Archive for March, 2010

-

We’re Up 11.82% in Six Weeks

Eddy Elfenbein, March 22nd, 2010 at 3:58 pmToday was an outstanding day for our Buy List. The average of our 20 stocks was up 0.95% which nearly doubled the S&P’s gain of 0.51%. Seventeen of our 20 stocks closed higher. Ten were up more than 1% and two were up more than 2%.

Since the near-term low on February 8, the S&P 500 is up 10.32% but we’re up 11.82%. That’s a 150 basis point outperformance in just six weeks.

Barron’s just noted that Gilead (GILD) is going for “only 12 times expected-forward earnings. The company has plenty of free cash and impressive growth.” -

Gene Simmons on Estate Planning

Eddy Elfenbein, March 22nd, 2010 at 1:59 pmFrom Bloomberg. Yes, Bloomberg:

Gene Simmons, singer and bassist for the rock band Kiss, said high-net-worth individuals should better prepare to protect their wealth after they die.

“You should know what your choices are in planning your estate,” said Simmons, co-founder of Cool Springs Life Equity Strategy, in an interview with Bloomberg Television in New York today.

Simmons said his company can benefit athletes and entertainers who earned fortunes without building financial expertise. Kiss has broken box-office records set by Elvis Presley and the Beatles, according to Simmons’s Web site. The band benefits from licensing agreements that sell apparel, wine bottles and jewelry emblazoned with the Kiss logo.Kiss wine? It says too little and yet too much.

-

What If Women Ran Wall Street?

Eddy Elfenbein, March 22nd, 2010 at 1:41 pmNew York Magazine has an article provocatively titled “What If Women Ran Wall Street?” It says pretty much what you’d expect.

I will add one thing about finance and gender. Wall Street is the world’s capital of the overcompensating male. Far from the hunter-gathering, trading demands that your brain hunts, but physically you’re only gathering. There’s a huge disconnect and as a result, Wall Streeters are excessively aggressive and obnoxious. If any of these guys were in a real work crew or infantry platoon, their strutting behavior would quickly stop.

-

Is Krugman Now Pro-EMH?

Eddy Elfenbein, March 22nd, 2010 at 1:13 pmAndrew Leonard has a good point: if Obamacare is such a disaster for the economy, where’s the market reaction?

More broadly: the perceived probability of passage, as indicated by Intrade, was only around 30 percent a month ago (which is why I’m still rubbing my eyes). So the expectations of what we’re told would be a great disaster have risen dramatically. And the market has yawned.I’m confused. Is Krugman is now praising efficient markets? I thought he was against all that.

Also, if the market falls from here, would that be enough for Krugman to support repealing healthcare reform? If there’s an Intrade contract for that, I’d be short. -

Friday the Thirteenth and the Stock Market

Eddy Elfenbein, March 22nd, 2010 at 11:21 amIn this study, we investigate whether Friday the thirteenth has an effect on the stock market returns. We report the following findings: (1) The returns prior Friday the thirteenth are lower than normally prior the year 1981. (2) The returns after Friday the thirteenth are higher than normally after the year 1980. (3) Serial correlation in stock indexes is positive prior the year 1981 and negative after the year 1980. (4) Serial correlation between Friday and the following day is significantly lower after Friday the thirteenth. Thus, we conclude that the Monday anomaly is not more evident than Friday the thirteenth anomaly, and the anomalies may be interrelated.

-

Market Rallies after HCR

Eddy Elfenbein, March 22nd, 2010 at 9:48 amDespite the healthcare bill passing last night or perhaps due to its passing, the stock market is up modestly this morning. I’m especially pleased to see our healthcare stocks rallying. One of my concerns about this year’s Buy List has been our heavy exposure to the healthcare sector.

Fortunately, those stocks have done fairly well so far. Medtronic (MDT), for example, is up over 3% today and is close to taking out its 52-week high. Gilead Sciences (GILD) is a 12% winner for the year and I think it has more room to run. Becton Dickinson (BDX), which is a medical device maker, is inches away from a new high.

Outside our healthcare stocks, Joey Banks (JOSB) is at another new high and Bed Bath & Beyond (BBBY) is up thanks to a very nice earnings report from Williams Sonoma (WSM).

Here’s the CEO of Stryker (SYK) discussing the impact of HCR on CNBC:

-

Looking at Bracketology

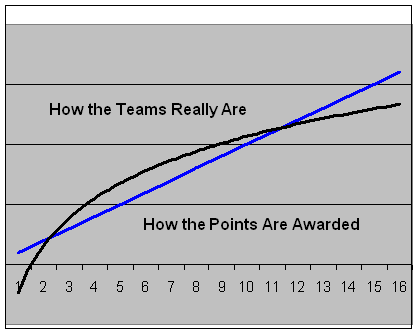

Eddy Elfenbein, March 18th, 2010 at 10:28 amToday is the beginning of the NCAA Basketball Tournament and I wanted to discuss an aspect of bracketology that’s somewhat related to investing. (Yes, it’s one of those posts.)

