary adjustments, provide the support to clean up their balance sheets, and assure the continuity of a strong, viable institution that can serve our people and our economy.

I understand that on any given day, Wall Street may be more comforted by an approach that gives banks bailouts with no strings attached, and that holds nobody accountable for their reckless decisions. But such an approach won’t solve the problem. And our goal is to quicken the day when we re-start lending to the American people and American business and end this crisis once and for all.

I intend to hold these banks fully accountable for the assistance they receive, and this time, they will have to clearly demonstrate how taxpayer dollars result in more lending for the American taxpayer. This time, CEOs won’t be able to use taxpayer money to pad their paychecks or buy fancy drapes or disappear on a private jet. Those days are over.

Still, this plan will require significant resources from the federal government – and yes, probably more than we’ve already set aside. But while the cost of action will be great, I can assure you that the cost of inaction will be far greater, for it could result in an economy that sputters along for not months or years, but perhaps a decade. That would be worse for our deficit, worse for business, worse for you, and worse for the next generation. And I refuse to let that happen.

I understand that when the last administration asked this Congress to provide assistance for struggling banks, Democrats and Republicans alike were infuriated by the mismanagement and results that followed. So were the American taxpayers. So was I.

So I know how unpopular it is to be seen as helping banks right now, especially when everyone is suffering in part from their bad decisions. I promise you – I get it. -

Home Prices Post Biggest Drop in 21 Years

Eddy Elfenbein, February 25th, 2009 at 12:42 amFrom BusinessWeek:

The S&P/Case-Shiller U.S. National Home Price Index plunged 18.2% during the final quarter of 2008, the biggest annual decline in the closely watched index’s 21-year history.

Separately, for the month of December alone the Case-Shiller 20-City Composite Index fell 18.5% compared with the previous December, also a record decline. The most severe declines were in Phoenix, Las Vegas, and San Francisco, which all dropped by more than 30% in December compared with December 2007.

But the financial crisis has helped to spread the pain across the nation. Other cities that were holding up relatively well until recently are now seeing a quickening pace of declines. The year-over-year price decline in the New York metro area, which is at the center of the financial meltdown, was 9.2% in December, compared with 8.6% in November and 7.7% in October. Home prices in Charlotte, a major banking hub, fell by 7.2% in December. In October, Charlotte prices fell at just 4.4% compared with a year earlier. And home prices were actually increasing on an annual basis as recently as March 2007. -

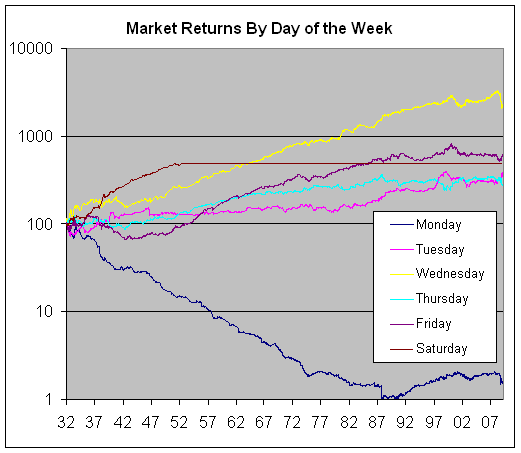

Market Returns by Days of the Week

Eddy Elfenbein, February 25th, 2009 at 12:06 amHere’s a look at market returns by days of the week. I did this last year but now I have more data including Saturdays. There was actually trading on Saturdays up to the early 1950s.

Here’s the breakdown: From 1932 through Monday, Wednesday was the best day of the week. In fact, Wednesday beat the four days (and Saturday) combined. Not including dividends, the S&P 500 returned 2,179% on Wednesdays, 502% on Thursdays, 244% on Tuesdays, 175% on Thursdays and an ugly -98.5% on Mondays.

Let me add what I hope is an obvious point—these stats don’t mean anything. It’s just fun trivia. You really can’t build a workable trading strategy around these numbers. We’re also talking about results of nearly 80 years of data. Even starting 20 years ago, Monday suddenly becomes the second-best day.

A few other points to mention. When Saturday trading was around, it was a great day. The market returned 389% on Saturdays from 1932 to 1952. Plus, even when there was Saturday trading, the market was often closed on Saturdays over the summer.

Statistically, the only really noticeable standout is the awful performance on Mondays. As I said, even that has diminished in recent years.

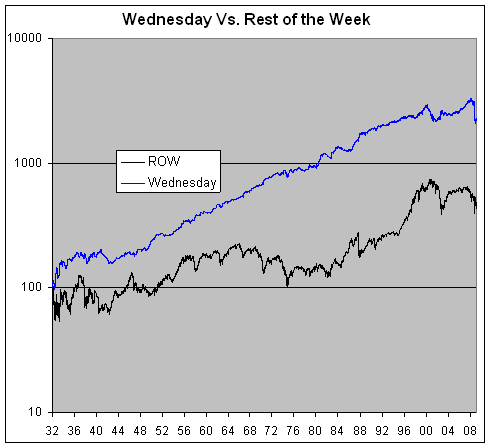

As strong as Wednesdays have been, they recently came through an awful stretch. The S&P 500 dropped on 10 straight Wednesdays this past fall. And they were big drops—the losing streak knocked one-third off the Wednesday’s historic return.

The S&P 500 is in the negative on Monday, Tuesday, Thursday and Saturday. The market’s entire return has come just on Wednesday and Friday. Here’s a look at Wednesday against the rest of the week:

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His