Archive for September, 2009

-

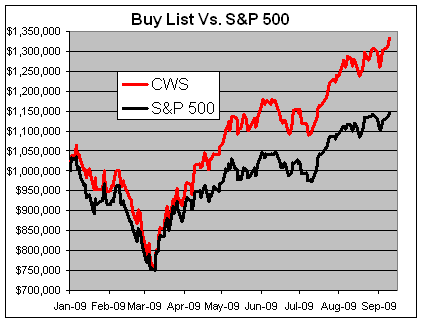

The Buy List YTD

Eddy Elfenbein, September 10th, 2009 at 12:14 pmThe CWS Buy List continues to perform very well. Through yesterday’s close, the Buy List is 33.31% compared with 14.41% for the S&P 500 (neither figures includes dividends). That’s a YTD high for the Buy List and it’s a high for its outperformance against the S&P 500 which now stands at 18.9%.

The Buy List was helped yesterday by Cognizant Technology Solutions (CTSH) which said that positive demand trends are continuing into the third quarter. The stock is now a double for us. Also, Nicholas Financial (NICK) announced the opening of a new branch in Akron, Ohio. -

Myths of the Credit Crisis

Eddy Elfenbein, September 9th, 2009 at 2:02 pmArnold Kling has a good article looking at some myths of the financial crisis. One that he tackles is the idea that there was too little regulation. Instead, Kling asserts that regulation was one of the problems.

The myth is that the regulators failed to focus on the systemic implications of financial innovation. The reality is that the regulators were keenly interested in systemic risk. However, like their counterparts in the financial industry, the regulators thought that the innovations had reduced systemic risk. The problem was not that regulators lacked a mandate to address systemic risk. What they lacked was judgment and insight.

-

Greenspan: Market crisis “will happen again” Me: Greenspan “will not happen again.”

Eddy Elfenbein, September 9th, 2009 at 11:38 am“The crisis will happen again but it will be different,” he told BBC Two’s The Love of Money series.

He added that he had predicted the crash would come as a reaction to a long period of prosperity.

But while it may take time and be a difficult process, the global economy would eventually “get through it”, Mr Greenspan added.

“They [financial crises] are all different, but they have one fundamental source,” he said.

“That is the unquenchable capability of human beings when confronted with long periods of prosperity to presume that it will continue.”

Speaking a year after the collapse of US investment bank Lehman Brothers, which was followed by a worldwide financial crisis and global recession, Mr Greenspan described the behaviour as “human nature”.Follow link to video.

-

From Wall Street to Seasame Street

Eddy Elfenbein, September 9th, 2009 at 10:46 amIt’s getting rough out there. Elmo’s mom (who’s apparently from Virginia) loses her job.

Visit msnbc.com for Breaking News, World News, and News about the Economy

Next up, a discussion on the national debt with Count Von Count. This may take awhile.

-

China alarmed by US money printing

Eddy Elfenbein, September 8th, 2009 at 3:54 pmThe good news is that someone is alarmed by U.S. monetary policy. The bad news is that it’s a top member of the Chinese Communist hierarchy.

Cheng Siwei, former vice-chairman of the Standing Committee and now head of China’s green energy drive, said Beijing was dismayed by the Fed’s recourse to “credit easing”.

“We hope there will be a change in monetary policy as soon as they have positive growth again,” he said at the Ambrosetti Workshop, a policy gathering on Lake Como.

“If they keep printing money to buy bonds it will lead to inflation, and after a year or two the dollar will fall hard. Most of our foreign reserves are in US bonds and this is very difficult to change, so we will diversify incremental reserves into euros, yen, and other currencies,” he said.

China’s reserves are more than – $2 trillion, the world’s largest. -

51.04% of all trading on the NASDAQ Friday was short selling

Eddy Elfenbein, September 8th, 2009 at 12:31 pmThere were 6,516 stocks with daily short volume reported and total NASDAQ trading volume of 1,318,772,463 shares. Total Daily Short Volume was 673,135,041 shares. 51.04% of all trading on the NASDAQ Friday was short selling.

-

UN wants new global currency to replace dollar

Eddy Elfenbein, September 8th, 2009 at 11:05 amThis is a pipe dream:

In a radical report, the UN Conference on Trade and Development (UNCTAD) has said the system of currencies and capital rules which binds the world economy is not working properly, and was largely responsible for the financial and economic crises.

It added that the present system, under which the dollar acts as the world’s reserve currency , should be subject to a wholesale reconsideration.

Although a number of countries, including China and Russia, have suggested replacing the dollar as the world’s reserve currency, the UNCTAD report is the first time a major multinational institution has posited such a suggestion.