Most pools following the linear scoring method (i.e. you get 10 points if a #10 seed wins), but the key to understanding the game is that the quality of teams are not spread out linearly.

Generally speaking, the better the teams are, the greater the gap between them and the next seed. The teams are really spread out exponentially. If I had to guess, I’d say that the difference between a #12 seed and a #5 seed is probably about the same as the difference between a #3 seed and a #1 seed.

Here’s something what it looks like:

The black line shows how the teams really are while the blue line shows you how points are awarded. (Note: This isn’t drawn to scale. I’m just trying to show you the principle.)

As a result of this mismatch between exponential reality and linear price, there’s an inefficiency to exploit.

I’ll show you what I mean.

The tournament expanded to 64 teams in 1985 so we now have 25 years of data. Here’s how many Sweet 16 appearances each seed has had over the last 25 years.

Seed…………….Sweet 16……………..Points

#1……………………88…………………… 88

#2……………………64…………………… 128

#3……………………52 ……………………156

#4……………………43 ……………………172

#5……………………36 ……………………180

#6……………………35…………………… 210

#7……………………18 ……………………126

#8……………………9………………………..72

#9……………………3………………………..27

#10………………….18……………………..180

#11………………….11……………………..121

#12………………….17……………………..204

#13………………….4……………………….52

#14………………….2……………………….28

#15………………….0……………………….0

#16………………….0……………………….0

I’ve also included a point total. As you can see, there’s an advantage in picking teams at the optimal spread between quality and points like the #10 and #12 seeds.

The invaluable Abnormal Returns guided us to the Geek’s Guide to NCAA Tournament Pools at Wired. The magazine looked at the bracket picks done by thousands of people at ESPN. They then compared the crowd’s picks with some statistical predictions by two college basketball analysts.

Sure enough, the crowd has responded to incentives. You can see that the crowd has tended to overpick the #10, #11 and #12 seeds (those are the cells in green on Wired’s chart). The process is repeated in the later rounds with the #4 and #5 seeds. (Wired notes that the crowd’s consensus bracket usually finishes in the 80th percentile.)

This is interesting because the crowd is doing two things. One, they can be overruling what the bracket committee did. Also, they seem to be paying close attention to seeding and acting accordingly.

This behavior illustrates an aspect of why CAPM doesn’t work. Historical research has shown that the most volatile stocks aren’t the best performers as they should be according to the model. Instead, they’re among the worst. This makes sense since people are probably willing to overpay for a long shot of a big payoff, and this leaves the “sure-things” underrepresented.

Selecting the #10 and #12 seeds is a good strategy in the early rounds, but just like momentum investing, it quickly turns against you. After the first two rounds, the most logical way to play the brackets is to select the favorite. Yes, it’s boring but it works—just like value investing.

In the basketball tournament, you can see how unloved the #1 seeds are (note the red cells). The key fact of investing is that the most conservative and ignored stocks are often the best investments. -

Inflation Continues to Be Tame

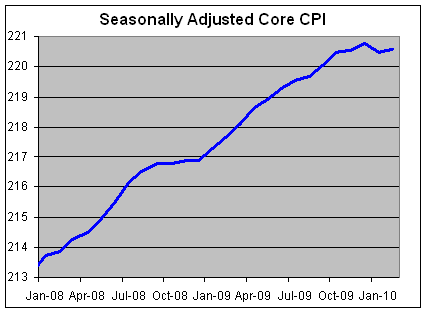

Eddy Elfenbein, March 18th, 2010 at 9:37 amToday’s CPI report shows that consumer prices were flat last month. Wall Street was expecting an increase of 0.1%. The core rate, which excludes volatile food and energy prices, rose just 0.05%.

Last month’s report was noteworthy since it was the first time since 1982 that the seasonally adjusted core rate had a meaningful decline. The core rate has now had its smallest year-over-year increase since 2004. Over the last four months, core inflation is running at just 0.66% annualized.

-

The Buy List Continues to Rally

Eddy Elfenbein, March 17th, 2010 at 9:26 amThe Buy List is up to another new high this year. As of 10 am, we’re up 7.6% for 2010 which is about double the S&P 500.

AFLAC (AFL) is up to another new high today. The shares are now up over 17% for the year. It’s hard to believe this stock was around $10 a share one year ago. I’m also pleased to see SEI Investments (SEIC) break out to a new 52-week high. The stock was upgraded a few days ago and it seems to be responding well. Currently, four of our Buy List stocks are up over 15% this year.

The best news yesterday came from Intel (INTC). Actually, it wasn’t news but a rumor that Intel will pre-announce strong earnings. The company hasn’t said anything and I doubt they will. The next earnings report isn’t due until April 13.

