Archive for September, 2009

-

Just In Case No One Remembers

Eddy Elfenbein, September 17th, 2009 at 12:02 amFrom almost the exact bottom, March 12, 2009, Nouriel Roubini wrote a column in Forbes “How Low Can The Stock Markets Go? The answer: Lower … much lower.”

To be clear, I’m not trying to paint Roubini in a bad light. I’m trying to point out the folly of market forecasts. -

Fourth Downs: Kick, Punt or Go for It?

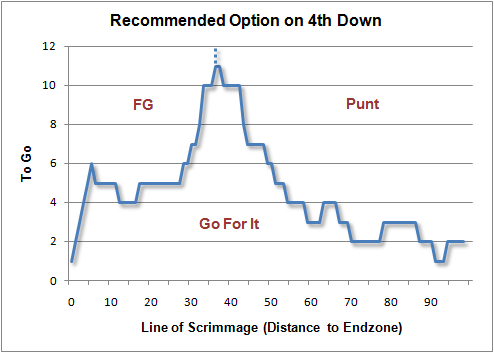

Eddy Elfenbein, September 16th, 2009 at 7:26 pmBrian Burke runs the excellent Advanced NFL Stats blog. He combs through mountains of data to uncover interesting aspects of the game.

Burke recently completed a big study looking at fourth downs and the advantages of going for it versus kicking or punting. As it turns out, football teams ought to go for it on fourth downs far more than they do.

After crunching tons of data, this is the chart Burke came up with showing the recommended option of what to do on fourth down.

The charts shows that football coaches have been far too risk averse. In fact, if they were to follow the advice on Burke’s chart, I think the number of field goal attempts would plummet.

The lingering question is why are coaches so conservative? Perhaps it has to due with the fact that the future points you might get are abstract, whereas punting down field is obvious.

Bear in mind that the advantage of going for it on fourth down isn’t that you’ll make the first down. Instead, it’s the net result of giving up the ball versus surrendering the ball with a punt farther down field. There are lots of variables in play.

There is a financial equivalent (I’m sure you were waiting). What Burke’s study is really looking is risk management. That’s what a lot of investing is about as well. The question investors need to ask isn’t if Dell is a good investment. Instead, is Dell a good investment given its risk compared with other investments with similar risk?

Behavioral economists have shown that we’re not so good at measuring probabilities. We’re far more likely to horde what we have rather than risk an uncertain payoff (See here where I asked: Which would you choose; $1,000 guaranteed or a 50% chance at making $3,000?)

For many years now, gold has outperformed stocks and Treasuries have beaten stocks for decades. According to conventional wisdom, that’s not supposed to happen but it did. Punting on fourth down is conventional wisdom so it will take a brave coach to be the first one to challenge this orthodoxy. -

Another New High

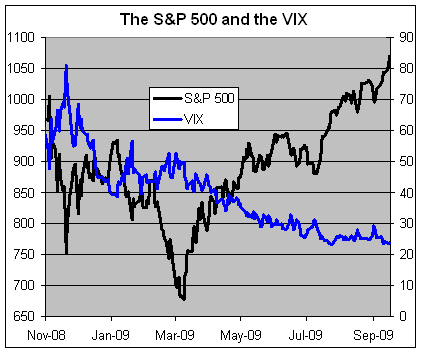

Eddy Elfenbein, September 16th, 2009 at 4:46 pmThe market was up yet again today. This was the eighth rally in the last nine sessions. I’ve been a fan of this rally, and I’ve had a lot of fun teasing the doubters, but it’s started to look tired to me (I mentioned I sold Dell earlier today).

For the year, the S&P 500 is now up over 18% not including dividends, and it’s up 58% since the March 9th closing low. Our Buy List has done even better, up 36.3% for the year and 80.3% since March 9th.

The VIX, or volatility index, got close to a new 52-week low today. Interestingly, the VIX rose today even though it usually falls on days when stocks rally. In October, the VIX came close to breaking 90. Today, it’s at 23.

Here’s a look at the S&P 500 (black line, right scale) and the VIX (blue line, right scale):

-

Technical Number to Watch

Eddy Elfenbein, September 16th, 2009 at 3:04 pmWhen the S&P 500 hits 1,066.86, that’s exactly a 60% gain from the March 6 intra-day low.

-

Bed Bath & Beyond Makes New High

Eddy Elfenbein, September 16th, 2009 at 2:54 pmBed Bath & Beyond (BBBY) just broke out to a new 52-week high today. The stock has been as high as $38.38 in today’s trading. In July, Barron’s said that stock was headed to $40 and it looks like they might be right. At the time of their call, BBBY was at $32.65.

One of the new stocks I added to this year’s Buy List was Baxter International (BAX). I’m pleased with how the company has performed although the share price hasn’t done that well. It’s currently up about 3% this year. The company beat earnings estimates by two cents a share in January, April and July. That’s a good sign.