In essence, the report calls for a new Bretton Woods-style system of managed international exchange rates, meaning central banks would be forced to intervene and either support or push down their currencies depending on how the rest of the world economy is behaving.

The proposals would also imply that surplus nations such as China and Germany should stimulate their economies further in order to cut their own imbalances, rather than, as in the present system, deficit nations such as the UK and US having to take the main burden of readjustment.

“Replacing the dollar with an artificial currency would solve some of the problems related to the potential of countries running large deficits and would help stability,” said Detlef Kotte, one of the report’s authors. “But you will also need a system of managed exchange rates. Countries should keep real exchange rates [adjusted for inflation] stable. Central banks would have to intervene and if not they would have to be told to do so by a multilateral institution such as the International Monetary Fund.”

The proposals, included in UNCTAD’s annual Trade and Development Report, amount to the most radical suggestions for redesigning the global monetary system.

Although many economists have pointed out that the economic crisis owed more to the malfunctioning of the post-Bretton Woods system, until now no major institution, including the G20 , has come up with an alternative. -

Buffett Sees More Trouble Ahead

Eddy Elfenbein, September 8th, 2009 at 10:25 amThe New York Times catches up with the Oracle of Omaha:

After boldly buying when so many were selling assets, his conglomerate, Berkshire Hathaway, is pulling back, buying fewer stocks while investing in corporate and government debt. And Mr. Buffett is warning that the economy, though on the mend, remains deeply troubled.

“We are not out of problems yet,” Mr. Buffett said last week in an interview, in which he reflected on the lessons of the last 12 months. “We have got to get the sputtering economy back so it is functioning as it should be.”

Still, Mr. Buffett hardly sounded shellshocked in the wake of what he once called the financial equivalent of Pearl Harbor. (An estimated net worth of $37 billion would be a balm to anyone’s psyche.) -

How the SEC Failed

Eddy Elfenbein, September 8th, 2009 at 10:09 amLarry Ribstein points us to the SEC’s report on Bernie Madoff and it’s absolutely scathing. Here’s a sample:

The investigation that arose from the most detailed complaint provided to the SEC, which explicitly stated it was “highly likely” that “Madoffwas operating a Ponzi scheme,” never really investigated the possibility of a Ponzi scheme. The relatively inexperienced Enforcement staff failed to appreciate the significance ofthe analysis in the complaint, and almost immediately expressed skepticism and disbelief. Most of their investigation was directed at determining whether Madoff should register as an investment adviser or whether Madoff’s hedge fund investors’ disclosures were adequate.

As with the examinations, the Enforcement staff almost immediately caught Madoff in lies and misrepresentations, but failed to follow up on inconsistencies. They rebuffed offers of additional evidence from the complainant, and were confused about certain critical and fundamental aspects of Madoff’s operations. When Madoff provided evasive or contradictory answers to important questions in testimony, they simply accepted as plausible his explanations.Ouch! When you see the sheer incompetence of the government, it ought to serve as a great refutation to conspiracy theorists. Yet I have a feeling that logic and facts won’t make a dent in their efforts.

Bonus: Madoffs get $13,800 property tax rebate -

Oliver Stone Is Back

Eddy Elfenbein, September 8th, 2009 at 8:28 amThe New York Times looks at the return of Oliver Stone:

While Mr. Stone’s youth was steeped in the ways of finance, thanks to his father’s profession, he did not inherit a facility for such matters. He did poorly in economics at Yale, and turned to filmmaking. He has spent the last several months researching the financial collapse by reading and by meeting with executives and academics.

Earlier in the summer he brought Mr. LaBeouf to a cocktail party organized by Nouriel Roubini, a New York University economics professor and chairman of a consulting firm, and held in rented space at the Maritime Hotel in Chelsea. There Mr. Stone and Mr. LaBeouf discussed the financial collapse with hedge fund managers who are clients of Mr. Roubini’s firm.

“In this financial crisis it was the traditional banks and the investment banks that had a larger role in doing stupid and silly things than the hedge funds,” said Mr. Roubini, who earned acclaim for being early in predicting the financial crisis. (Mr. Stone offered Mr. Roubini a small role in the film as a hedge fund manager.)I’m not surprised to hear that Stone did poorly in economics. It doesn’t sound like he’s gotten much better. The late Pauline Kael said she despised his movies. I’m not sure why anyone takes Stone seriously:

“They control culture, they control ideas. And I think the revolt of September 11th was about ‘Fuck you! Fuck your order—’ ”

“Excuse me,” a fellow-panelist, Christopher Hitchens, said. ” ‘Revolt’?”

“Whatever you want to call it,” Stone said.

“It was state-supported mass murder, using civilians as missiles,” said Hitchens, a columnist for Vanity Fair and The Nation.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His