Still, the company is doing well. In January, Intel said that Q1 margins and revenues will above Wall Street’s expectations. The Street currently has Intel’s first-quarter’s earnings pegged at 37 cents a share. That seems about right. -

Why the Bears Are Wrong

Eddy Elfenbein, March 17th, 2010 at 9:00 amYesterday, James Altucher had a good article in the WSJ detailing the bearish arguments against stocks along with his responses. Here’s a sample:

• Many homes are still in foreclosure or under water:

• Although forececlosures last month were still 6% higher than the year ago period, they were 2% less than last month. The 6% is the lowest year-to-year increase since January 2006. The rate of foreclosures are decreasing and the fact that we had a month-to-month decrease in foreclosures suggests that the 50-month stretch of year-to-year increases could be coming to a close.

• The Case-Shiller Housing index has been up for the past six months, suggesting prices are stabilizing

• When a foreclosure happens, people have more money to spend (they are no longer spending on mortgage.

• The housing declines began in 2006. The market top didn’t happen until November, 2007 and the collapse didn’t happen until Lehman collapsed in September, 2008. The market collapse was more a function of the financial collapse and then the “Great Liquidation” (see below) than the housing collapse.

- Load More

Does anyone have a suit of armor, jet skis and a blowtorch I can borrow/rent? There's an experiment I'm working on.

This is pretty amazing. US elections combined since 1924:

GOP: 1,058,301,749

DEM: 1,057,846,951

Oth: 88,548,252Unemployment spikes in Washington, DC

-

-

Archives

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- October 2022

- September 2022

- August 2022

- July 2022

- June 2022

- May 2022

- April 2022

- March 2022

- February 2022

- January 2022

- December 2021

- November 2021

- October 2021

- September 2021

- August 2021

- July 2021

- June 2021

- May 2021

- April 2021

- March 2021

- February 2021

- January 2021

- December 2020

- November 2020

- October 2020

- September 2020

- August 2020

- July 2020

- June 2020

- May 2020

- April 2020

- March 2020

- February 2020

- January 2020

- December 2019

- November 2019

- October 2019

- September 2019

- August 2019

- July 2019

- June 2019

- May 2019

- April 2019

- March 2019

- February 2019

- January 2019

- December 2018

- November 2018

- October 2018

- September 2018

- August 2018

- July 2018

- June 2018

- May 2018

- April 2018

- March 2018

- February 2018

- January 2018

- December 2017

- November 2017

- October 2017

- September 2017

- August 2017

- July 2017

- June 2017

- May 2017

- April 2017

- March 2017

- February 2017

- January 2017

- December 2016

- November 2016

- October 2016

- September 2016

- August 2016

- July 2016

- June 2016

- May 2016

- April 2016

- March 2016

- February 2016

- January 2016

- December 2015

- November 2015

- October 2015

- September 2015

- August 2015

- July 2015

- June 2015

- May 2015

- April 2015

- March 2015

- February 2015

- January 2015

- December 2014

- November 2014

- October 2014

- September 2014

- August 2014

- July 2014

- June 2014

- May 2014

- April 2014

- March 2014

- February 2014

- January 2014

- December 2013

- November 2013

- October 2013

- September 2013

- August 2013

- July 2013

- June 2013

- May 2013

- April 2013

- March 2013

- February 2013

- January 2013

- December 2012

- November 2012

- October 2012

- September 2012

- August 2012

- July 2012

- June 2012

- May 2012

- April 2012

- March 2012

- February 2012

- January 2012

- December 2011

- November 2011

- October 2011

- September 2011

- August 2011

- July 2011

- June 2011

- May 2011

- April 2011

- March 2011

- February 2011

- January 2011

- December 2010

- November 2010

- October 2010

- September 2010

- August 2010

- July 2010

- June 2010

- May 2010

- April 2010

- March 2010

- February 2010

- January 2010

- December 2009

- November 2009

- October 2009

- September 2009

- August 2009

- July 2009

- June 2009

- May 2009

- April 2009

- March 2009

- February 2009

- January 2009

- December 2008

- November 2008

- October 2008

- September 2008

- August 2008

- July 2008

- June 2008

- May 2008

- April 2008

- March 2008

- February 2008

- January 2008

- December 2007

- November 2007

- October 2007

- September 2007

- August 2007

- July 2007

- June 2007

- May 2007

- April 2007

- March 2007

- February 2007

- January 2007

- December 2006

- November 2006

- October 2006

- September 2006

- August 2006

- July 2006

- June 2006

- May 2006

- April 2006

- March 2006

- February 2006

- January 2006

- December 2005

- November 2005

- October 2005

- September 2005

- August 2005

- July 2005

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His

Eddy Elfenbein is a Washington, DC-based speaker, portfolio manager and editor of the blog Crossing Wall Street. His