The company said today that its goal is to grow EPS by 11% to 13% over the next five years. For this year, they see EPS in a range of $3.76 to $3.80. That’s what they had said in July when they raised guidance slightly. They also raised guidance in April (notice a trend here). I’m sticking with Baxter. -

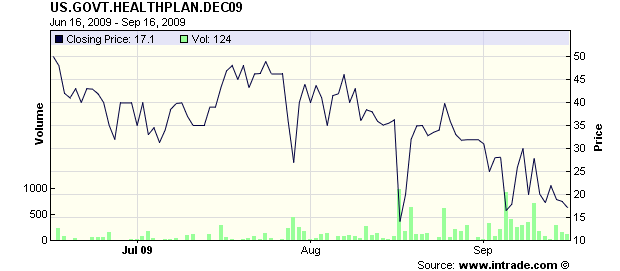

Intrade on Healthcare Reform

Eddy Elfenbein, September 16th, 2009 at 1:07 pmThe futures market doesn’t expect anything to happen before the end of the year:

-

Sold My Position in Dell

Eddy Elfenbein, September 16th, 2009 at 12:56 pmI used to be a big fan of Dell (DELL) which was a horrible mistake on my part. Nevertheless, any investor will have good ideas and dumb ideas. This was a dumb one.

I initially bought Dell in late 2005 around $30.50 a share and rode it all the way down to $8 earlier this year. When you’re down that much, the temptation is to say “Screw this” and sell out at any price. Fortunately, I fought that and held on for a bit more.

I decided to come up with a fair price and wait until Dell came within range. The fair price I chose was $15 a share. The stock recently hit it though I held out for a little more and sold today at $17.

It’s easy to talk about your winners but I wanted to share some of my big losers as well. Still, the lesson is the same and that’s not to let your emotions get the best of you. -

Archbishop of Canterbury: Bankers Have Failed to Repent

Eddy Elfenbein, September 16th, 2009 at 10:31 amThe Archbishop of Canterbury, Dr. Rowan Williams, has said that bankers have failed to repent for the financial crisis.

Dr Williams said: “There hasn’t been a feeling of closure about what happened last year. There hasn’t been what I would, as a Christian, call repentance. We haven’t heard people saying ‘well actually, no, we got it wrong and the whole fundamental principle on which we worked was unreal, empty’.”

Asked if the City was returning to business as usual he said: “I worry. I feel that’s precisely what I call the ‘lack of closure’ coming home to roost. It’s a failure to name what was wrong. To name that, what I called last year ‘idolatry’, that projecting of reality and substance onto things that don’t have them.”Dr. Williams has already shown himself to be economically illiterate (“Every transaction in the developed economies of the West can be interpreted as an act of aggression against the economic losers in the worldwide game”), but this last statement is truly bizarre. More importantly, it has zero understanding of the credit crisis. As Oliver Kamm points out: “You could have saints and archangels trading derivatives, but if their risk models are wrong then you’ll get the same result.”

-

One Year Ago Today

Eddy Elfenbein, September 15th, 2009 at 12:21 pmMe one year ago today:

The Fed’s Suez Crisis

Something that struck me about Lehman’s demise is how little power the Federal Reserve really has. Don’t get me wrong, the Fed is darn powerful, but it’s not all-knowing and all-seeing, despite what some folks think. The Fed is powerful because people think it’s powerful.

Analysts hang on every word in a statement or testimony, but in the case of Lehman Brothers (LEH), the Fed really couldn’t do much. Wall Street basically stood up to the Fed and the central bank was exposed. Since Bear was the first, the Fed can open its mouth and get its way. But the Fed can’t make the weaker argument the stronger, and that’s what was needed with Lehman.

I’d say the Lehman story was a combination of too much debt—at one time they were leverage 40-to-1, they didn’t know what they owned, and they refused to listen to any criticism. To top it off, they had horrible luck too. That’s not a good combination.

With Level 3 assets (these are basically assets that can’t be priced easily so we have to trust Lehman for the price), Lehman once claim they their Level 3 stuff was up 9%, even though the market was down by 10%. When people called them on it, Lehman got mad and blamed the shorts. That’s just arrogance. Then they spent something like $22 billion on Archstone? I mean, what the hell? Talk about the wrong price, the wrong industry at the wrong time. Aside from that, it was a great deal!

Einhirn and other shorts said they didn’t know what their stuff was worth and they were undercapitalized. Fuld & Co. just refused to listen. I don’t think they’re crooks at all, they sincerely believed in what they were doing. Until the end, the company was offering assurance to investors.

With Bear and Lehman we often heard about counterparty risk. Well, that theory got shot down with Lehman. I’m going to go on the idea that the reason there wasn’t a deal for Lehman is that no one wanted one. If someone wanted, it would have happened. Novel thinking I know. But it tells us that the Street is hardly concerned about counterparty risk. JPM was concerned about with Bear because it was mostly their risk.

I heard Hank Paulson talk about bringing stability to the markets. Yeah, right. That’s basically like the flea giving orders to the dog. The Fed and the Treasury do not have this thing contained. If the housing market recovers, then the problem goes away. It’s as simple as that. -

Boo Hoo Column of the Day

Eddy Elfenbein, September 15th, 2009 at 12:17 pmThe following is from Jane Pedreira, a former senior Veep at Lehman:

I was robbed first by Ben Bernanke, the Federal Reserve chairman, and Henry Paulson, the former Treasury secretary, who refused to support a sale of the company, and later by the bankruptcy judge who approved the sale of Lehman to Barclays for peanuts.

I am still unable to pay all of my bills. I know the public at large doesn’t have sympathy for Wall Street employees, but did I deserve to be robbed because of the mistakes of others?Oh brother.

(Via: Carney)

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His {kind=link}